📌 Key Takeaways

High minimum order quantities in kraft paper force small converters to choose between volume discounts and operational flexibility—a choice that quietly drains working capital and warehouse space.

- The MOQ Barrier is a Cash Flow Problem, Not Just a Pricing Rule: When a supplier’s minimum order exceeds your monthly consumption by two or three times, you’re not buying paper—you’re making an involuntary loan to your own inventory that locks up capital for months.

- “Cheap” Per-Ton Prices Hide Expensive Carrying Costs: Industry benchmarks show that holding excess inventory costs 20-25% of its value annually, and can exceed 30% when credit is expensive—enough to erase the discount you thought you were getting.

- The True Cost Calculator Reveals When Higher Prices Protect Cash: A simple framework comparing extra tons carried, months of excess stock, and capital locked up shows when paying $30-50 more per ton for lower minimums actually strengthens your balance sheet.

- Agility Becomes Your Scale When Volume Isn’t an Option: Small converters who segment inventory into “healthy,” “at-risk,” and “excess” categories, then combine flexible sourcing with grade consolidation, turn MOQ constraints into design problems they can solve rather than walls they must accept.

- Strategic Sourcing Beats Volume Surrender: Dual-sourcing structures—using large principals for stable baseline grades while maintaining low-MOQ partners for trials and top-ups—preserve supply security without forcing over-ordering across your entire product mix.

Small and mid-sized packaging converters managing 20-50 tons of monthly kraft paper consumption will find this framework immediately applicable, preparing them for the detailed implementation strategies and calculation examples that follow.

The quote arrives, and the math looks simple enough. The per-ton price drops by 12% if you commit to a full container—60 tons instead of the 20 you actually need each month. Your finance partner sees the discount and asks the obvious question: why wouldn’t we take it?

Because that “savings” comes with a three-month supply sitting in your warehouse, locking up $45,000 in working capital you’d planned to use for equipment maintenance. The floor space fills up. Cash that should be circulating through your operations is instead stacked against the back wall in the form of kraft paper reels you won’t convert for another 90 days.

This is the MOQ barrier in action. It’s not simply a purchasing rule printed on a supplier’s quote sheet. It’s the structural constraint that forces small and mid-sized packaging converters to choose between operational agility and volume-based pricing—a choice that larger kraft paper buyers with deeper pockets and bigger warehouses rarely face.

When a kraft paper supplier’s minimum order quantity exceeds your actual consumption rate by a factor of two or three, you’re not just buying paper. You’re making an involuntary investment in inventory that quietly drains cash, blocks floor space, and reduces your ability to respond when a customer asks for a rush order in a different grade or when market conditions shift.

This guide explains what the MOQ barrier really is, why it exists in kraft paper supply chains, and how small converters are learning to design around it rather than surrender to it. The core insight is straightforward: agility can be your competitive edge when scale isn’t an option. The practical tool that makes this shift possible is a simple framework for calculating the true cost of inventory—a lens that reveals when paying a higher per-ton price for lower minimums actually protects your cash position and keeps your operation flexible.

By the end, you’ll understand the economics that create these volume requirements, see how to quantify the hidden costs they impose, and know which sourcing strategies other SMEs are using to break free without losing supply security.

How the MOQ Barrier Shows Up in a Converter’s Day-to-Day

The MOQ barrier is not just a rule on a quote; it’s the pattern that forces you to keep more stock and cash tied up than your business really needs. It appears whenever a supplier’s minimum order quantity—whether expressed as tonnage, roll count, or container load—exceeds the volume you can reasonably consume or convert within your natural replenishment cycle.

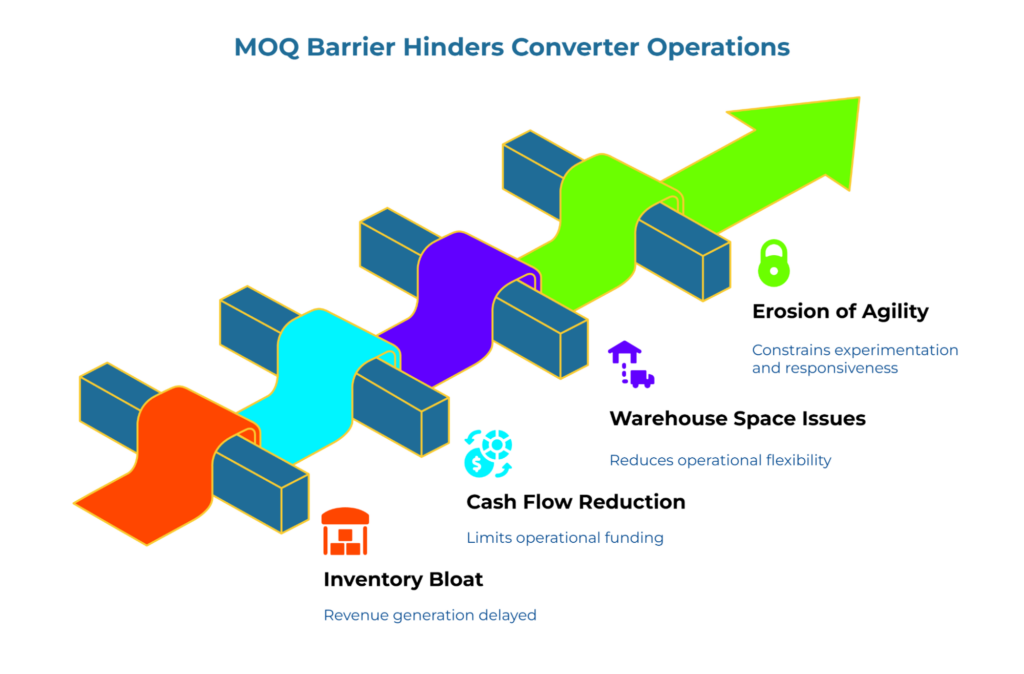

For a converter running 20 tons of kraft paper per month, a principal mill or trader might require 40, 60, or even 80 tons as the minimum for a competitive price. The immediate consequence is inventory bloat: those extra tons sit in your warehouse for two, three, or four months before they enter production. During that time, they’re not generating revenue. They’re consuming space, blocking cash, and creating risk.

From a cash-flow perspective, this over-buying is an involuntary loan to your own inventory. Working capital—defined as current assets (including inventory) minus current liabilities—represents the liquidity available to fund daily operations.[4] When MOQs force excess inventory, they directly reduce that liquidity. Suppose your monthly kraft paper spend is $30,000 at your actual consumption rate. A 60-ton MOQ forces you to commit $90,000 upfront—three times your normal monthly outlay. That $60,000 difference is capital that could have funded payroll, covered maintenance, or supported a marketing push. Instead, it’s locked in reels.

The warehouse impact is equally tangible. Floor space isn’t infinite. When principal MOQs force you to stack rolls three months deep, you lose the flexibility to take on a sudden custom order or trial a new grade without first clearing room. Packaging operations are often run in facilities where every square meter has already been allocated. Excess stock doesn’t just occupy space—it creates logistical friction that slows everything down.

What’s especially relevant for small converters is the erosion of agility. A business that’s locked into 60-ton orders can’t easily test a new supplier with a 5-ton trial. It can’t pivot quickly when a customer requests a different basis weight or finish. The volume commitment becomes a constraint on experimentation and responsiveness, which are often the very advantages that allow smaller players to compete against larger, slower-moving buyers.

Signs You’re Stuck Behind the MOQ Barrier

You know you’re facing this constraint when your warehouse has “dead corners” filled with reels from orders placed two or three months ago, when your finance team flags inventory levels as a working capital concern, or when you find yourself declining a customer’s request for a specialty grade because you’d need to order far more than that single job requires. Another telltale sign is high days-of-inventory on key grades—when the average number of days your stock sits before conversion significantly exceeds your supplier lead times and safety stock targets. These patterns indicate that your sourcing structure is dictating your operational decisions rather than the other way around.

Why the Cheapest Per-Ton Price Can Be the Most Expensive Choice

Price per ton is easy to compare, which is why it dominates purchasing conversations. But it’s only one component of total cost. When you chase a low per-ton price that’s contingent on a high MOQ, the savings on the unit price can be completely offset—or even reversed—by the cost of carrying that extra inventory. Cash has a cost, whether it’s the interest on a line of credit or the opportunity cost of capital that could have been deployed elsewhere. Storage has overhead. Risk accumulates: grades can become obsolete, customers can cancel, and paper can be damaged during extended storage.

Consider a simplified scenario. A converter uses 20 tons per month. Option A offers $750 per ton with a 60-ton MOQ. Option B offers $800 per ton with a 25-ton MOQ. At first glance, Option A saves $50 per ton—$3,000 total on a 60-ton order. But Option A also forces you to carry 40 extra tons (two extra months of supply) compared to what you’d hold with a purchase closer to your actual needs. If your cost of capital is 10% annually and you’re tying up an extra $30,000 in stock for those two months, the carrying cost alone is roughly $500. Add storage, handling, and the risk of grade obsolescence or damage, and that $3,000 “savings” shrinks considerably. In some cases, it disappears entirely.

The Economics Behind High MOQs (It’s Not Just ‘Greed’)

High MOQs exist because mills and principals are optimizing their own production, freight, and risk—even when that clashes with a small converter’s reality. Understanding this doesn’t mean accepting it forever. It shows where the leverage points are and why certain suppliers operate the way they do.

Kraft Paper Mills produces paper in campaigns. A paper machine might be scheduled to run a specific grade for several days or even weeks before switching to another specification. Changeovers are expensive. They require the machine to be stopped, cleaned, reconfigured, and restarted—a process that consumes time, materials, and labor without producing saleable output. For the mill, longer production runs spread those changeover costs across more tonnage, which improves efficiency and lowers per-unit production cost. A thousand-ton campaign allows the mill to amortize the changeover across a large output. A twenty-ton run makes the changeover cost per ton prohibitively high.

Freight optimization reinforces these volume requirements. Containerized and bulk shipments are priced by the load, not by the kilogram. A full twenty-foot container might hold 20 to 25 tons (subject to local road weight regulations), and a forty-foot container might hold 25 to 28 tons, depending on the grade and reel configuration. Shipping a half-full container doesn’t cut the freight cost in half; you still pay for the container. Ocean freight, trucking, and intermodal logistics all favor full loads. Suppliers pass these realities on to buyers in the form of MOQs that align with economically efficient shipment sizes.

Risk management also plays a role. When a mill or trader commits tonnage to a small buyer, they face the risk that the order will be delayed, modified, or canceled. Smaller orders often come from buyers who are less established, who may lack the financial cushion to absorb market volatility, or who are testing the supplier before committing to a long-term relationship. To manage this risk, suppliers either require higher minimums (which signal serious intent) or price smaller orders at a premium that compensates for the uncertainty.

The contrast is stark. A mill scheduling a thousand-ton campaign for a large, creditworthy buyer operates with predictable efficiency. An SME asking for 20 tons of the same grade represents a production slot that’s harder to justify economically. The mill isn’t refusing out of spite; it’s making a calculation about utilization, cost recovery, and risk. For the SME, this creates a structural disadvantage. Scale confers access to better pricing and more flexible terms, not because mills play favorites, but because the economics of production and logistics reward volume.

This doesn’t mean the situation is unchangeable. Recognizing the underlying drivers helps you identify where you have room to negotiate and where you need to design a different sourcing strategy. Some mills and traders do specialize in smaller lots, accepting the higher per-ton cost in exchange for shorter commitment cycles and mixed-load efficiencies. Others are willing to batch smaller orders from multiple buyers. The key is understanding that a principal mill optimized for long campaigns and full containers isn’t going to restructure its operations for a single 20-ton buyer—but you can still access the supply you need by working with partners who have built their business model around smaller, more flexible customers.

Calculating the “True Cost of Inventory” When You Chase MOQs

Per-ton price is only one part of the cost equation. The rest is cash locked in extra tons, storage and handling overhead, shrinkage or damage risk, and opportunity cost—what else that cash could have supported. When you over-order to meet an MOQ, you’re not just buying paper. You’re making an involuntary investment in inventory, and that investment has a price.

Inventory carrying cost is formally defined as the sum of physical holding costs (storage, insurance, obsolescence) and financial costs—specifically the Weighted Average Cost of Capital (WACC), which reflects what that cash could have earned if invested elsewhere.[1][2] Standard industry frameworks often cite 20-25% of inventory value annually as a baseline carrying cost, though this figure rises significantly during periods of high interest rates.[3] However, in high-interest environments or for businesses relying on expensive credit lines, true carrying costs can exceed 30% annually. This is where the True Cost of Inventory framework becomes essential. It’s a simple lens that forces the hidden costs into the open and allows you to compare offers on a more complete basis. Instead of asking, “Which supplier has the lowest per-ton price?” you ask, “Which offer protects my cash position and agility while still meeting my supply needs?”

What Goes Into Your True Cost of Inventory

The framework uses a handful of straightforward inputs that any small converter can gather from their own records and quotes.

Monthly usage is your baseline. Look at your historical consumption, averaged over the last few months to smooth out seasonal variation. For this example, suppose you use 20 tons per month.

Supplier MOQ is the minimum order size required to access a specific price. This might be 40 tons, 60 tons, or 80 tons depending on the supplier and the grade.

Price per ton under high MOQ is the unit price the supplier quotes for their standard minimum. Suppose this is $750 per ton for a 60-ton order.

Price per ton for a low-MOQ alternative is the unit price a smaller or more flexible supplier offers for an order closer to your actual needs. Suppose this is $800 per ton for a 25-ton order.

Cost of capital represents the annualized rate at which your working capital has a cost—either the interest you pay on a line of credit or the WACC that reflects your opportunity cost. A typical figure for SMEs might be 8% to 12% annually.

Waste rate is optional but worth including if you have data. Paper can be damaged, grades can become obsolete, or customer orders can be canceled, leaving you with stock you can’t easily move. Even a modest waste rate of 2% to 5% adds real cost when you’re carrying months of extra inventory.

A Simple Scenario: Paying More Per Ton to Buy Less

Let’s work through a scenario with illustrative numbers to see how the math plays out.

You use 20 tons of kraft paper per month. Supplier A requires a 60-ton MOQ and offers $750 per ton. Supplier B requires a 25-ton MOQ and offers $800 per ton. Supplier A looks cheaper at first: you’re saving $50 per ton, which is $3,000 on a 60-ton order.

But Supplier A forces you to carry 60 tons upfront. At 20 tons per month, that’s three months of supply. Supplier B’s 25-ton order covers just over one month of supply—closer to your natural replenishment cycle.

The extra inventory you’re holding with Supplier A is 35 tons (60 minus 25). At $750 per ton, that’s $26,250 in cash locked up. If your cost of capital is 10% annually, the carrying cost on that $26,250 over the two extra months is roughly $437. Add storage, insurance, and handling—conservatively estimated at $5 per ton per month—and the two extra months cost another $350 (35 tons × $5 × 2 months). Include a modest waste rate of 3% on the extra stock, and you’re adding another $788 in expected loss (35 tons × $750 × 3%). The hidden costs total approximately $1,575.

Meanwhile, the “savings” from Supplier A’s lower per-ton price is $3,000. Subtract the hidden costs, and your net advantage is $1,623—still positive, but much smaller than it first appeared. If your cost of capital is higher, your waste rate is greater, or your storage costs are above the conservative estimate, the advantage shrinks further. In some cases, it disappears entirely, and the “cheaper” option becomes more expensive on a total-cost basis.

Here’s where the quarterly impact becomes significant. If this ordering pattern repeats every three months, those carrying costs accumulate to nearly $5,500 annually—eroding a substantial portion of the perceived $12,000 annual price discount (assuming four orders per year). The gap between headline savings and actual savings narrows dramatically once you account for the recurring burden of excess inventory.

This is the breakeven per-ton premium you can justify. In this scenario, you could afford to pay roughly $27 more per ton to a low-MOQ supplier and still come out even or better on total cost. Supplier B’s $50 premium is above that threshold, so Supplier A still wins—but by a much narrower margin than the headline price suggests. If Supplier B could reduce their premium to $30 per ton, the math would flip, and the higher per-ton price would actually protect your cash and agility better than the “discount.”

Use this framework to compare your current principal MOQ with at least one low-MOQ option. The numbers will tell you whether a higher per-ton price actually makes you safer. The goal isn’t to eliminate MOQs entirely—that’s often unrealistic. The goal is to make an informed choice about when accepting a volume requirement makes sense and when it’s worth paying more for flexibility.

Practical Ways SMEs Overcome the MOQ Barrier Without Losing Supply Security

You can’t always change a mill’s MOQ, but you can change how you structure your buying and inventory so it doesn’t trap you. SME converters who’ve navigated this constraint successfully tend to use a handful of recurring strategies. None of them are silver bullets, but each one works in specific situations, and several can be combined to reduce the total burden.

Combining Volumes Across Multiple Sites or Buyers

If your company operates more than one plant, or if you’re part of a cooperative or informal network of converters, you can pool orders to reach a supplier’s MOQ while distributing the tonnage across multiple facilities. Each location takes only what it needs, but the collective volume satisfies the principal’s minimum.

In some markets, non-competing converters coordinate through formal Group Purchasing Organizations (GPOs) or informal buying clubs to split full-truck shipments. However, this approach demands clear legal agreements regarding liability and strict adherence to anti-trust regulations. Converters exploring this strategy should consult legal counsel to ensure compliance, particularly when coordinating pricing discussions or sharing competitive information.

This approach makes sense when the converters or plants involved use similar grades and can coordinate their purchasing cycles. The key risks are coordination complexity and potential quality inconsistency if the order is split across different production runs. Logistics also matter: if the plants are geographically dispersed, freight costs can eat into the savings from the volume discount.

From a True Cost of Inventory perspective, this strategy reduces the excess stock each individual facility has to carry, which lowers the cash lock and storage burden. The trade-off is the need for tighter coordination and shared trust among the participants.

Designing Grade Families to Reduce SKU Fragmentation

Many small converters carry too many stock-keeping units. A customer asks for a specific basis weight or finish, and the converter adds it to inventory without first checking whether an existing grade could serve the same purpose with minor adjustments to the converting process.

By consolidating grades into a smaller family of specifications, you increase the volume you run through each SKU, which moves you closer to meeting MOQs for each one. Instead of carrying eight different kraft paper grades, you might standardize on four. The reduction in fragmentation allows you to order closer to economically efficient minimums without over-stocking any single grade.

This strategy works best when your customer base is flexible enough to accept standardized specifications or when your converting equipment can adjust to handle minor variations. The risk is that consolidation might limit your ability to serve highly specialized orders. The upside is that you’re ordering in larger, more economical lots while still keeping total inventory aligned with actual demand.

Using Flexible Suppliers Who Specialize in Smaller Lots

Not all suppliers optimize for long campaigns and full containers. Some traders, distributors, and smaller mills have built their business model around serving SMEs with lower minimums, shorter commitment cycles, and the ability to ship mixed loads.

These suppliers typically charge a higher per-ton price to compensate for their higher operational complexity and smaller throughput per order. But for a converter who values agility and can’t afford to lock cash into three months of inventory, that premium can be justified through the True Cost of Inventory lens. You pay more per ton, but you tie up less cash, occupy less warehouse space, and retain the flexibility to test new grades or respond to sudden demand shifts.

Key risks include potential quality variation—smaller suppliers may not have the same process control as large integrated mills—and the need to verify their reliability and financial stability. The advantage is access to volumes that match your actual consumption without forcing you into inventory positions that strain your balance sheet.

Exploring Dual-Sourcing: Large Principal for Baseline, Low-MOQ Partner for Top-Ups

A common middle-ground strategy is to maintain a relationship with a traditional large supplier for your core baseline demand, while adding a flexible, low-MOQ partner for top-ups, niche grades, or trial orders. The large supplier still receives enough volume to justify favorable pricing, but you’re no longer locked into over-ordering every grade for every situation.

For example, you might commit to a 60-ton MOQ with your principal supplier for the grade that represents 70% of your monthly usage. For the remaining 30%—specialty grades, new trials, or seasonal spikes—you source from a smaller partner who accepts 10- or 15-ton orders. This structure keeps your core supply secure and economically priced while preserving flexibility at the margin.

The risk is managing two relationships and ensuring that quality remains consistent across both sources. You’ll need to monitor both suppliers’ delivery performance and maintain inventory buffers that account for the different lead times and reliability profiles. The benefit is that you’re no longer forced to over-order across your entire product mix. You apply the high-MOQ constraint only where it makes economic sense and use flexibility where it’s worth paying a premium.

Aligning Payment Terms with Inventory Reality

MOQs and payment terms interact in ways that amplify working capital strain. When a converter is forced into 60-ton orders with 30-day payment terms, but customers pay on 60-90 days, the cash gap widens dangerously.

While full payment-terms design sits in a dedicated cluster, converters can explore several financial tools to bridge this gap. Supply chain financing allows buyers to extend payment terms with suppliers while a financial institution pays the supplier promptly. Trade credit insurance protects against customer default risk, which can make banks more willing to provide favorable financing terms. Where volume leverage exists, some converters negotiate partial prepayments or staged payment schedules that better align with their stock turnover rates.

Each of these strategies interacts with the True Cost of Inventory framework. Combining volumes reduces the cash-per-facility burden. Consolidating grades allows you to hit MOQs without over-ordering total tonnage. Flexible suppliers let you pay a premium to avoid inventory bloat. Dual-sourcing balances the economics of scale on your core grades with the agility to handle variation and experimentation. None of these is a universal solution, but together they form a toolkit that allows you to design around volume constraints rather than simply accept them.

From Volume Constraints to Agility: What Changes When You Shift Your Mental Model

When you treat agility as your scale, MOQ rules become constraints to design around—not walls that define your business. This shift in perspective is more than semantic. It changes how you evaluate suppliers, structure contracts, and allocate working capital.

The old mental model says, “We must hit principal MOQs or we’re not serious buyers.” It treats the supplier’s minimum as the floor for credibility and accepts over-stocking as the necessary price of access. The new model says, “We must keep inventory and cash aligned with our actual demand and risk appetite.” It acknowledges that volume requirements exist for structural reasons but refuses to let them dictate operational strategy.

Concrete changes follow from this reframing. Converters who adopt an agility-first approach build inventory review routines into their monthly operations. They track monthly usage, lead times, and usage variability with the same rigor they apply to production schedules. Many implement a simple segmentation framework, categorizing stock into “healthy” (turning at expected rates), “at-risk” (approaching obsolescence or showing demand decline), and “excess” (significantly above safety stock targets) categories. This data becomes the foundation for negotiations: instead of accepting a supplier’s MOQ as a given, they present consumption data and ask, “What’s the smallest order you can accommodate given our actual throughput?”

They also start experimenting with new suppliers in small, controlled trials. Instead of committing 60 tons to an unknown partner just to access their pricing, they test with 10 or 15 tons—even if it costs more per ton—to validate quality, delivery reliability, and fit with their equipment. This approach treats the premium on a small trial order as the cost of de-risking a larger future commitment, which is far cheaper than discovering quality problems or delivery failures after locking up $50,000 in inventory.

From a working capital and risk perspective, agility reduces not just stock levels, but also operational panic and firefighting. When you’re not locked into three months of inventory for every grade, you can respond to a customer’s request for a rush order in a different basis weight. You can pivot when market conditions shift or when a long-term customer changes specifications. You’re no longer hostage to decisions you made months ago under different circumstances.

A simple before-and-after comparison illustrates the shift. Before: An SME converter orders 60 tons to hit a principal MOQ, sits on two extra months of stock, and declines a customer request for a trial order in a new grade because the warehouse is full and cash is tight. After: The same converter uses the True Cost of Inventory framework to justify a 25-ton order at a higher per-ton price, maintains a leaner inventory profile, and has the space and capital to take on the trial order, which turns into a long-term relationship worth far more than the savings from chasing the volume discount.

Where to Go Next

If you’re dealing with inventory overload when principal MOQs force you to over-buy, the next step is to work through the cost-of-carry calculations in detail and identify which grades are tying up the most cash relative to their turnover rate.

If your immediate challenge is sourcing low-MOQ kraft paper when your cash is tight, focus on building a shortlist of flexible suppliers and running side-by-side comparisons of their total cost using the framework outlined here.

For a broader perspective on how agility functions as a competitive advantage for smaller buyers, see why agility is the new scale in paper procurement—a strategic overview that connects inventory flexibility to risk management, customer responsiveness, and long-term resilience.

FAQs & Edge Cases

Is it ever okay to accept a high MOQ just for the price?

Yes, if the discount genuinely justifies the carry cost and you have the cash and space to absorb the extra inventory without operational strain. Run it through the True Cost of Inventory framework and see if the numbers work. For stable, high-volume grades where usage is predictable and storage isn’t a constraint, hitting a principal MOQ might still be the most economical choice. The issue arises when you’re forced into high MOQs across your entire product mix, including grades with variable or low demand.

What if my bank prefers I show large stocks as ‘security’?

This is a legitimate concern in some lending relationships, where inventory on the balance sheet functions as collateral. However, carrying excess inventory to satisfy a lender’s preference can be expensive if it locks up cash that could be deployed more productively elsewhere. One approach is to present your lender with data showing that leaner, faster-turning inventory doesn’t reduce your creditworthiness—it improves your cash flow and reduces the risk of obsolescence. Stock that is damaged, obsolete, or mismatched to demand weakens security over time. Another option is to negotiate financing terms that recognize accounts receivable and equipment as collateral, reducing the reliance on raw material stock.

Can I negotiate MOQs directly with mills as a small converter?

In most cases, a large integrated mill will not restructure its MOQ policy for a single small buyer. Mills optimize for long runs and full loads, and changing that structure is economically difficult. However, negotiation is still possible at the edges. You can ask about batching—where the mill combines your order with others to reach a production-efficient quantity. You can inquire whether they have a distribution partner who handles smaller lots. You can also negotiate on lead time and delivery frequency rather than MOQ: instead of taking 60 tons at once, you might commit to 60 tons over three months delivered in 20-ton shipments, which reduces your inventory peak even if the total commitment remains the same. Offering predictable long-term schedules or combining several grades into a single load can also justify more flexible terms.

Disclaimer: This article provides general information about inventory and procurement for educational purposes. It is not financial, legal, or investment advice. Please consult your own advisors before making decisions based on these concepts.

References

[1] UNIS Freight & Logistics Glossary – “Inventory Carrying Cost” (definition and components of inventory carrying cost)

[2] Datex – “What are Inventory Carrying Costs?” (overview of capital, storage, handling, and risk cost categories in carrying cost)

[3] FreshBooks – “What is Inventory Carrying Cost? – Formula & Application” (discussion of capital costs as a component of inventory value)

[4] Investopedia – “Working Capital” (definition of working capital and its role in liquidity)

Our Editorial Process

Our expert team uses AI tools to help organize and structure our initial drafts. Every piece is then extensively rewritten, fact-checked, and enriched with first-hand insights and experiences by expert humans on our Insights Team to ensure accuracy and clarity.

About the PaperIndex Insights Team

The PaperIndex Insights Team is our dedicated engine for synthesizing complex topics into clear, helpful guides. While our content is thoroughly reviewed for clarity and accuracy, it is for informational purposes and should not replace professional advice.