📌 Key Takeaways

Chasing volume discounts through oversized MOQs drains working capital, locks inventory for months, and turns “scale” into a strategic trap for small converters.

- Agility Outperforms Scale for SMEs: For converters with limited working capital and storage, the ability to source right-sized volumes from multiple suppliers creates more value than pursuing discounts tied to mill-scale MOQs.

- The MOQ Barrier Functions as a Filter: High minimum order quantities aren’t just operational requirements—they’re deliberate mechanisms that tier buyers into “main accounts” versus secondary status, forcing small converters to overcommit or accept unfavorable terms.

- Working Capital Is Your Real Constraint: Inventory carrying costs run 20-30% annually; when you factor in storage, obsolescence risk, and opportunity cost, that “discount” bulk order often costs more than sourcing smaller volumes at standard pricing.

- Diversification Creates Negotiation Power: In an agility-first model, leverage comes from optionality rather than order size—suppliers compete for reliable, repeatable customers who can shift volume based on service, quality, and responsiveness.

- Stock Days Beat Price Per Ton: The best sourcing decision keeps you nimble rather than heavy—a deal that increases your stock days from 30 to 75 typically creates more cash strain than the per-ton savings are worth.

Small and mid-sized packaging converters, procurement managers, and business owners in the kraft paper converting industry will find their strategic framework here, preparing them for the detailed procurement approach that follows.

The procurement playbook most small converters inherited wasn’t written for them.

Picture a packaging converter with 15 employees and a steady customer base. A new order comes in—profitable, manageable, exactly the kind of work that keeps the lights on. But there’s a problem. The kraft paper grade they need is locked behind a 20-ton minimum order quantity from their primary mill. That’s six months of inventory for a single grade, which means tying up between $20,000 and $30,000 in working capital (depending on grade and landed costs) and renting additional warehouse space. The choice becomes binary: turn down the order or accept terms designed for kraft paper buyers ten times their size.

This scenario plays out across the industry because small and mid-sized converters are operating with a mental model borrowed from large mills and multinational buyers. In that world, scale equals negotiating power. Bigger orders mean better prices. Volume is the path to competitive advantage.

But for converters running tight operations with limited storage and narrow cash flow margins, chasing scale often becomes a trap. The traditional “bigger is better” approach assumes you have the working capital to absorb oversized orders, the warehouse space to store them, and the customer base to move inventory before it becomes a liability.

For SME converters, agility is the new scale.

This article challenges the inherited orthodoxy that small buyers must either accept unfavorable terms or grow large enough to demand better ones. We’ll examine why procurement agility—the ability to source the right volumes from a diversified network of kraft paper suppliers—creates more strategic value than pursuing discounts tied to oversized MOQs. The centerpiece is a comparison matrix that contrasts scale-first and agility-first approaches across the dimensions that actually matter to small converters: working capital impact, supply resilience, negotiation leverage, decision speed, and operational flexibility.

The Old Script: Why SMEs Were Told to Chase Scale

The language of paper procurement reflects its industrial origins. Mills speak in terms of production runs, capacity utilization, and economies of scale. Brokers and large distributors reinforce this narrative because their business models depend on consolidating volume. The implicit message to small buyers has always been clear: if you want competitive pricing and reliable supply, you need to buy like the big players.

This thinking made sense in an era when information asymmetry gave mills and large traders significant power. Small converters had limited visibility into global supply chains, few alternatives to local distributors, and no practical way to verify or compare suppliers across borders. The received wisdom became: accept the terms available, or grow large enough to set your own.

The industry reinforces this through explicit tier structures. For example, a converter with current consumption of 150 tonnes per month may be encouraged to increase commitments to 200–250 tonnes to access ‘main account’ treatment. In this context, high MOQ thresholds function as a filtering mechanism—those who cross it receive priority pricing and service, while those who don’t must accept secondary status. The MOQ barrier becomes not just an operational requirement but a deliberate tool for concentrating volume and testing buyer commitment.

But that framing embeds several assumptions that don’t hold for most SME converters. It assumes you can afford to lock capital in inventory for months at a time. It assumes your customer base is stable enough to guarantee you’ll move that inventory before market conditions shift. It assumes you have warehouse capacity that scales with opportunistic bulk purchases. And it assumes that the discount you receive for volume actually compensates for these risks.

For many small converters, none of these assumptions are true. The hidden subtext of “small buyers take what they get” is that the procurement model itself was never designed with their constraints in mind.

How the MOQ Barrier Turns Scale into a Trap

Minimum order quantities exist for legitimate operational reasons. Mills achieve efficiency through long production runs of standardized grades. Breaking down production to accommodate small orders increases setup costs and complicates scheduling. From the mill’s perspective, MOQs protect margin.

But from the converter’s perspective, high MOQs create three distinct pressures. The first is immediate: cash flow strain. Good working capital management is crucial to meeting short-term obligations and keeping operations stable; excess stock directly erodes that stability (Source: Investopedia). Purchasing six months of inventory upfront means that working capital—already a scarce resource—becomes trapped in warehouse stock rather than available for equipment upgrades, labor, or responding to customer opportunities. For a small converter operating on thin margins, this isn’t just inconvenient. It’s a structural constraint on growth.

The second pressure is spatial. Warehouse space costs money, whether you own or lease. Bulk orders often force converters to rent additional storage or inefficiently stack materials in production areas, creating handling delays and increasing the risk of damage or moisture contamination. The kraft paper you bought at a “discount” becomes more expensive when you factor in the cost of storing it properly for six months.

The third pressure is strategic. When you’ve committed significant capital and space to a single grade from a single supplier, your flexibility to respond to market changes evaporates. A customer requests a trial run with a different basis weight? You can’t pivot quickly. A competitor introduces a product that requires a specialty liner? You’re locked in. The high-MOQ trap isn’t just about cash and space—it’s about losing the ability to adapt.

The Hidden Cost of Buying Like a Big Mill

The volume discount pitch is compelling: buy more, save per ton, strengthen your competitive position. But this framing ignores the carrying costs that small converters absorb when they oversize orders to hit mill minimums.

Start with the opportunity cost of capital. That $35,000 tied up in a six-month kraft paper stockpile isn’t available for other uses. You can’t invest it in a new slitter to improve production efficiency. You can’t use it as a buffer to negotiate better payment terms with customers. You can’t deploy it to test a new product line or pursue a strategic account that requires a different material specification. The capital is static, sitting in a warehouse, slowly losing value to storage costs and the risk of quality degradation.

Inventory is one of the largest users of working capital in many businesses; holding more than needed directly squeezes liquidity (Source: Investopedia). Standard supply chain models estimate that total inventory carrying costs typically run between 20% and 30% of inventory value annually once you factor in the cost of capital, storage, insurance, shrinkage, and obsolescence risk. For a $35,000 stockpile, that’s $7,000 to $10,500 per year—which often erases the per-ton discount that justified the bulk purchase in the first place.

Then there’s the rigidity cost. Large standing inventories reduce your ability to switch suppliers, test new grades, or respond to customer requests that fall outside your current stock profile. If a customer approaches you with a project that requires a different Cobb value or a lighter basis weight, you can’t easily pivot. Your inventory becomes an anchor, not an asset.

The conventional scale-first approach also embeds a hidden assumption about demand stability. It assumes that customer orders will arrive in predictable patterns and that the grades you’ve stockpiled will align with those orders. But small converters often serve diverse customers with varying needs. Demand for specific grades can shift month to month based on customer projects, seasonal patterns, or competitive dynamics. When your inventory doesn’t match incoming orders, you’re stuck managing mismatches—using suboptimal grades, disappointing customers, or liquidating stock at a loss.

Supply concentration amplifies this risk. A high-MOQ, single-supplier setup means that any disruption—port congestion, production issues, quality drift, or changed credit policy—hits the SME much harder. Recent global shocks have highlighted how vulnerable smaller firms are when supply lines are too concentrated and cash buffers are thin (Source: OECD). Larger companies can absorb such shocks or diversify quickly; SMEs often cannot.

The truly insidious element is that the scale-first mindset trains small converters to view their size as a weakness rather than a potential advantage. The implicit message is that if you could just buy more, store more, and commit more capital, you’d unlock better terms. But this ignores the fundamental mismatch between mill-scale procurement logic and the operational reality of a 15-person converter with limited storage and fluctuating customer demand.

Deep Dive: What Procurement Agility Really Means for SMEs

Procurement agility is not ad-hoc buying or opportunistic spot purchasing. It’s a systematic approach to sourcing that prioritizes flexibility, resilience, and capital efficiency over the pursuit of volume discounts.

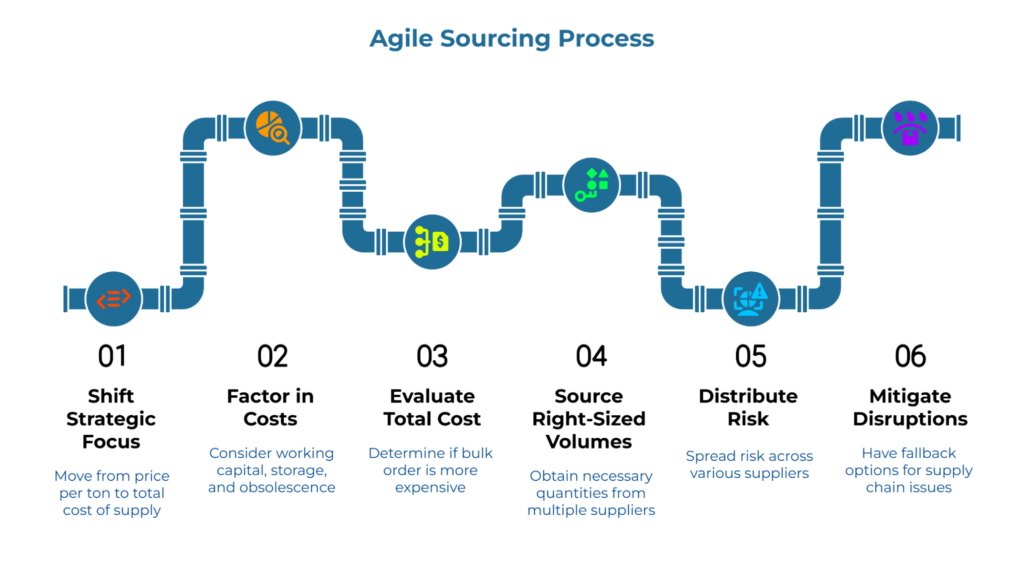

At its core, agility means building a procurement model that matches your actual operational constraints rather than imitating the purchasing behavior of companies ten times your size. It means recognizing that for small converters, the ability to source the right volume at the right time from a diversified network of suppliers creates more strategic value than squeezing an extra 2% discount by oversizing orders.

This distinction matters because the industry’s default framing conflates “agility” with “reactive purchasing”—buying what you need when you need it with no forward planning. That’s not what we’re describing. An agile procurement strategy still involves forecasting demand, building supplier relationships, and negotiating terms. The difference is in the structural design: instead of committing to large volumes with a single mill to secure better pricing, you build a portfolio of supplier relationships that gives you optionality.

Why Agility Matters

Procurement agility is the ability to adjust sourcing decisions quickly and safely as demand, prices, or supplier conditions change. For SMEs, agility is directly linked to three outcomes: working capital protection—buying closer to actual demand and keeping cash available for operations rather than locked in stock; supply resilience—designing options so that one supplier, one route, or one grade does not control the entire business; and margin protection—maintaining the ability to accept attractive, smaller or urgent jobs without being blocked by past purchasing decisions.

Research on corporate resilience indicates that companies with shorter cash conversion cycles and active liquidity management are significantly better positioned to absorb supply chain shocks and recover faster (Source: McKinsey & Company). This isn’t theoretical. During supply chain disruptions, converters with diversified supplier networks and lower inventory positions consistently demonstrated faster recovery times and maintained operational continuity better than those locked into single-source, high-volume commitments.

A common misconception is that agile sourcing means sacrificing quality or reliability. The assumption is that small, flexible orders can only be sourced from secondary traders or questionable mills willing to break down larger lots. But the reality is more nuanced. Many mills and established traders now recognize that serving SME converters with smaller, more frequent orders can be a profitable segment if structured correctly. Some offer split shipments, allowing you to commit to a larger total volume over time while taking delivery in manageable increments. Others specialize in serving smaller buyers precisely because they’ve optimized their operations for this segment.

The real-world implication of agility-first sourcing is that it shifts your strategic focus from price per ton to total cost of supply. When you factor in working capital costs, storage expenses, obsolescence risk, and the value of operational flexibility, the “cheaper” bulk order often proves more expensive than sourcing right-sized volumes from multiple suppliers at a slightly higher per-ton cost.

Another implication is that agility allows you to derisk your supply chain. When you depend on a single mill or distributor for a critical grade, any disruption—production delays, quality issues, freight complications, or simply the supplier deciding to prioritize larger customers—becomes your emergency. Agile sourcing distributes that risk across multiple relationships, giving you fallback options when disruptions occur.

The SME Kraft Paper Sourcing Strategy in One Sentence

An effective SME kraft paper sourcing strategy is a structured approach to building and maintaining relationships with a diversified network of mills, traders, and distributors who can supply the grades you need in volumes that align with your actual consumption rate and working capital capacity, with backup options for critical materials and the flexibility to test new suppliers without over-committing.

This definition deliberately emphasizes three elements that distinguish a strategy from reactive buying: diversification (multiple suppliers, not a single-source dependency), volume alignment (order sizes that match your real consumption and cash position, not mill minimums), and flexibility (the ability to adapt without being locked in). It’s not about buying small because you can’t afford to buy large. It’s about buying smart—matching your sourcing structure to your operational reality.

The Scale vs. Agility Comparison Matrix

The difference between scale-first and agility-first procurement becomes clearest when you compare them across the dimensions that actually impact your business operations.

| Dimension | Scale-First Approach | Agility-First Approach |

| MOQ & Working Capital Impact | High Capital Intensity: Requires significant upfront capital allocation, extending the Cash Conversion Cycle and reducing liquidity available for operational expenses | High Liquidity: Smaller, frequent outlays keep the Cash Conversion Cycle short, preserving working capital for immediate operational needs or unexpected expenses |

| Supply Resilience / Risk of Disruption | High Concentration Risk: Reliance on a single source creates a Single Point of Failure; disruptions (port strikes, mill outages) directly impact production capability | Distributed Risk: A diversified supplier network creates redundancy; if one supply route fails, pre-qualified backup options ensure business continuity |

| Negotiation Leverage for SMEs | Volume-Dependent: Leverage is derived strictly from order quantity, placing SMEs at a structural disadvantage against larger multinational buyers | Optionality-Dependent: Leverage is derived from the ability to switch suppliers; competitive tension is created by service reliability rather than just order size |

| Operational Complexity & Decision Speed | Simpler relationship management but slower to adapt when needs change | Requires more active supplier management but enables faster response to customer demands |

| Operational Flexibility (Testing New Grades/Customers) | High Opportunity Cost: Large standing inventories act as an anchor, restricting the ability to pivot to new paper grades or customer specifications without liquidation losses | Adaptive: Low inventory levels allow for rapid market response, enabling the testing of new grades or acceptance of niche orders without being blocked by legacy stock |

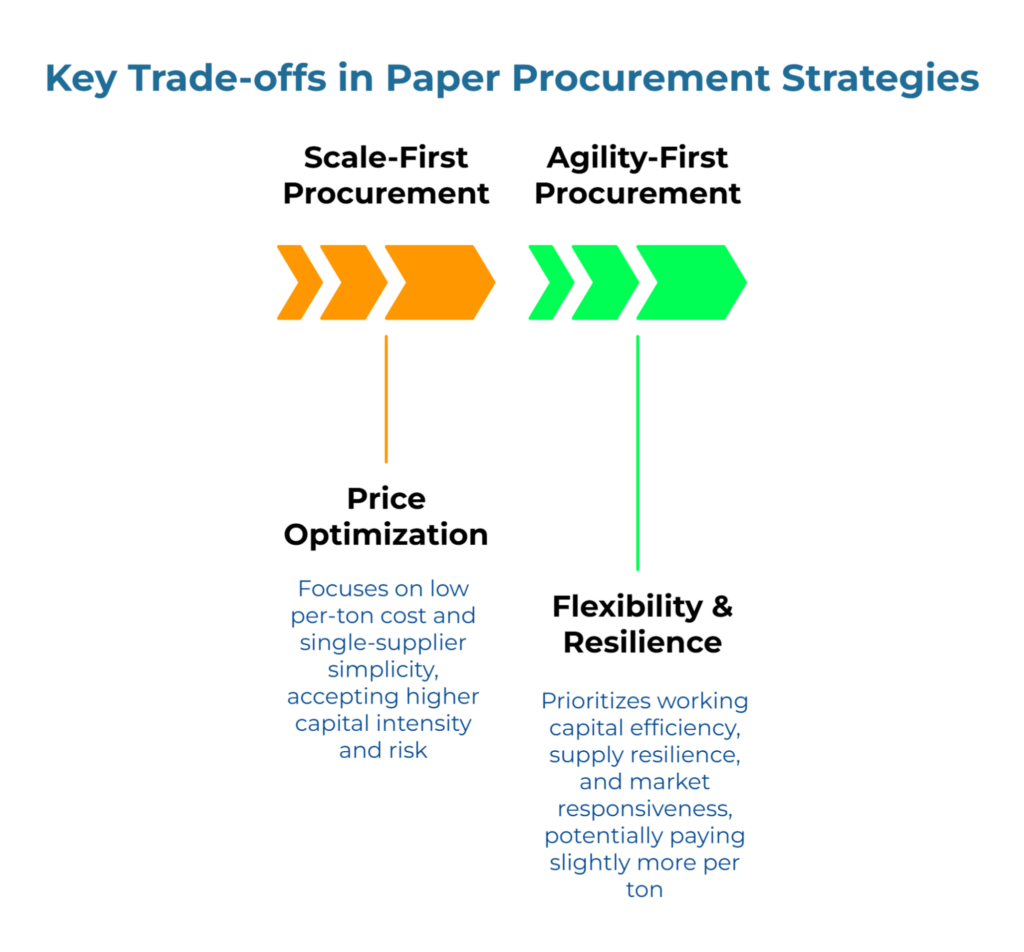

The pattern that emerges is clear: scale-first procurement optimizes for per-ton cost and relationship simplicity, but it does so by accepting higher capital intensity, concentration risk, and operational rigidity. Agility-first procurement inverts these trade-offs. You may pay slightly more per ton on individual orders, but you gain working capital efficiency, supply resilience, and the flexibility to respond to market opportunities or disruptions.

For small converters, this trade-off usually favors agility. The additional cost per ton—if it even exists after accounting for carrying costs—is more than offset by the strategic benefits of not having your capital and warehouse space locked into a single supplier’s MOQ requirements.

Another way to understand this matrix is that it challenges the implicit assumption that procurement is a zero-sum negotiation where your only leverage is order size. In an agility-first model, your leverage comes from diversification and optionality. Suppliers compete for your business not because each individual order is large, but because you represent a reliable, repeatable customer who can shift volume based on service, quality, and responsiveness.

What Changes When You Stop Apologizing for Being Small

The shift from scale-first to agility-first thinking changes how you approach supplier conversations and internal decision-making. Instead of positioning your size as a limitation that suppliers need to accommodate, you frame it as a structural advantage that allows you to be more responsive and adaptive than larger competitors.

When you’re sourcing from an agility-first perspective, the conversation with a potential supplier changes immediately. You’re no longer asking if they can “work with” your smaller volumes. You’re evaluating whether their capabilities align with your sourcing strategy. Can they deliver consistent quality in smaller lot sizes? Do they have the logistics infrastructure to support frequent, reliable shipments? Are they set up to handle split deliveries or flexible scheduling? Can they provide the documentation and traceability you need without the overhead that makes sense only for very large orders?

One of the most tangible shifts involves how you define “good deals.” A low price with a very high MOQ and long payment period may look attractive on paper. But if it pushes your stock days from 30 to 75, the cash strain and risk often outweigh the nominal savings. In an agility-first mindset, the real question becomes: “Does this deal keep us nimble, or does it make us heavy?”

This framing shift has practical implications. Suppliers who specialize in serving SME converters—often regional mills, specialized traders, or distributors with optimized warehousing—become more attractive partners than large mills that view small orders as an inconvenience. You’re not settling for second-tier suppliers; you’re selecting partners whose operational model matches yours.

Internally, the agility lens changes how you evaluate procurement decisions. The relevant question is no longer “Can we afford to buy this much upfront to hit the MOQ?” but rather “Does this order align with our consumption forecast and cash flow capacity, and do we have backup suppliers if this relationship underperforms?” The decision criteria shift from price per ton and order size to total cost of supply and supply chain resilience.

For suppliers reading this, the opportunity is straightforward: SME converters represent a substantial and underserved segment of the market. Many small buyers are actively looking for partners who can provide mill-quality materials in volumes that align with their working capital constraints. If you can structure your offerings to support agility-first sourcing—through split shipments, flexible minimum orders, or value-added services like quality pre-inspection—you differentiate yourself from competitors who are still chasing only the largest accounts.

New Questions to Ask Suppliers

When evaluating potential suppliers from an agility-first perspective, the questions you ask need to focus on flexibility, reliability, and service rather than just price per ton and payment terms.

What is the smallest MOQ at which you can still treat us as a serious, repeat customer?

This question directly addresses the tier system that many suppliers use. You’re not asking for a favor; you’re identifying whether their business model can accommodate your size as a strategic account rather than a transactional one-off.

Can you support split shipments over a defined period?

This question probes whether a supplier can commit to a larger total volume while allowing you to take delivery in manageable increments that align with your actual consumption and storage capacity. A supplier who offers split shipments understands the working capital constraints of small buyers.

If we commit to steady monthly off-take, can you give us more flexibility on shipment size or schedule?

This reframes the negotiation from “Can you accept smaller orders?” to “Can we design a relationship that gives both sides predictability?” Many suppliers value consistency over sheer volume per shipment.

What is your typical lead time variability, and how do you communicate delays?

Agility depends on predictability. A supplier who can reliably deliver on schedule—even if the lead time is slightly longer—is often more valuable than one who promises fast delivery but frequently misses commitments. The question also tests their communication practices, which become critical when you’re managing multiple supplier relationships.

Do you offer smaller trial quantities before committing to larger volumes?

This reveals whether the supplier is willing to invest in building a relationship rather than requiring immediate commitment. For small converters testing a new grade or supplier, the ability to run a pilot order without over-committing is essential.

What verification documentation do you provide, and can I inspect materials before shipping?

Quality assurance becomes more important when you’re diversifying your supplier base. You need confidence that a new supplier can consistently meet specifications. Suppliers who proactively offer certificates of analysis, allow pre-shipment inspections, or provide sample approval processes are demonstrating their commitment to quality transparency.

In a tight situation, what is the fastest realistic lead time if we prioritize speed over rate?

This question surfaces whether the supplier has the operational flexibility to respond to urgent needs. The answer tells you whether they can be a true partner during disruptions or peak demand periods.

New Way to Judge Sourcing Options

When several offers look similar on rate, an agility-first lens provides clear decision rules that go beyond nominal price per ton.

Prefer the option that keeps stock within a sensible number of days, even if the rate is slightly higher. If one supplier offers a 5% lower rate but requires you to hold 90 days of inventory versus another at standard pricing who can deliver in 30-day cycles, the working capital benefit of the second option often outweighs the discount.

Value second and third supplier options, especially for critical grades, even if they are used for smaller volumes. Having a backup supplier you’ve already qualified and tested is worth the complexity of managing an additional relationship. The cost of scrambling to find an alternative during a disruption far exceeds the administrative overhead of maintaining portfolio diversity.

Reward clarity and predictability in lead times, quality, and documentation at least as much as marginal price differences. A supplier who consistently delivers on time with accurate documentation and stable quality creates operational stability. That stability reduces internal firefighting, improves planning accuracy, and allows you to commit more confidently to customers.

Consider the total relationship value, not just the transaction. Can this supplier help you enter new markets? Do they provide market intelligence or technical support? Are they willing to collaborate on trials or custom specifications? These intangibles often create more value than a few dollars per ton in pricing.

Where This Mindset Connects to the Rest of the MOQ and Agility Hub

This article provides the conceptual foundation for understanding why agility matters for small converters and how it differs from traditional scale-first thinking. But shifting your procurement approach requires more than just adopting a new mental model. You need practical frameworks for implementation.

The guide to overcoming the MOQ barrier translates this worldview into a tactical playbook. It covers strategies for negotiating with mills, working with traders who can break down larger lots, and using aggregation models to access mill-quality materials without accepting mill-scale MOQs. If this article has convinced you that agility is valuable, that guide shows you how to operationalize it.

Similarly, the agile procurement playbook for SME converters provides a step-by-step framework for building and managing a diversified supplier network. It addresses practical questions like how many suppliers you need for critical grades, how to structure trial orders, and how to balance relationship management complexity against supply chain resilience.

For converters concerned about supplier quality when diversifying, the spoke on how to verify international suppliers without travel offers a risk-reduction framework. Agility doesn’t mean sacrificing due diligence. It means having structured processes for vetting new suppliers efficiently.

Finally, if working capital constraints are your primary barrier to implementing agile sourcing, the guide on how to source low-MOQ kraft paper when your cash flow is tight provides specific tactics for identifying suppliers and structuring orders that align with your cash position. It also connects to broader working capital topics, including understanding the hidden cost of high MOQs and inventory and managing MOQ and lead time surprises on large orders.

For converters concerned about supplier quality when diversifying, the spoke on how to verify international suppliers without travel offers a risk-reduction framework. Agility doesn’t mean sacrificing due diligence. It means having structured processes for vetting new suppliers efficiently.

Finally, if working capital constraints are your primary barrier to implementing agile sourcing, the guide on how to source low-MOQ kraft paper when your cash flow is tight provides specific tactics for identifying suppliers and structuring orders that align with your cash position. It also connects to broader working capital topics, including understanding the hidden cost of high MOQs and inventory and managing MOQ and lead time surprises on large orders.

This ecosystem of content is designed to move you from understanding why agility matters to knowing how to build it into your procurement operations. The mental model presented here is the first step. The linked resources provide the operational detail.

Conclusion: Agility Is the Real Scale for SME Converters

The inherited playbook for paper procurement was written by and for large buyers with deep pockets, massive storage capacity, and stable demand. For decades, small converters were told that their size was a weakness—that they needed to grow, consolidate orders, and chase volume discounts to compete.

But the reality is that the MOQ barrier and scale-first thinking often hurt small converters more than they help. Tying up working capital in oversized inventory, accepting concentration risk with a single supplier, and sacrificing operational flexibility to secure marginally better pricing doesn’t create competitive advantage. It creates fragility.

Agility—the ability to source the right volumes from a diversified network of suppliers who align with your consumption rate and working capital capacity—is the structural advantage that matches how small converters actually operate. You can’t compete with large converters on bulk purchasing power, but you can compete on responsiveness, flexibility, and capital efficiency. That’s a different kind of scale, and for many small businesses, it’s the one that actually matters.

The Scale vs. Agility matrix you’ve seen in this article isn’t just a comparison chart. It’s a decision-making tool. Use it to evaluate your current supplier relationships and identify where you’re accepting scale-first trade-offs that don’t serve your business. Then begin building the agile sourcing strategy that gives you resilience, optionality, and the working capital flexibility to grow on your own terms.

If you’re ready to map your existing suppliers against the agility framework and start building a more resilient procurement strategy, the practical guides linked throughout this article provide the next steps. Neutral platforms and directories like PaperIndex.com can also support agility-first sourcing by giving you visibility into a diverse pool of mills, traders, and distributors without requiring large upfront commitments or forcing you into single-supplier dependence.

Disclaimer: This article is educational and all examples and statistics in the article are fictional.

Our Editorial Process

Our expert team uses AI tools to help organize and structure our initial drafts. Every piece is then extensively rewritten, fact-checked, and enriched with first-hand insights and experiences by expert humans on our Insights Team to ensure accuracy and clarity.

About the PaperIndex Insights Team

The PaperIndex Insights Team is our dedicated engine for synthesizing complex topics into clear, helpful guides. While our content is thoroughly reviewed for clarity and accuracy, it is for informational purposes and should not replace professional advice.