📌 Key Takeaways

The warehouse is full, but the bank account is empty—a pattern that quietly destroys working capital for small packaging converters.

- Lower Unit Price Doesn’t Mean Lower Total Cost: Volume discounts that force you to carry excess inventory for months often generate holding costs—storage, handling, insurance, degradation, and financing—that exceed the initial savings, turning an apparent bargain into a net loss.

- Full Warehouses Create Cash Traps, Not Security: Excess kraft paper inventory increases financial risk through demand shifts, specification changes, physical damage, and extended cash conversion cycles that leave working capital locked in reels instead of available for payroll, taxes, and opportunities.

- High MOQs Are Design Choices, Not Fixed Laws: While mills and large traders have genuine production constraints, small converters retain strategic flexibility through supplier diversification, adjusted order cadence, and relationship-building that balances unit cost against cash availability.

- Holding Costs Accumulate Invisibly But Relentlessly: Annual inventory carrying costs for SME operations typically range from the mid-teens to 30% of inventory value, encompassing facility expenses, labor, insurance, product degradation, and the opportunity cost of capital that could fund growth or provide a financial buffer.

- Cash Flow Timing Matters More Than Invoice Price: The critical question before every large order isn’t “What’s the cost per ton?” but “What will this do to my available cash for the next three to six months?”—because working capital health depends on the cash-to-cash cycle, not just purchase price.

Strategic purchasing decisions require balancing three objectives simultaneously: competitive pricing, operational flexibility, and healthy working capital.

SME packaging paper converters and procurement managers will gain practical frameworks here, preparing them for the detailed financial analysis and diagnostic tools that follow.

The warehouse is full. Twenty pallets of kraft paper reels stacked three high, representing a solid month of production capacity. The purchase order felt smart when you signed it—a 10% volume discount that would trim margins and improve competitiveness. But now, six weeks later, you’re staring at a tax bill and wondering which supplier payment to delay because the bank balance doesn’t match the inventory value sitting on your warehouse floor.

For SME packaging converters, this moment repeats itself with uncomfortable frequency. The promise of lower unit prices drives purchasing decisions that make sense on paper but quietly suffocate working capital in practice. You’re carrying more stock than your cash flow can comfortably support, and every extra week those reels sit idle stretches the gap between cash out and cash back in.

This is inventory overload. It’s not about having materials ready for production—that’s necessary and smart. It’s about the structural mismatch between minimum order quantities imposed by suppliers and the financial capacity of small converting operations. The result is a cash trap that feels invisible until you’re scrambling to meet payroll while standing in a warehouse full of paper.

What “Inventory Overload” Looks Like for SME Packaging Converters

Inventory overload occurs when you’re carrying more months of stock than your business can fund without straining other financial obligations. It’s the gap between what your production schedule requires and what you purchased to unlock a price break or satisfy a supplier’s minimum order quantity.

At its core, this is a working capital problem. Working capital represents the difference between current assets—cash, receivables, and inventory—and current liabilities like short-term payables and obligations. It measures how easily a business can cover day-to-day expenses. When too much capital becomes locked in slow-moving inventory, the cushion available for payroll, taxes, and supplier payments shrinks rapidly.

Consider a converter running a small operation with consistent monthly consumption of kraft paper. Under normal circumstances, an adequate stock buffer for production planning and customer fulfillment is determined by the intersection of your supplier lead times, demand predictability, and financial capacity. For many converters, this translates to carrying enough material to cover immediate production needs plus a reliable safety margin. But when a kraft paper supplier requires a minimum order of three months’ consumption to access competitive pricing, the equation changes fundamentally.

You place the order because the alternative—paying a premium for smaller quantities—feels financially irresponsible. The reels arrive, the warehouse accommodates them, and production continues as planned. But two months later, when quarterly tax payments come due or a key piece of equipment needs urgent repair, the cash that should be available for these obligations is instead locked in paper that won’t convert to finished goods and revenue for another four to six weeks.

The warehouse looks healthy and operational. The cash position tells a different story. Both conditions exist simultaneously, and the gap between them represents working capital under pressure.

This pattern directly affects the cash conversion cycle—the time between paying suppliers and receiving cash from customers. When stock sits longer than anticipated, the cycle stretches, and working capital becomes increasingly constrained. Understanding how inventory days and payment terms interact to stretch this cycle reveals the full picture of working capital strain in small converting operations.

Myth #1: Bigger Orders Always Improve Profitability

Myth: Increasing order volume to secure lower unit pricing automatically improves overall profitability and business health.

Reality: Unit cost represents only one component of total cost. Volume discounts reduce the price paid per ton, but holding excess inventory creates a second category of expenses that often exceed the initial savings.

The typical calculation focuses exclusively on the purchase price. Compare two straightforward scenarios:

Option A: Order 20 tons at $1,000 per ton = $20,000 total Option B: Order 40 tons at $950 per ton = $38,000 total

The discount appears compelling. You save $50 per ton across 40 tons, generating $2,000 in apparent savings compared to placing two separate 20-ton orders. The unit economics look favorable, and the decision seems obvious.

What this calculation omits is the cost of holding that additional 20 tons for the months before production actually needs it. Holding costs—also called inventory carrying costs—represent the combined expense of storing and maintaining inventory, including warehousing, handling, insurance, damage, shrinkage, and the cost of capital tied up in stock. These expenses accumulate across multiple categories and compound over time.

Storage and facility costs exist whether you lease warehouse space or own it outright. Leased facilities charge directly for square footage. Owned facilities carry opportunity costs—the productive use that space could serve if it weren’t occupied by excess stock—plus ongoing depreciation, utilities, and maintenance expenses allocated across the inventory footprint.

Handling and internal logistics consume labor time. Moving reels to accommodate new shipments, reorganizing stock for efficient picking, tracking inventory locations, conducting cycle counts—these operational tasks scale with inventory volume and represent real labor costs that could be deployed elsewhere in the operation.

Insurance and loss prevention increase proportionally with inventory value. Higher stock levels raise insurance premiums. They also increase exposure to shrinkage from minor damage during handling, environmental issues like moisture intrusion, or losses from theft or misplacement in larger warehousing operations.

Product degradation and obsolescence accelerate with time. Kraft paper exposed to humidity fluctuations can develop quality issues. Customer specification changes can render entire stock batches obsolete or force significant discounting to move material that no longer matches current demand. The longer paper sits, the higher these risks become.

Financing costs take multiple forms. If you’re using a line of credit to fund purchases, interest charges accumulate monthly on the borrowed amount. If you’re straining cash flow by purchasing more than needed, you might delay payments to other suppliers, potentially incurring late fees or damaging relationships. Even without explicit borrowing, the opportunity cost of capital tied up in slow-moving inventory represents a financing burden.

Return to the scenario above. That extra 20 tons—the difference between Option A and Option B—represents $18,000 in additional capital tied up in inventory. If those reels sit for six months before being used, and your annual carrying costs fall in the mid-teens or higher as a percentage of inventory value—common for SME operations with limited space and higher financing costs—the holding expenses can easily consume most or all of that $2,000 discount.

Meanwhile, that $18,000 remains unavailable for sales activities, machinery maintenance, tax payments, or responding to unexpected opportunities. The warehouse is fuller, but the business isn’t more profitable. The lower unit price becomes irrelevant when the total cost increases.

How the Unit Price vs. Holding Cost Infographic Should Work:

The central visual for this article should make this trade-off immediately obvious. One bar shows the one-time savings from the bulk discount—in this case, $2,000. Adjacent bars show cumulative holding costs if the extra stock sits for one month, three months, and six months. The viewer should be able to identify the exact point where the holding cost bar overtakes the discount bar and realize: “From here onwards, the discount is gone. Now this stock is actively costing money.”

This visual representation often proves more powerful than formulas or abstract percentages. It transforms the concept from theory into something tangible that can be screenshot, printed, and discussed in team meetings or budget reviews.

The principle applies broadly: discounts that require carrying inventory beyond your normal operating buffer must be evaluated against the full cost of holding that stock. When holding costs exceed the discount, the transaction destroys value rather than creating it.

Myth #2: Full Warehouses Mean You Are “Safe”

Myth: Maintaining high inventory levels protects the business from supply disruptions and provides security against demand fluctuations.

“A full warehouse can be a cash trap disguised as security.”

Reality: Excess stock increases financial and operational risk rather than mitigating it.

A warehouse stocked with several months of kraft paper creates psychological comfort. Supply concerns vanish. Lead time pressures ease. The ability to fulfill customer orders without coordination stress feels like operational strength. But this perceived safety masks several categories of risk that compound over time.

Demand patterns shift without warning. A major customer reduces order volume due to their own market conditions. Another customer switches product specifications, rendering a portion of your carefully stocked inventory mismatched to current requirements. Market trends move toward different grades or weights of paper. Each of these scenarios—common in small converting operations serving diverse customers—transforms “adequate stock” into “excess inventory” overnight.

Specification changes create immediate obsolescence. When a customer who represents 30% of your monthly volume decides they need a different basis weight or finish, the reels purchased specifically for their orders become problem stock. You’ll either discount heavily to move the material to other customers, accept lower margins, or potentially write it off entirely. The cash invested in that inventory doesn’t return as planned, and the working capital impacts compounds.

Physical risks accumulate with storage duration. Handling damage increases with every movement and reorganization of stock. Environmental exposure—temperature swings, humidity fluctuations, dust accumulation—creates quality degradation that worsens over months. Minor losses from mishandling or misplacement become statistically more likely with larger inventory volumes and longer hold times.

Cash conversion cycle extension represents the most significant risk. Every week that paper sits in your warehouse waiting for production and sale is another week your cash remains locked and unavailable. You’ve already paid the supplier, but you won’t receive payment from your customer for weeks or months. During that gap, you still need to cover payroll, tax obligations, utility bills, equipment maintenance, and other supplier invoices. The mismatch between cash out and cash in creates constant pressure on working capital.

High minimum order quantities that force overbuying directly threaten business liquidity and operational resilience. Cash locked in excess reels cannot respond to emergencies, cannot fund equipment repairs, cannot capitalize on unexpected opportunities, and cannot provide the financial buffer that small businesses need to navigate market volatility.

The warehouse might look strong and secure, but if the bank balance is tight and cash flow is stressed, the business is operating in a fundamentally vulnerable position. Security built on excess inventory is an illusion when working capital is constrained.

Myth #3: High MOQs Are Just the Cost of Doing Business

Myth: Minimum order quantities represent immutable constraints that converters must accept without question as a basic condition of participating in the kraft paper supply chain.

Reality: MOQs reflect genuine structural constraints on the supply side, but SME converters retain significant agency in how they respond to these requirements.

Paper mills operate at scale because efficiency demands it. Production runs measured in hundreds of tons make economic sense for large manufacturing facilities. Asking a mill to produce a custom order of five tons disrupts their operations and creates unit economics that don’t work for either party. Similarly, large traders consolidate volume to negotiate favorable terms with mills, and they pass MOQ requirements downstream to maintain their own operational efficiency. These are real constraints embedded in supply chain structure, not arbitrary policies designed to inconvenience small kraft buyers.

However, accepting every MOQ at face value without examining its impact on your working capital represents a strategic choice—and often an expensive one. When you routinely agree to minimum orders that force you to purchase three or four months of inventory to access competitive pricing, you’re making an implicit decision that lower unit cost matters more than cash availability.

Small converters have more flexibility than they often recognize. Diversifying your supplier mix can reduce dependence on any single source with particularly restrictive MOQs. Some regional distributors, smaller traders, and specialty suppliers specifically serve SME converters and structure their offerings around smaller, more frequent orders. These sources might carry slightly higher unit costs, but when evaluated against reduced holding costs and improved cash flow, the total cost equation can actually favor the smaller order approach.

Order cadence adjustment offers another lever. Rather than placing large quarterly orders to maximize discounts, some converters find better results with smaller monthly orders that track more closely to actual consumption. The per-unit price might increase modestly, but the working capital benefits—reduced inventory carrying costs, better cash flow predictability, lower storage requirements—can outweigh the price differential.

Strategic supplier relationships matter. Mills and large traders operate in a competitive environment. When you approach negotiations with clear data about your consumption patterns, payment reliability, and willingness to commit to volume over time through smaller, more frequent orders, some suppliers will accommodate. The conversation shifts from “take it or leave it” MOQs to genuine discussions about structuring supply arrangements that work for both parties.

The objective isn’t to eliminate MOQs entirely—that’s neither realistic nor necessary. The objective is to recognize that blindly accepting every MOQ without evaluating its working capital impact creates a pattern of overbuying that quietly damages financial health. Better sourcing strategy balances unit cost, order flexibility, and cash flow impact rather than optimizing solely for the lowest price per ton.

How to See the True Cost of Inventory on Your Balance Sheet

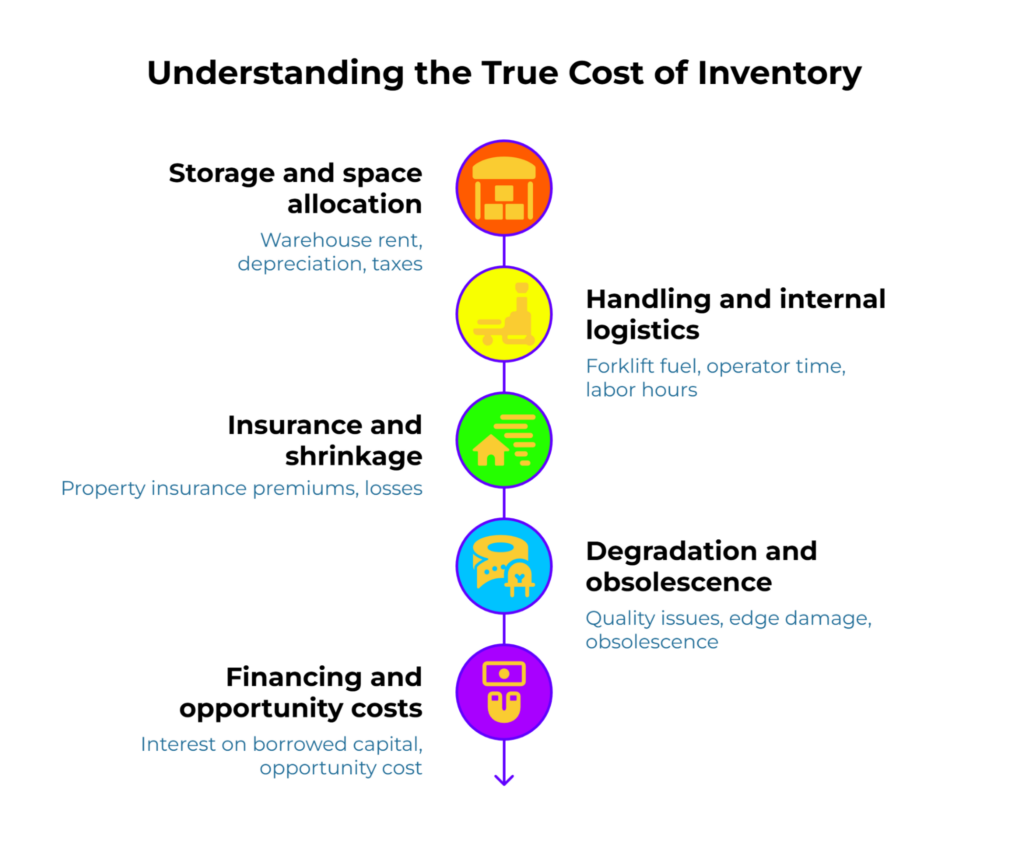

Inventory carries a “monthly rent” that many converters don’t explicitly calculate. Even when you own your warehouse and storage space feels free, holding stock still incurs real costs that accumulate over time. Understanding these costs transforms how you evaluate purchasing decisions and makes it possible to distinguish between genuinely valuable discounts and transactions that look good on paper but destroy value in practice.

Holding costs—the combined expense of storing and maintaining inventory—encompass warehousing, handling, insurance, damage, shrinkage, and the cost of capital tied up in stock. When properly accounted for, these costs typically fall into five categories, each representing actual cash expenditure or opportunity cost:

Storage and space allocation: If you lease warehouse facilities, the cost shows up directly in monthly rent charges. If you own your building, the cost takes the form of depreciation, property taxes, insurance on the structure, utilities allocated to storage areas, and maintenance expenses. There’s also opportunity cost—space occupied by excess inventory could potentially be used for additional production capacity, improved workflow organization, or other value-generating activities.

Handling and internal logistics: Moving reels requires forklifts, fuel, and operator time. Reorganizing stock to accommodate new shipments takes labor hours. Tracking inventory locations, conducting cycle counts, investigating discrepancies—these operational necessities scale with inventory volume. The labor and equipment costs are real, and they increase proportionally with the amount of stock you’re managing.

Insurance and shrinkage: Property insurance premiums for inventory scale with the value you’re carrying. Higher stock levels mean higher premiums. Additionally, larger inventory volumes create more opportunities for loss through minor handling damage, environmental exposure, administrative errors, or occasional theft. These losses might seem small individually, but they compound over time and represent real financial impact.

Degradation and obsolescence: Kraft paper exposed to humidity can develop quality issues. Reels stored for extended periods face increased risk of edge damage, contamination, or quality drift. Customer specification changes can render entire batches obsolete or force heavy discounting to move material that no longer matches current demand. The longer inventory sits, the higher the probability of one of these loss events occurring.

Financing and opportunity costs: If you’re using borrowed capital—a line of credit, term loan, or delayed supplier payments—to fund inventory purchases, you’re paying interest on that capital for as long as the inventory remains unsold. Even if you’re not explicitly borrowing, capital tied up in slow-moving inventory represents an opportunity cost. That cash could be deployed elsewhere: equipment upgrades that improve efficiency, marketing initiatives that generate new customers, or simply held as a buffer against unexpected expenses.

When these categories are summed, total holding costs for inventory-intensive businesses typically represent a substantial percentage of inventory value annually. For SME operations, these costs often fall at the higher end of industry averages due to less optimized logistics, limited economies of scale, and the higher financing or opportunity cost of capital tied up in stock.

The practical takeaway: before committing to any large order driven by volume discounts, estimate holding costs and compare them to the savings. A simple rule of thumb suffices: if you’re buying more than two months’ extra inventory to capture a discount, calculate roughly what it costs to hold that excess stock for the time it will sit in your warehouse, then compare that cost to the discount received. If the numbers don’t clearly favor the discount, the transaction probably doesn’t make financial sense regardless of how attractive the unit price looks.

Quick Self-Check: Are You in Inventory Overload Right Now?

Take five minutes to assess your current inventory position with these diagnostic questions. Answer honestly based on your actual operational experience over the past six months:

Are you regularly carrying more than three months of kraft paper stock based on your normal consumption rate?

If production typically uses 10 tons monthly and you’re routinely sitting on 35 to 40 tons, you’re carrying excess inventory driven by purchasing patterns rather than operational necessity.

Have you delayed supplier payments, struggled with payroll timing, or postponed equipment maintenance in the past six months while your warehouse was still full of paper?

This mismatch—tight cash despite full inventory—is the clearest signal of working capital strain caused by overbuying.

Do you have reels in your warehouse that you mentally categorize as “slow-moving,” “problem stock,” or “leftover from that order”?

These labels indicate inventory that isn’t aligned with current production needs and represents cash locked in material that isn’t generating revenue.

Does more than 30% of your warehouse floor space feel occupied by stock that isn’t moving through production within a six-week cycle?

Physical space is a proxy for capital allocation. If a third of your facility is devoted to storing paper that isn’t actively converting to finished goods, working capital is being consumed by inventory holding rather than production.

Have you turned down a new customer opportunity, delayed investing in equipment that would improve efficiency, or avoided pursuing a promising business development lead specifically because you didn’t have available cash despite having substantial paper inventory on hand?

This scenario reveals the opportunity cost of inventory overload: capital trapped in stock becomes unavailable for activities that could grow or strengthen the business.

Has your cost of financing—whether explicit interest payments, overdraft fees, or penalties for delayed payments—increased over the past year while your production volume has remained stable or grown only modestly?

Rising financing costs without corresponding revenue growth often indicates that working capital is under pressure, and excess inventory is frequently the cause.

If you answered yes to two or more of these questions, inventory overload is likely affecting your working capital and constraining your operational flexibility. This isn’t an indictment of management capability or planning skill. It’s a structural pattern created by the interaction between supplier MOQs, volume discount incentives, and the financial realities of running a small converting operation.

Recognizing the pattern makes it possible to adjust purchasing strategy, evaluate suppliers differently, and prioritize cash flow health alongside unit cost optimization in your decision-making.

Shift Your Buying Criteria from Unit Price to Cash Flow

The quiet threat to working capital in SME packaging conversion isn’t primarily the price of kraft paper on invoices—it’s the inventory overload created by minimum order quantities and volume discount structures that encourage buying beyond operational needs.

Unit price matters. Competitive margins require careful cost management, and securing favorable pricing on raw materials is part of that discipline. But unit price represents only part of the total cost equation. The other part—often invisible in standard purchasing analysis—is the cost of holding inventory and the impact on working capital of having cash locked in stock rather than available for other business needs.

Before placing your next significant order, ask one diagnostic question: “What will this order do to my available cash over the next three to six months?”

If the answer is that it will consume cash you might need for payroll, quarterly taxes, equipment maintenance, or responding to unexpected opportunities, then the volume discount driving the purchase decision deserves careful scrutiny. The lower unit price might not compensate for the working capital strain and financial inflexibility it creates.

Effective sourcing strategy for small converters balances three objectives simultaneously: competitive unit costs, operational flexibility, and healthy working capital. This doesn’t mean ignoring price or accepting uncompetitive cost structures. It means recognizing that a modestly higher unit price paired with smaller order quantities, better payment terms, or faster inventory turnover can sometimes deliver better total financial outcomes than relentlessly pursuing the absolute lowest price per ton.

The cash-to-cash cycle—the time from when you pay a supplier to when you receive payment from your customer—drives working capital health more directly than any single purchase price. Orders that stretch this cycle by forcing you to carry months of excess inventory damage working capital even when the unit economics look favorable.

For a complete understanding of how inventory days interact with payment terms to affect your cash conversion cycle, this detailed guide on working capital strain from payment terms provides the framework for mapping when cash leaves your business and when it returns. Understanding both dimensions—how long inventory sits and how payment timing works—gives you the visibility needed to make sourcing decisions that genuinely strengthen financial position rather than just reducing line items on purchase orders.

Additional practical guidance on managing working capital, optimizing sourcing strategy, and building financial resilience in small converting operations is available through PaperIndex Academy, where in-depth educational resources address the specific operational and financial challenges faced by SME packaging converters.

Disclaimer: This article provides general educational guidance about working capital management and inventory strategy. It is not personalized financial advice. Each converter’s financial situation, supplier relationships, and market context differs. Business owners should consult qualified financial advisors when making significant purchasing or financing decisions.

Our Editorial Process

Our expert team uses AI tools to help organize and structure our initial drafts. Every piece is then extensively rewritten, fact-checked, and enriched with first-hand insights and experiences by expert humans on our Insights Team to ensure accuracy and clarity.

About the PaperIndex Insights Team

The PaperIndex Insights Team is our dedicated engine for synthesizing complex topics into clear, helpful guides. While our content is thoroughly reviewed for clarity and accuracy, it is for informational purposes and should not replace professional advice.