📌 Key Takeaways

A 15-day shift in payment terms can free tens of thousands in trapped working capital—or quietly tighten the cash squeeze until month-end becomes a crisis.

- Payment Terms Are Design Levers, Not Fixed Rules: Kraft paper payment terms with suppliers and customers can be negotiated to shrink the cash gap, reducing overdraft dependence without complex financial engineering.

- The Terms-Driven Cash Gap Formula Reveals Hidden Costs: Subtracting supplier payment days from customer payment days shows exactly how many days your cash is locked up funding someone else’s operations—and converting that gap to rupees or dollars makes the real cost visible.

- Small Moves on Both Sides Beat Big Wins on One: Nudging supplier terms from 30 to 45 days while moving customer terms from 90 to 60 days can cut working capital needs by 75%, compared to negotiating aggressively with only suppliers or only customers.

- Simple Scenario Tables Enable Real Negotiations: Side-by-side comparisons showing the same monthly kraft paper spend under different term combinations (30/90 vs 45/60) turn abstract finance discussions into concrete, printable tools for owner meetings, supplier calls, and customer conversations.

- The Stress Point is Predictable and Fixable: When overdraft limits stay near maximum, mills call about late payments, and profitable orders feel risky, the root cause is often a 45-to-60-day payment-terms gap that can be systematically narrowed through small, realistic adjustments.

Prepared finance and procurement teams can use these mini-scenarios the same day they read them—no complex models required.

Finance, procurement, and sourcing leaders at SME packaging converter companies will find a practical framework here, preparing them for the detailed payment terms strategy and working capital mapping that follows.

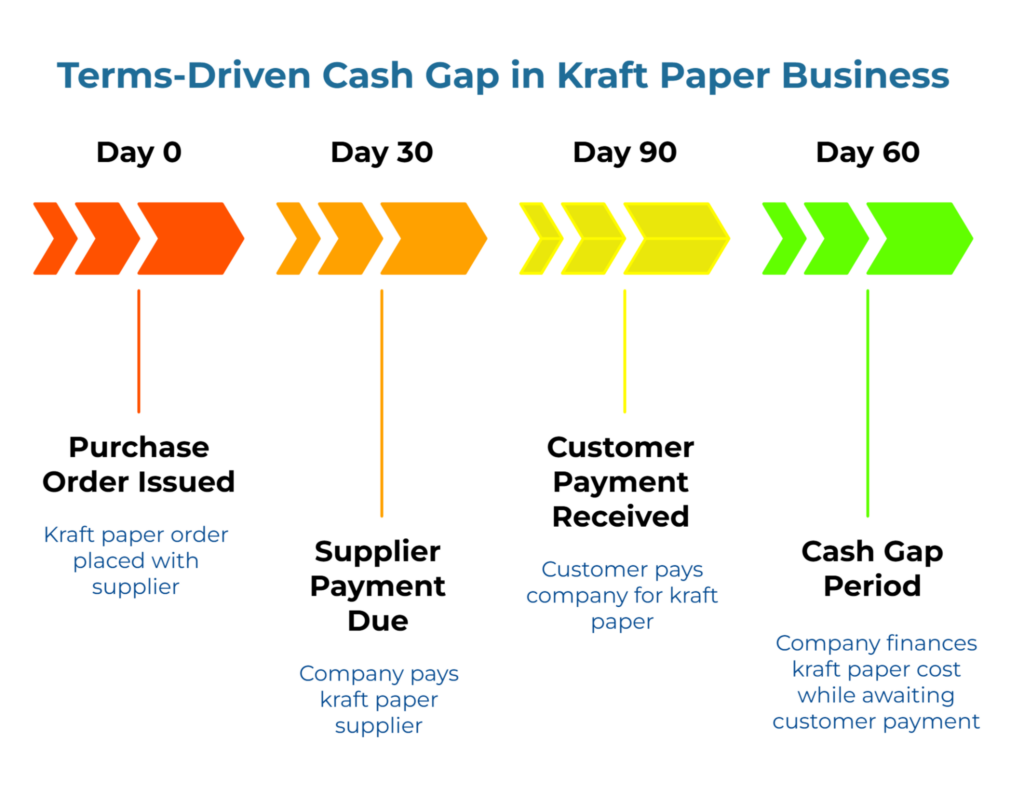

The mill sends a new contract. Payment terms: 30 days instead of your usual 45. Your first thought is probably “that’s just 15 days—how bad can it be?” But when you sit down with your finance team at month-end, overdraft is maxed out, and there’s a kraft paper order due tomorrow that you can’t quite cover.

Payment Terms Design for Kraft Paper Suppliers & Customers is the process of structuring, negotiating and enforcing payment terms with kraft paper suppliers and end customers so that inflows and outflows of cash are better aligned and less dependent on emergency financing. It is like adjusting the gears on a bicycle so your legs, chain and wheels move in sync instead of fighting each other. After mapping their terms, a converter nudges key customers from 90 to 60 days, secures 45-day terms with a core supplier and finds that month-end cash feels much more manageable. Practically, readers start by listing their current terms, spotting the worst gaps and planning one small improvement conversation on each side of the chain.

This article walks through simple mini-scenarios that show exactly how a 15-day change in supplier or customer payment terms affects your cash gap. You’ll see side-by-side comparisons using the same monthly kraft paper spend but different term combinations. By the end, you’ll have a practical tool you can print, share with your owner or CFO, and use in actual negotiations the same day.

Why 15 Days in Payment Terms Matter More Than They Look

Most packaging converters treat payment terms as fixed constraints. The kraft paper mill says 30 days, customers demand 90, and finance juggles overdraft to bridge the gap. But payment terms are actually a financial design lever—often as negotiable as price—that you can adjust on both sides of your supply chain to optimize liquidity.

In B2B relationships, terms like Net 30, Net 45, or Net 60 represent standard trade credit arrangements. These terms specify when invoices are due and effectively determine who finances the working capital during the transaction cycle. Longer customer payment terms give kraft paper buyers more time to pay, but they also keep cash locked in receivables and shift the financing pressure back onto suppliers and small converters.

Here’s why 15 days matters: working capital strain from payment terms happens when you consistently pay kraft paper suppliers earlier than customers pay you. This creates a cash gap measured in both days and actual rupees or dollars. Even a modest 15-day shift in supplier terms or customer terms can meaningfully change how much cash or overdraft you need to keep operations moving.

Small businesses feel this pressure more acutely. When a supplier tightens terms from 45 to 30 days, you’re suddenly funding kraft paper inventory 15 days earlier. If your monthly kraft paper spend is ₹30 lakh (roughly $36,000), that 15-day change ties up an extra ₹15 lakh in working capital. For a converter already near its overdraft limit, that’s not a minor inconvenience—it’s a crisis that triggers late payments, strained supplier relationships, or rejected orders.

The hidden leverage lies in the fact that both sides of the equation are negotiable. You can’t always get mills to extend terms, but you can often negotiate modest improvements with secondary suppliers or push back gently on customers who treat 90-day terms as non-negotiable. Research from Intuit QuickBooks on small business cash flow shows that longer customer payment times and late payments are strongly associated with cash flow problems and force SMEs to rely more heavily on short-term credit to bridge gaps.

The Cash Gap in Days: A Simple Picture

The Terms-Driven Cash Gap is the specific structural mismatch between your payment outflow and collection inflow, representing the days you must finance a transaction solely because customer terms exceed supplier credit. It’s the period during which your cash is locked up funding someone else’s operations.

In working capital management, three timing elements drive the overall cycle:

Days Payable Outstanding (DPO): How long you have to pay mills or traders—this represents the trade credit you receive from suppliers.

Days Inventory Outstanding (DIO): How long kraft paper typically sits in inventory before it’s converted and invoiced to customers.

Days Sales Outstanding (DSO): How long customers take to pay you after you invoice them. (DSO) measures the average number of days it takes for a company to collect payment after a sale has been made.

Together, these components form the Cash Conversion Cycle (CCC), which indicates how long cash is tied up in operations before it returns as collections. The formula links DSO, DIO, and DPO to show the complete working capital picture.

For the purposes of isolating the impact of payment terms negotiations, we can calculate what we’ll call the Terms-Driven Cash Gap. Provided you do not increase your inventory levels (e.g., buying bulk to get better terms), the gap determined specifically by payment terms is:

Terms-Driven Cash Gap (days) = Customer Payment Days – Supplier Payment Days

If your customers pay in 90 days and you pay kraft paper suppliers in 30 days, your payment-terms gap is 60 days. During those 60 days, you’re carrying the cost of that kraft paper on your books, funding it through working capital or overdraft.

To estimate the average working capital requirement, multiply your average daily kraft paper spend by the cash gap. If you spend ₹30 lakh per month on kraft paper, your daily spend is roughly ₹1 lakh. A 60-day cash gap means ₹60 lakh is always tied up in the payment cycle. That’s cash you can’t use for other orders, equipment maintenance, or growth opportunities.

How This Gap Shows Up as Overdraft Stress

A larger gap in days directly increases the average amount of working capital tied up in kraft paper (accruing interest costs) and the duration that credit lines stay near their limits, reducing liquidity for emergencies.

For the converter, this feels like:

Living with a permanent overdraft balance that never fully clears, even during slower months.

Tense calls from mills or traders when payments run a few days late because the customer payment hasn’t arrived yet.

Internal debates about whether to accept a profitable order because the timing might break the working capital shock absorber and push you over the bank limit.

Month-end becomes a high-stress event where you’re constantly calculating which supplier can wait an extra week and which customer needs a polite reminder call to prevent a cash crisis.

This framework helps you see payment terms not as abstract contract clauses but as direct controls on your cash flow. When a supplier proposes tighter terms or a customer pushes for longer terms, you can immediately calculate the cash impact and decide whether the trade-off makes sense.

Mini-Scenarios: How 15 Days Change Your Cash Gap

Let’s make this concrete with three scenarios using the same monthly kraft paper spend. The only variables that change are supplier payment days and customer payment days.

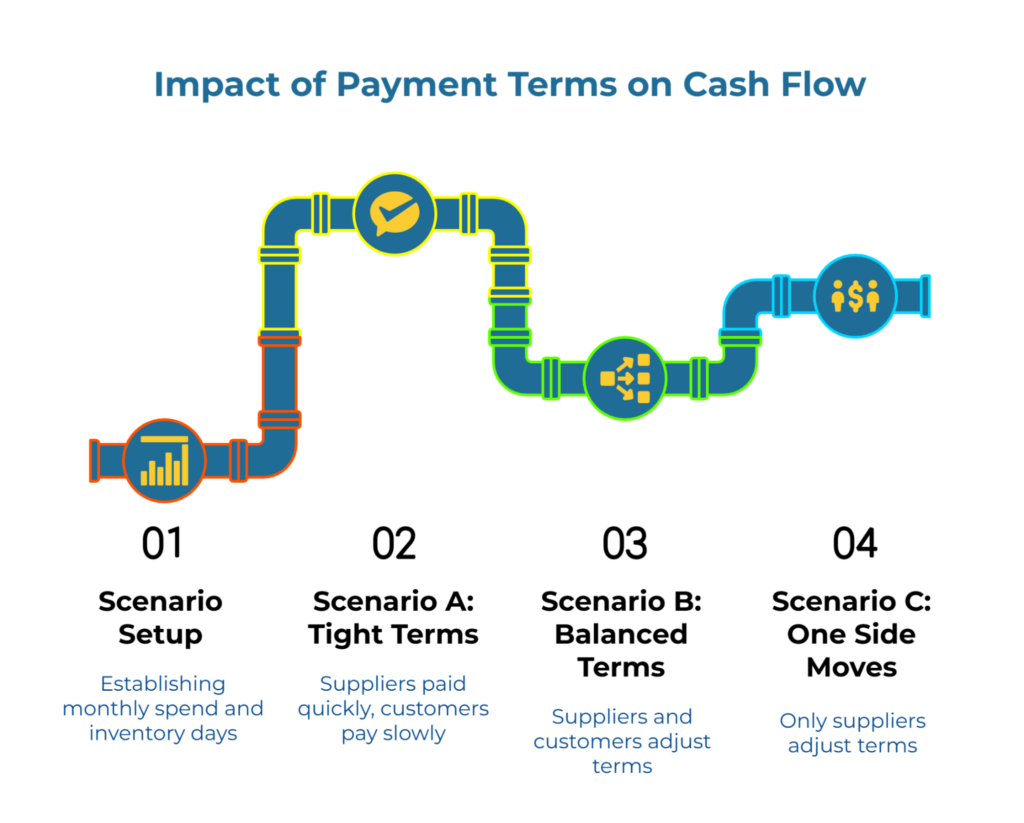

Scenario Setup: Same Monthly Spend, Different Term Combinations

For all three scenarios, assume:

- Monthly kraft paper spend = ₹30 lakh ($36,000)

- Inventory days remain constant

- Only supplier days and customer days change

To estimate the working capital impact, we use this simplified proxy: Approximate cash locked ≈ (Terms-Driven Gap ÷ 30) × Monthly Spend. These are rounded, illustrative examples designed to show direction and scale, not precise finance-model outputs.

| Scenario | Supplier Days | Customer Days | Cash Gap (Days) | Approximate Cash Tied Up |

| Scenario A: Tight Terms | 30 | 90 | 60 | ₹60 lakh ($72K) |

| Scenario B: Balanced Terms | 45 | 60 | 15 | ₹15 lakh ($18K) |

| Scenario C: One Side Moves | 45 | 90 | 45 | ₹45 lakh ($54K) |

Scenario A: Tight Terms (The Stressful Baseline)

In this scenario, you pay suppliers fast (30 days) but customers pay slowly (90 days). The 60-day cash gap means ₹60 lakh—roughly two months of kraft paper spend—is always locked in the payment cycle.

This is the classic working capital squeeze that many small converters face by default. Kraft paper suppliers want money about one month after dispatch, while large customers take about three months to pay. The converter is effectively financing two months’ worth of kraft paper spend from internal cash or overdraft.

Month-end under Scenario A often feels like:

- Overdraft limit almost always near the ceiling

- Pressure to slow down payments to smaller suppliers to preserve cash

- Nervousness about accepting incremental orders, even when profitable, because the cash gap is already wide

- Constant mental math about which payments can be delayed without damaging key relationships

Scenario B: Balanced Terms (Negotiated Improvement)

Now imagine nudging both sides by 15 days in your favor. Suppliers agree to 45 days, and you’ve successfully moved key customers from 90 to 60 days.

The cash gap shrinks dramatically from 60 days to just 15 days. Cash locked in kraft paper falls from ₹60 lakh to ₹15 lakh—a difference of ₹45 lakh freed up for other uses.

In many converters, this shift is the difference between running permanently at the edge of the bank limit versus having room to absorb a large new order without panic. Month-end conversations with your bank become calmer. You can say yes to growth opportunities without immediately checking the overdraft balance.

Scenario C: One Side Moves (Partial Progress)

In reality, sometimes only one side agrees to move. Perhaps you successfully negotiate 45-day terms with suppliers, but customers remain firm on 90 days.

The gap narrows from 60 to 45 days. Cash locked drops from ₹60 lakh to ₹45 lakh. While not as dramatic as Scenario B, this still frees up ₹15 lakh in working capital.

This scenario shows two important points: Moving just one side still helps meaningfully, and moving both sides a little is often better than waiting for one perfect negotiation. The combination in Scenario B (45/60) is far safer than either extreme on its own.

Using These Scenarios in Real Conversations

The mini-scenarios are designed as a conversation prop, not a theoretical model. You can print the table, walk into a meeting, and show exactly what different term combinations mean in cash terms.

With Your Owner or Management Team

Use the 30/90 versus 45/60 comparison to shift the conversation from “this is how the industry works” to “this is what 15 days does to our cash gap.” Keep the language in days and rough cash multiples rather than technical jargon. Position payment terms design as a way to protect the business’s oxygen—cash—while still serving key customers.

If a more detailed explanation of the overall cash flow gap is needed, share the core explainer on working capital strain from payment terms alongside this article.

With Suppliers

When speaking to mills or traders, show that the request isn’t about squeezing them but about aligning gears so both sides can grow without constant emergencies. Use simple language: “If we can move from 30 days to 45 days with you, it cuts our cash gap by half a month. That makes it easier for us to keep growing our kraft paper volumes with you safely.”

If helpful, reference your broader mapping from the cash conversion cycle article to show you understand the full picture.

With Key Customers

When negotiating with large customers, explain that 90-day terms push the working capital burden back up the chain and increase the risk of supply disruptions. Use the scenarios to illustrate a compromise: “Moving from 90 days to 60 days shrinks the gap by a full month. That gives us more headroom to keep supplying you reliably, even when orders spike.”

Frame the request as joint risk management, not a complaint. Over time, these conversations help reposition the converter as a trusted partner managing shared risk, rather than a small buyer asking for exceptions.

What to Do Next After Seeing Your Own Numbers

List, Compare, Then Design Your Next Small Move

A simple sequence to put this into practice:

List your top three kraft paper suppliers and top three customers, with current terms (supplier days, customer days). Write them down in a simple table.

Compute the approximate cash gap in days for the main supplier-customer pairs using the formula from earlier. This becomes your baseline—your own Scenario A.

Pick one move on each side of the chain where a 15-day improvement looks both meaningful and realistic. Focus on your most flexible supplier or your newest customer relationship where terms haven’t solidified yet.

Prepare the conversation using scenario-style language rather than technical finance language. Frame it around mutual benefit—suppliers might extend terms in exchange for committed volume, and customers might accept shorter terms in exchange for priority scheduling or volume discounts.

Track the impact monthly. After making even one term adjustment, calculate your new cash gap and monitor how it affects month-end stress. Small wins build confidence and give you proof points for harder conversations later.

Where This Fits in the Bigger Payment Terms Playbook

For converters ready to take a more systematic approach, the full payment terms design playbook walks through a complete alignment strategy covering supplier negotiation tactics, customer communication frameworks, and internal finance alignment.

If you want to understand how inventory days interact with payment terms, the inventory days and overdraft stress guide provides the complete picture. For converters wondering how much working capital they actually need once terms are optimized, the working capital limit calculation guide turns cash gaps into bank-ready numbers.

Resource

- Working Capital Strain from Payment Terms: A Simple Guide to Seeing and Fixing Your Kraft Paper Cash Flow Gap

- Working Capital Strain from Payment Terms: Inventory Days, Overdraft Stress, and How Much Cash Is Stuck in Kraft Paper

- Corporate Finance Institute: Cash Conversion Cycle

- Investopedia: Days Sales Outstanding

- Wikipedia: Net D Trade Credit Terms

- Intuit QuickBooks: Small Business Cash Flow Management

From Stress to Strategy

Month-end doesn’t have to feel like a crisis. The mini-scenarios in this article show that small, realistic changes in kraft paper payment terms—often just 15 days—can materially reduce the cash gap that drives overdraft stress. You’re not stuck with the terms you inherited. Supplier-customer payment terms alignment is a design lever, not a fixed constraint.

Print the scenario table. Share it with your finance team. Use it in your next supplier or customer conversation. The math is simple, the conversations are straightforward, and the relief at month-end is real.

Disclaimer: This article is for educational purposes only. Payment terms and working capital management should be discussed with qualified financial advisors and tailored to your specific business circumstances.

Our Editorial Process

Our expert team uses AI tools to help organize and structure our initial drafts. Every piece is then extensively rewritten, fact-checked, and enriched with first-hand insights and experiences by expert humans on our Insights Team to ensure accuracy and clarity.

About the PaperIndex Insights Team

The PaperIndex Insights Team is our dedicated engine for synthesizing complex topics into clear, helpful guides. While our content is thoroughly reviewed for clarity and accuracy, it is for informational purposes and should not replace professional advice.