📌 Key Takeaways

Unit price tells you what the supplier charges—landed cost tells you what you’ll actually pay when folding cartons reach your door.

- Normalize Every Quote to One Basis: Mixed Incoterms make apples-to-oranges comparisons; convert all quotes to the same delivery point before ranking suppliers.

- Name Every Hidden Cost Layer: Freight, duties, port fees, documentation, and defect reserves belong in your worksheet—not as surprises on next quarter’s variance report.

- Log Assumptions With Owners and Dates: When freight rates or duty rules shift, finance needs to know which figures were locked and which were placeholders.

- Budget for Disruption, Not Just Delivery: Quality disputes, documentation errors, and replacement shipments carry real costs that “zero defect” budgets ignore.

- Use a Boring Worksheet Consistently: A calm, repeatable tool beats clever shortcuts—structure prevents the budget from changing shape after suppliers are awarded.

Predictable budgets come from better cost frames, not better guesses.

Procurement managers and finance teams evaluating folding carton suppliers will gain a defensible comparison method here, preparing them for the detailed worksheet structure that follows.

~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

The quarterly budget review is in fourteen minutes. Three folding carton quotes sit on the desk—one EXW Shanghai, another FOB Mumbai, a third showing ‘destination handling included’ but no mention of duty. The unit prices look comparable. But which supplier is actually cheapest?

That question cannot be answered yet. And neither can the spreadsheet.

A to-door metric is the comparison basis that translates a supplier’s quoted price into what the business will actually pay when folding cartons arrive at the receiving dock—freight cleared, duties paid, documentation complete. Think of it like an architectural blueprint: the number becomes trustworthy only when everyone is pricing the same scope on the same basis.

This article is not about predicting market prices. It is about building the decision structure that makes every quote comparable before commitment. The real forecasting failure is rarely bad arithmetic—it is bad comparison architecture. When one supplier quotes EXW and another quietly embeds more of the journey into their price, the procurement team is not comparing suppliers. It is comparing incomplete cost frames.

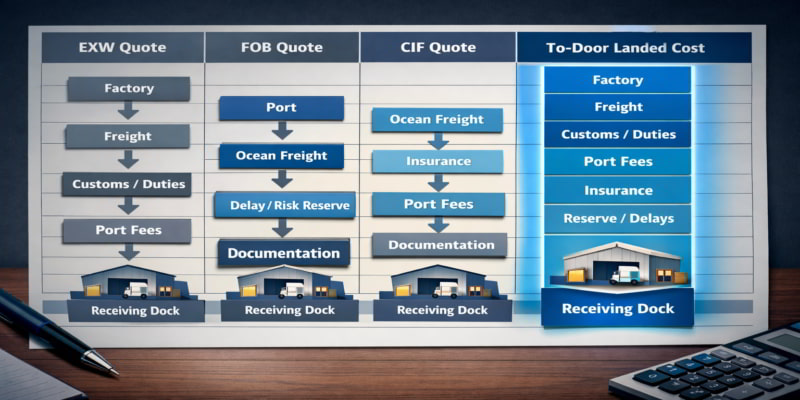

Why Unit Price Breaks the Moment Real Logistics Begin

Unit price looks clean on a spreadsheet. It sits in a single cell, easy to sort, easy to compare. But the moment that folding carton leaves the supplier’s facility, the unit price stops telling the truth.

Unit price excludes everything that happens between the factory gate and the receiving dock, functioning as a partial cost disguised as a complete one. The supplier quoting EXW (Ex Works) is pricing only what sits at their loading bay. For a detailed treatment of how each Incoterm shifts cost responsibility, see incoterms for kraft paper buyers: EXW vs FOB vs CIF vs DDP and what changes in your total cost—the principles apply equally to folding carton procurement. The supplier quoting CIF (Cost, Insurance, and Freight) has bundled ocean transit but left destination handling and customs clearance as buyer responsibilities. Under the ICC Incoterms® 2020 framework, each term allocates risk and cost transfer at a different point—and those differences determine which expenses remain invisible until the invoice arrives.

What exactly is missing when a team budgets from EXW or unit price alone?

The gap is not minor. A unit-price-only approach typically omits origin handling and export clearance (if pricing below FOB), ocean or air freight depending on the shipping mode, marine cargo insurance, destination port charges and terminal handling, import duties and taxes based on product classification under the Harmonized System, inland transportation from port to facility, and documentation costs including inspection or certification requirements.

Each missing layer represents a forecast error waiting to surface. The procurement team that awards business on unit price alone is not saving money. It is deferring cost discovery until the quarterly variance report demands an explanation.

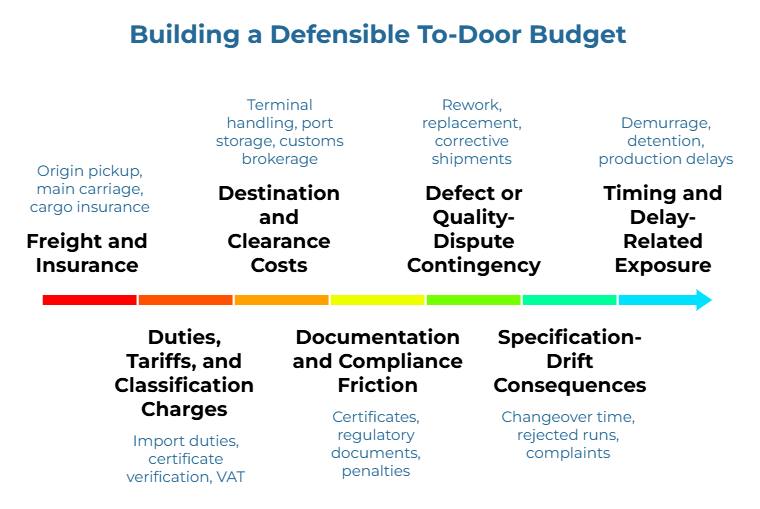

The Hidden Variables a ‘To-Door’ Budget Must Capture

Building a defensible budget means naming every cost layer between the quoted price and the moment folding cartons reach the warehouse. These variables do not disappear when ignored—they surface later, unallocated and unexplained.

Which costs belong in every to-door worksheet, even before a supplier is chosen?

Organize landed-cost variables into seven categories. Even when exact figures are unavailable at the quoting stage, the categories themselves must appear in the worksheet so the team knows what still needs estimating.

Freight and Insurance. This includes origin pickup where applicable, main carriage by sea or air, and cargo insurance. Freight rates fluctuate, so the worksheet should note the quote date and whether the rate is spot or contracted. Insurance calculations typically depend on CIF value, commodity type, route, and coverage terms.

Duties, Tariffs, and Classification Charges. Import duties depend on the product’s HS code classification and the destination country’s tariff schedule. For folding cartons with sustainability claims, certificate verification adds another layer—see the mistake most teams make with green folding cartons (and how verification fixes It). The WTO Tariff & Trade Data portal provides a starting point for checking applied rates, though final duty treatment may vary based on trade agreements, origin certificates, and anti-dumping measures. Value-added taxes or goods-and-services taxes assessed at import also belong here.

Destination and Clearance Costs. Terminal handling charges, port storage fees, customs brokerage, and inspection or fumigation requirements fall into this category. These costs are often quoted in local currency and shift based on port congestion, container dwell time, and seasonal demand.

Documentation and Compliance Friction. Certificates of origin, phytosanitary certificates, conformity assessments, and other regulatory documents carry both direct fees and indirect costs. Delays when paperwork is incomplete, penalties when declarations are incorrect—these friction points multiply when supply chains cross multiple jurisdictions.

Defect or Quality-Dispute Contingency. Even with tight specifications, some portion of shipments may arrive out of tolerance. The underlying issue often traces back to specification clarity—a topic addressed in board grade tolerances explained: securing folding carton specifications across suppliers. The worksheet should include a reserve line for rework, replacement, or expedited corrective shipments. This is realistic forecasting, not pessimism.

Specification-Drift Consequences. When a supplier’s process shifts—different board grade, adjusted caliper, changed coating—the folding cartons may still pass inspection but cause downstream problems on filling lines. For a systematic approach to preventing this drift, see the truth decay of data sheets: why relying on supplier specifications ruins folding carton specifications. The cost of specification drift shows up in changeover time, rejected runs, and customer complaints, not in the original quote.

Timing and Delay-Related Exposure. Demurrage charges when containers sit at port, detention fees when equipment is not returned on schedule, production delays when shipments miss their windows—these timing-related costs rarely appear in supplier quotes but frequently appear in variance reports. Schedule slippage during peak seasons or port congestion periods can multiply these exposures significantly.

The unit price serves merely as the visible baseline of the transaction. The seven categories detailed above represent the structural cost architecture that determines actual fiscal impact. A budget that isolates the quoted price from these operational variables is fundamentally incomplete; it treats a partial data point as a total cost, ensuring that the eventual variance report will be a post-mortem of unmanaged logistics and compliance friction.

From EXW to To-Door: A Practical Normalization Workflow

Comparing quotes becomes meaningful only after every offer sits on the same basis. The goal is not to guess at missing costs—it is to make assumptions explicit so finance can trust the comparison.

How should procurement teams normalize mixed Incoterm quotes without inventing numbers?

Step 1: Establish a single Incoterm and named place as the comparison basis. For comparative normalization, DDP (Delivered Duty Paid) serves as the most effective baseline, though procurement must weigh this against the loss of logistics control inherent in supplier-managed freight. If DDP is not practical, CIF or CIP to the destination port works, with identical downstream assumptions added to each quote.

Step 2: Map each supplier’s quoted Incoterm to the comparison basis. For each quote, identify which cost layers are already included and which must be added. The methodology mirrors the approach detailed in comparing quotes across incoterms: a practical normalization method for true to-door decisions. An EXW quote requires adding origin handling, freight, insurance, duties, and destination costs. A CIF quote already includes freight and insurance but leaves duties and inland transport as buyer responsibilities. Document these gaps explicitly.

Step 3: Add the missing journey costs using consistent sources. Use the same freight forwarder quote, the same duty-rate source, and the same inland-transport estimate for every supplier. This keeps the comparison fair even when absolute numbers turn out to be estimates. Log the source and date for each figure added.

Step 4: Separate fixed quote facts from estimated downstream variables. The worksheet should visually distinguish between hard numbers—the supplier’s quoted unit price, confirmed freight rates—and soft numbers, such as duty estimates based on HS classification research or inland transport based on forwarder indicative rates. Finance needs to see which figures are locked and which carry estimation risk.

Step 5: Identify the owner of each non-quote input. Procurement may own the comparison basis. Logistics may own the lane assumptions. Finance may own the reserve logic. Quality may own the specification-risk notes. Assigning ownership transforms estimates into accountable inputs and prevents assumptions from floating anonymously through the model.

Step 6: Compare only after every offer reaches the same to-door basis. Now—and only now—does the price comparison become meaningful. The lowest unit price may no longer be the lowest landed cost. This principle—that comparability must precede price comparison—is explored further in why to-door comparability of kraft paper beats “cheapest quote” thinking. More importantly, the reasoning becomes explainable.

For deeper treatment of this normalization logic, the landed-cost framework for kraft paper: from incoterms to to-door comparability walks through freight, insurance, duty, and yield-factor normalization in detail. The price-to-door playbook extends this with freight scenario stress-testing.

Where Budgets Still Fail Even After Freight Is Added

Adding freight to the unit price is necessary but not sufficient. Budgets that look accurate on paper still fail when the team ignores operational disruption risk.

Why do specification drift and quality disputes belong in budget forecasting?

Because they happen. And when they happen, they carry costs that were never in the original quote.

Compliance delay risk materializes when documentation does not match the shipment. A certificate of origin naming the wrong mill, an HS code mismatch flagged at customs, missing compliance documentation or origin declarations—any of these can hold a container at port while demurrage charges accumulate. The WTO’s customs valuation principles outline how declared values must align with documentation; mismatches trigger inspections, delays, and sometimes penalties.

Documentation mismatch risk extends beyond customs. When the invoice entity does not match the certificate holder, or when the bill of lading shows a different consignee than the letter of credit, the resulting delays and corrections create costs that never appeared in the RFQ. For a systematic approach to preventing such mismatches, see common chain-of-custody failure modes: invoice/label mismatches and how to prevent them.

Quality disputes do not announce themselves in advance. Understanding what proof to request at RFQ stage for folding cartons can reduce the likelihood of post-arrival disputes. A batch of folding cartons that technically meets specification but performs poorly on a filling line—slightly different caliper, subtly changed coating weight—creates downstream waste that budgets did not anticipate.

Replacement or expedited corrective action becomes necessary when a defect rate exceeds tolerance. Air-freighting replacement folding cartons to avoid a production shutdown costs multiples of the original sea-freight rate. A budget that assumed zero defects was never a budget—it was a hope.

The cost-of-inaction framing matters here. A procurement budget that excludes operational disruption risk will eventually face a variance it cannot explain—and the explanation will be that the methodology was incomplete from the start.

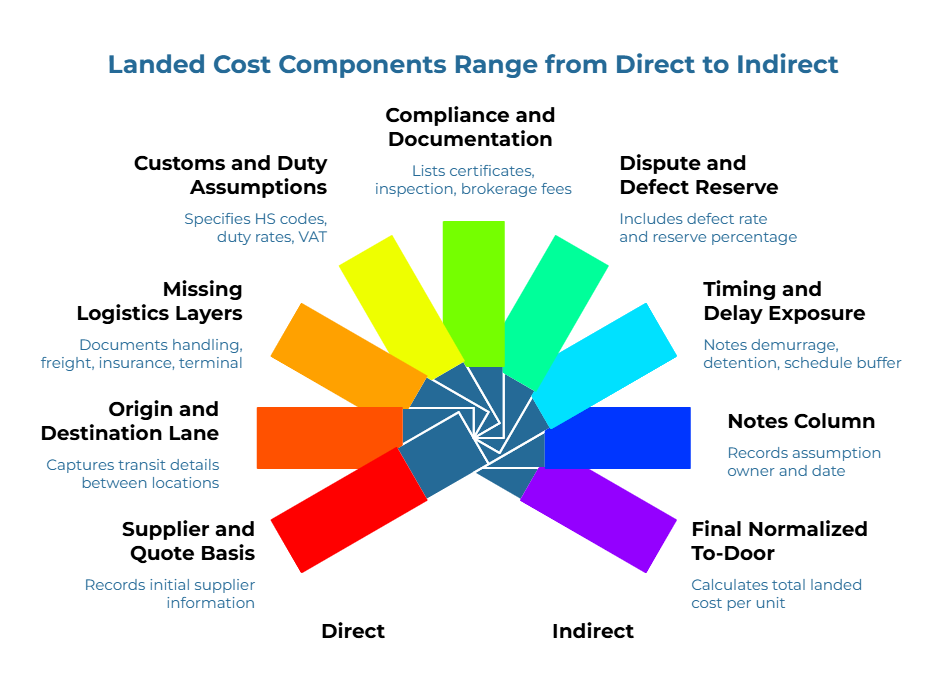

Build Your Landed Cost Normalization Worksheet

The framework becomes operational when it lives in a worksheet the team can reuse. The structure below captures essential fields. Adapt the specifics to product category and supply chain complexity.

Supplier and Quote Basis

Record the supplier name, quote reference number and date, quoted Incoterm and named place (such as EXW Shanghai, FOB Mumbai Port, or CIF Los Angeles), quoted unit price and currency, and quoted volume or order quantity.

Origin and Destination Lane

Capture origin country and port or location, destination country and port or location, and estimated transit time in days.

Missing Logistics Layers to Add

For each quote, document origin handling if not included, with amount or estimate source noted. Add freight for the main carriage with amount, rate type, and quote date. Include insurance with amount or percentage basis. Note destination terminal handling with amount or estimate source, and inland transport to facility with amount or estimate source.

Customs and Duty Assumptions

Specify the HS code used for duty calculation, applied duty rate with source reference to country tariff schedule or WTO data, estimated duty amount, VAT or GST rate and estimated amount, and any trade-agreement or preferential-rate assumptions applied.

Compliance and Documentation Assumptions

List required certificates and estimated fees, inspection or testing costs, brokerage fees, and estimated delay risk rated qualitatively as low, medium, or high.

Dispute and Defect Reserve Logic

Include historical defect rate or assumed rate, reserve percentage applied to order value, and rationale for the reserve—whether the supplier is new, the specification is complex, or historical data supports the assumption.

Timing and Delay Exposure

Note estimated demurrage risk based on port conditions, detention exposure based on equipment return requirements, and schedule buffer assumptions for production planning.

Notes Column

For every estimate, record the assumption owner—who provided the figure—and the date the assumption was recorded. Include open questions or pending confirmations. This column is what makes the worksheet auditable.

Final Normalized To-Door Comparison Field

Calculate total landed cost per unit normalized to the comparison basis, and total order value at landed cost.

What assumptions must be logged so finance can trust the comparison later?

Every estimate needs an owner and a date. When freight rates shift or duty interpretations change, the team needs to know which figures were locked and which were placeholders. A worksheet that hides its assumptions is a worksheet that breeds distrust the moment actuals diverge from forecast.

The summary below provides a scannable reference for the core worksheet logic:

| Field | What to Capture | Why It Matters |

| Quote basis | EXW, FOB, CIF, DDP, or other named-place basis | Establishes the comparison basis |

| Logistics additions | Freight, insurance, destination handling | Converts partial quotes to to-door comparability |

| Customs logic | Classification, duties, valuation assumptions | Prevents post-award landed-cost surprises |

| Compliance notes | Documentation, labeling, certificates, approvals | Captures friction that can delay release |

| Quality-risk note | Specification drift, claim exposure, defect handling | Reflects operational risk, not just nominal price |

| Ownership and date | Assumption owner and last update | Makes the model auditable for finance |

The worksheet should feel slightly boring. That is a good sign. Calm tools beat clever shortcuts in procurement.

The common pitfalls in landed-cost estimates reinforces this discipline: log every assumption, normalize to one basis, and run a cross-check before committing. If assumption logging remains the weak point, beyond haggling: why driver-based benchmarks create kraft paper procurement confidence reinforces the broader worldview shift from price haggling to structured cost discipline.

Forecasts Improve When Assumptions Stop Hiding

The goal was never to make a better guess. The goal was to build a better cost frame—one that forces every supplier onto the same comparison basis and exposes every assumption that affects the final landed cost.

When the quarterly budget review arrives, the conversation shifts. Instead of explaining a variance that came from nowhere, procurement presents a methodology that makes the gap between quote and invoice predictable, documented, and defensible.

Unit price is only a fraction of the true cost structure; ignoring landed costs ensures budget failure.

The strategy succeeds when assumptions are dated, owners are assigned, and budgets reflect actual landed liabilities rather than spreadsheet-bound illusions. True procurement discipline is realized when the budget reflects the fully burdened ‘To-Door’ reality—accounting for every mile, duty, and quality contingency before the first folding carton ever leaves the supplier’s loading bay.

To see how this landed-cost method fits into the broader budgeting system, continue with the parent framework: the guesswork gap: using specification-true quotes to build a predictable folding carton packaging budget.

Buyers evaluating international folding carton sourcing options can explore verified folding carton suppliers on PaperIndex.

Resources

For further reading on landed-cost normalization and defensible supplier evaluation:

- The Price-to-Door Playbook: Integrating Driver-Based Benchmarks with a Landed-Cost Framework for Defensible Supplier Selection

- The Landed-Cost Framework for Kraft Paper: From Incoterms to To-Door Comparability

- Common Pitfalls in Landed-Cost Estimates of Kraft Paper (and How to Avoid Invoice Disputes)

- Beyond Haggling: Why Driver-Based Benchmarks Create Kraft Paper Procurement Confidence

Disclaimer

This article is educational and explains procurement and landed-cost concepts for learning purposes only. Any examples, figures, or scenarios should be treated as illustrative, not as current market quotations, forecasts, or professional advice. Readers should verify duty rates, freight costs, and regulatory requirements with qualified professionals before making procurement decisions.

Our Editorial Process:

Our expert team uses AI tools to help organize and structure our initial drafts. Every piece is then extensively rewritten, fact-checked, and enriched with first-hand insights and experiences by expert humans on our Insights Team to ensure accuracy and clarity.

About the PaperIndex Insights Team:

The PaperIndex Insights Team is our dedicated engine for synthesizing complex topics into clear, helpful guides. While our content is thoroughly reviewed for clarity and accuracy, it is for informational purposes and should not replace professional advice.