📌 Key Takeaways

The gap between paying kraft paper suppliers and collecting from customers locks up working capital that could fuel growth instead of just funding timing mismatches.

- Payment Terms Are Design Levers, Not Fixed Rules: Supplier and customer payment terms can be adjusted gradually through respectful conversations, transforming a structural cash squeeze into a manageable rhythm where month-end stops feeling like a crisis.

- A One-Page Summary Turns Anxiety Into Clarity: Mapping current supplier days, customer days, and the resulting cash gap onto a single shareable page makes the invisible strain visible, enabling productive conversations with owners, teams, and banks without complex spreadsheets or financial jargon.

- Small Moves on Both Sides Compound Into Material Relief: Extending one key supplier from 30 to 45 days while encouraging one major customer to move from 90 to 75 days can cut a 35-day cash gap to 20 days, freeing ₹15 lakh ($18,000 USD) in working capital without straining relationships.

- The Five-Section Framework Makes It Bank-Ready: A complete one-page summary requires a clear header and purpose, current payment terms snapshot, cash gap estimate with rough working capital impact, target terms showing realistic improvements, and action notes with specific next conversations—simple enough to draft in a spreadsheet, professional enough for a banking discussion.

- Internal Alignment Multiplies External Success: When procurement sees how supplier negotiations affect the overall cash gap and sales understands how customer term extensions impact the same gap, the entire team starts thinking in terms of cash conversion cycles rather than just invoice amounts, making term improvement conversations far more strategic.

Visibility precedes control—one page can transform working capital from a constant source of stress into something the business actively manages.

Finance and procurement leaders at SME packaging converters will gain a concrete framework here, preparing them for the detailed implementation guidance that follows.

The overdraft sits at 92% of its limit. Three kraft paper supplier invoices are due this week. Your largest customer’s payment? Still another eighteen days away.

You know the pattern by now. Every month-end brings the same tight feeling, the same mental calculations about which invoices can wait and which absolutely cannot. The problem isn’t poor management or unrealistic forecasts. The structural gap between when you pay suppliers and when customers pay you creates a predictable cash squeeze that no amount of operational efficiency can eliminate.

What if you could see that gap clearly on a single page? What if you could show your owner, your bank manager, and your team exactly how kraft paper payment terms affect working capital—not with complex spreadsheets or accounting jargon, but with a simple, honest picture that everyone can understand in minutes?

That’s what this guide will help you build: a one-page payment terms summary that turns vague anxiety about “tight cash” into a concrete conversation starter. By the end, you’ll have a template you can complete with your own numbers and share confidently with the people who need to understand your cash rhythm.

Why Your Kraft Paper Payment Terms Deserve a One-Page Summary

Most finance and procurement leads at SME packaging converters can recite their main supplier and customer terms from memory. The kraft paper mill wants payment in thirty days. The large retailer takes ninety. You’ve accepted these terms as fixed constraints, handed down by stronger players in the supply chain.

But here’s what often remains invisible: those terms interact to create a specific cash conversion cycle pressure[1]. When you pay suppliers in thirty to sixty days while customers take sixty to ninety days to settle, the gap between cash out and cash in can stretch to thirty, forty, or even sixty days. At a monthly kraft paper spend of ₹30 lakh (approx. $36,000 USD), a sixty-day gap means roughly ₹60 lakh (approx. $72,000 USD) is constantly tied up just in the timing mismatch.

That’s working capital strain from payment terms—money that’s technically yours but unavailable because it’s stuck in the conversion cycle between buying paper and getting paid for boxes.

Globally, access to working capital remains one of the primary constraints limiting small and mid-sized businesses[2]. In markets such as the UK, the Federation of Small Businesses has historically estimated that poor payment practices threaten business survival, contributing to roughly 50,000 business closures annually according to their advocacy reports [3]. The financial pressure isn’t abstract—it’s a documented threat to business survival.

The one-page summary makes this visible. It takes terms you already know and arranges them so the structural problem becomes obvious to anyone looking at the page. More importantly, it reframes payment terms as design levers you can adjust gradually on both sides of the chain, rather than as fixed rules you must simply endure.

Most existing working capital content offers generic advice written by banks or consultants who’ve never managed kraft paper procurement at month-end. This guide assumes you understand your business. The challenge isn’t intelligence—it’s that nobody has yet shown you a simple, kraft-paper-specific picture of how supplier days and customer days combine to lock up cash.

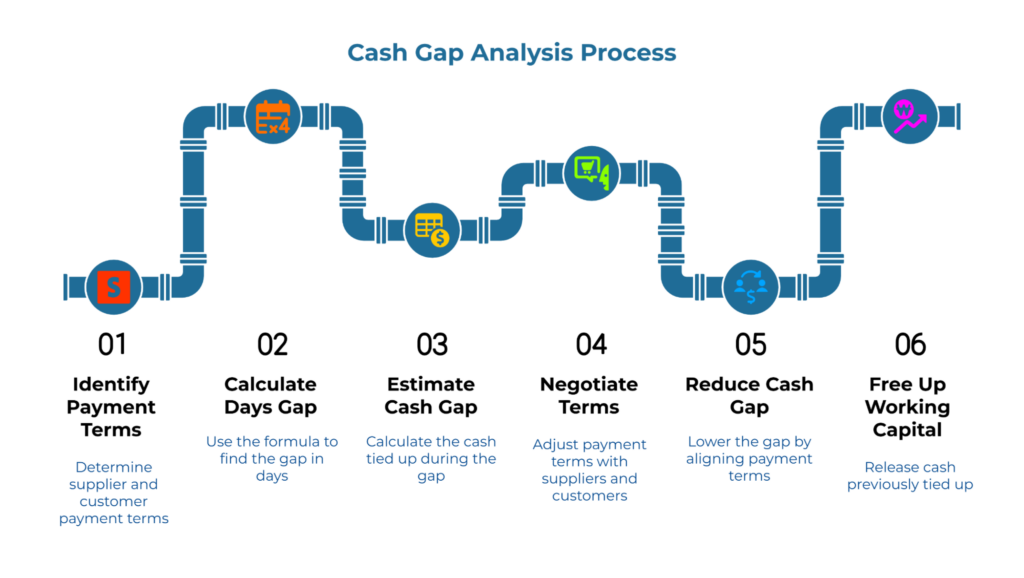

Map Your Current Supplier and Customer Payment Terms on One Line

Start by writing down current payment terms for your most important kraft paper suppliers and largest customers. You don’t need every account—just the handful that represent the majority of your monthly paper spend and incoming revenue.

The one-page summary needs rough but honest numbers, not perfect precision. Focus on the top three to five kraft paper suppliers by volume or spend, and the top five to ten customers that drive most of your kraft paper usage.

Supplier days represent how long you have to pay after receiving kraft paper. If your main mill invoices you on delivery and expects payment within thirty days, your supplier term is thirty days. Customer days represent how long your customers take to pay after you deliver finished boxes. If your contract specifies net sixty days and customers typically settle around day sixty-five, your customer term is approximately sixty-five days.

For each key relationship, note typical credit terms and how they behave in reality. If a customer’s contract says sixty days but they consistently pay in seventy-five, use seventy-five. This is about visibility, not creating an idealized version of reality.

The resulting picture might look something like this:

Suppliers: Mill A (30 days), Mill B (45 days), Trader C (30 days)

Customers: Large Retailer (90 days), Regional Distributor (60 days), Direct Industrial Client (45 days)

Already, a pattern emerges. Your cash goes out much faster than it comes back in. The timeline is lopsided, creating the familiar squeeze you feel every month-end.

Turn That Timeline Into a Visible Cash Gap

Now translate those term differences into a concrete cash gap measured in both days and money.

Think in three steps: When does money leave for kraft paper? When does money come back from customers? How many days of extra funding are needed in between?

Calculate the Days Gap

You can estimate your cash gap using this simple formula:

Cash gap (in days) ≈ (Days holding inventory + Days to collect from customers) – Supplier days

This isn’t a precise accounting formula—it’s a design estimate for discussion. Actual figures will vary by order pattern, partial payments, and other terms. But even an estimate such as “around 45 days” gives a much clearer sense of working capital strain than vague statements like “collections are slow.”

A Practical Numerical Example

Consider a simplified scenario. You buy kraft or brown paper from two main suppliers: one requires payment in thirty days, the other in forty-five days. Your weighted average supplier term is roughly thirty-five days. On the customer side, your largest accounts pay in ninety days, sixty days, and forty-five days respectively. Your weighted average customer term is approximately seventy days.

The gap between paying suppliers (day 35) and receiving payment from customers (day 70) is thirty-five days. During those thirty-five days, cash is effectively tied up.

If your average monthly kraft paper spend is ₹30 lakh, that thirty-five-day gap represents roughly ₹35 lakh ($42,000 USD) of average working capital constantly locked in to bridge the timing difference. You can calculate this by determining your approximate daily kraft paper purchases (monthly purchases ÷ 30), then multiplying by the days gap.

Small changes on both sides materially reduce that gap. If you could negotiate one key supplier from thirty days to forty-five days, and simultaneously encourage one large customer to move from ninety days to seventy-five days, your gap narrows to twenty days. That frees up approximately ₹15 lakh ($18,000 USD) in working capital that was previously immobilized.

Think of payment terms as bicycle gears[4]. When supplier terms, inventory management, and customer terms work together in reasonable alignment, the “legs, chain, and wheels” of your business move in sync. When they’re badly mismatched—very tight supplier terms against very long customer terms—you’re constantly pedaling uphill against resistance. Small adjustments bring those gears closer to alignment without requiring heroic effort from any single party.

The numbers here are illustrations to show direction and magnitude, not precise projections. The principle holds across different scales: narrowing the structural gap between cash out and cash in reduces the amount of working capital you need just to maintain steady operations.

Define Safer Target Terms With Small Moves on Both Sides

Instead of accepting current terms as unchangeable, sketch target terms that narrow the gap through modest, relationship-respectful adjustments. This is a design exercise, not a list of demands.

On the supplier side, identify your tightest term—the supplier demanding the fastest payment. Could that term shift by even ten or fifteen days? You’re not seeking unlimited credit. You’re proposing a small improvement that moves you from “impossible to manage” toward “difficult but workable.”

On the customer side, identify your longest term—the customer taking the most time to pay. Could that customer reasonably move closer to industry standard terms? Again, you’re not demanding immediate payment. You’re asking whether net ninety days could become net seventy-five days, or net seventy-five could become net sixty.

These changes require conversations, not demands. The one-page summary you’re building isn’t a negotiation weapon. It’s a clear, neutral picture that helps everyone—including suppliers and customers—understand why the current structure creates strain and how small shifts on both sides can reduce that strain without disadvantaging any single party.

A realistic target might look like this:

Supplier A: Current 30 days → Target 45 days

Customer X: Current 90 days → Target 75 days (ensuring compliance with local prompt payment laws, such as the MSMED Act in India which may cap terms at 45 days)

Those two adjustments alone could cut your cash gap from thirty-five days to approximately twenty-five days, freeing significant working capital without requiring large structural changes to existing agreements.

The goal isn’t perfect symmetry where supplier and customer terms match exactly. The goal is reducing the gap to a manageable level where month-end doesn’t feel like a recurring crisis and where modest volume growth doesn’t immediately trigger working capital strain.

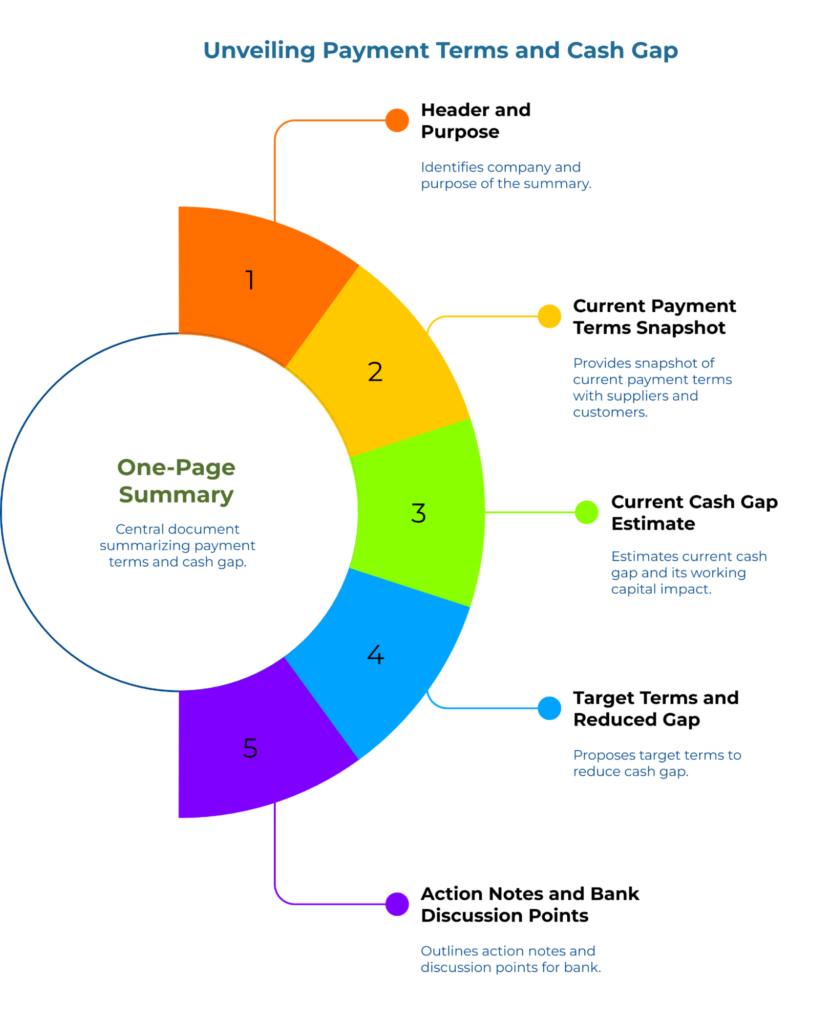

Pull Everything Together: What Goes on Your One-Page Summary

The one-page summary is your central deliverable. It should be simple enough to draft in a basic spreadsheet, clear enough for a designer to format as a clean PDF, and understandable enough that an owner or bank manager can grasp the key points in a few minutes without requiring a detailed explanation from you.

Think of this page as a bank-friendly payment terms summary or cash gap summary sheet. It should be structured enough to support a serious discussion but simple enough to print and carry into a meeting.

Section A: Header and Purpose

At the top, keep it straightforward:

- Company name and brief description (e.g., “Corrugated box manufacturer – medium-sized – main raw material: kraft paper”)

- Purpose line: “One-page summary of current and target payment terms for kraft paper suppliers and customers, and the resulting working capital gap.”

Section B: Current Payment Terms Snapshot

Show in compact form:

- Key kraft paper suppliers with typical credit terms and actual payment behavior

- Key customers with stated terms and actual collection patterns (e.g., “60 days on paper, 75 days in practice”)

A simple table format works well here, grouped by suppliers and customers. The goal is clarity, not completeness.

Section C: Current Cash Gap Estimate

Bring the numbers together:

- A short line explaining the approximate current gap in days (e.g., “Current estimated gap: ~45 days between paying suppliers and collecting from customers.”)

- A plain-language note on what that means in rough working capital terms (e.g., “This forces us to carry about 1.5 months of kraft paper purchases as extra working capital.”)

This is the heart of the working capital strain summary—but kept at a level that operations managers, sales heads, and bankers can all follow.

Your table might show:

| Supplier/Customer | Current Days | Target Days | Change |

| Supplier A | 30 | 45 | +15 |

| Supplier B | 45 | 45 | 0 |

| Customer X | 90 | 75 | -15 |

| Customer Y | 60 | 60 | 0 |

Section D: Target Terms and Reduced Gap

Show:

- Proposed target supplier terms (e.g., “Move 2 main suppliers towards 45 days”)

- Proposed target customer terms (e.g., “Move top 5 customers towards 60 days actual”)

- Resulting target days gap (e.g., “Target gap: ~15–20 days.”)

One or two sentences can spell out the strategic effect: “If we move to this target profile, the kraft paper cash gap shrinks from ~45 days to ~15–20 days, freeing up a significant portion of our existing working capital and bank limits.”

Section E: Action Notes and Bank Discussion Points

Outline:

- Which supplier discussions need to happen, and who leads them

- Which customer terms adjustments will be attempted, and in what order

- Any internal process changes (e.g., faster invoicing, clearer payment follow-up)

Include a clearly labeled box summarizing what this means for your bank:

“Our kraft paper cash gap currently requires us to carry approximately X days of purchases in working capital. Our target terms design would reduce this requirement over the next 6–12 months, provided our bank continues to support our working capital line. We are sharing this one-page payment terms summary to support a transparent discussion on how best to fund kraft-paper-related working capital.”

Include a gentle reminder that the page is a guide for discussion and planning, not a binding contract or a set of demands. Something like: “These targets are initial proposals for discussion. Actual terms will be agreed through respectful conversations with each party.”

The complete page should fit on a single sheet—viewable on a laptop screen, printable without awkward page breaks, or shareable as a PDF via email. It should require no specialized financial knowledge to understand. A plant manager or owner should be able to look at it and immediately grasp both the current cash pressure and the proposed direction.

How to Use the Summary With Your Team

The one-page terms summary is most useful when it’s actively used, not just filed. Internally, it can help align three critical functions that often operate in silos:

Procurement sees how negotiating an extra fifteen days from a mill affects the overall cash gap, not just the individual purchase order.

Sales sees how offering an extra fifteen days to a customer affects the same gap, making the trade-off between winning business and working capital visible.

Finance can show both teams how supplier and customer sides interact, using a simple visual instead of a dense spreadsheet that only accountants can parse.

The page makes it easier to prioritize which customers or suppliers to approach first. It also helps the team accept that not every negotiation will succeed—the design shows preferred direction, not guaranteed outcomes.

Over time, plant managers, sales heads, and even operations supervisors start to understand terms not just as “commercial offers,” but as part of the company’s cash conversion cycle. The more often the page is used in internal reviews, the more naturally the team starts to think in terms of days of cash gap, not just invoice amounts.

How to Use the Summary With Your Bank

Banks and other lenders generally appreciate concise, transparent information about how a business manages its working capital and trade credit[5]. A clear one-page payment terms summary can support conversations in several ways by showing where the strain is—not just that there is strain.

Once you’ve completed your one-page summary with actual numbers from your business, it becomes a powerful conversation tool.

Present it with calm, factual language such as:

“This page summarizes how our kraft paper payment terms currently work and where we are trying to move them. You can see the gap between paying mills and collecting from customers, and how that translates into working capital needs. We are not asking you to rely on promises of future collections; we are showing the current pattern and the realistic moves we are pursuing.”

This helps shift the conversation from vague complaints (“customers are slow”) to a more professional, data-informed approach. The summary demonstrates you understand your working capital needs precisely rather than simply requesting more credit when overdrafts approach limits. It positions you as a professional manager making data-informed requests rather than a desperate borrower seeking emergency relief.

The one-page summary does not create any obligations for the bank. It simply clarifies the numbers. The bank will still apply its own risk, compliance, and product frameworks. The summary aims to make those discussions more efficient and grounded, not to replace the bank’s own analysis.

What This One-Page Summary Is—and What It Is Not

Because this page will be shared beyond the finance team, it helps to be explicit about boundaries:

What It Is

- A design tool for thinking about payment terms with kraft paper suppliers and customers

- A communication tool for aligning internal teams on the cash gap

- A bank-friendly working capital support summary for explaining your kraft-paper-related cash needs

- A starting point for respectful conversations about improving terms on both sides

What It Is Not

- Not a legal document, contract, or commitment from any party

- Not a guarantee that suppliers or customers will accept new terms

- Not a replacement for detailed financial statements, aging reports, or formal cash flow forecasts

- Not personal financial advice or a recommendation for any specific product, bank, or structure

For decisions on facilities, limits, and risk, each business should rely on its own financial records, advisers, and banking relationships.

Where This Fits in the Wider Series

The one-page payment terms summary connects to other working capital resources. If you want a more detailed view of how supplier days, inventory days, and customer days combine to form your complete cash conversion cycle, the guide Working Capital Strain from Payment Terms: A Beginner’s Cash Conversion Cycle Map walks through that mapping process step by step.

For readers ready to design a more comprehensive set of term adjustments across multiple suppliers and customers, Payment Terms Design for Kraft Paper Suppliers & Customers: A Simple Playbook to Align Cash In and Cash Out provides detailed frameworks for structuring those conversations and implementing changes gradually.

And if you’re still establishing a foundational understanding of how payment terms create working capital strain, Working Capital Strain from Payment Terms: A Simple Guide to Seeing and Fixing Your Kraft Paper Cash Flow Gap offers a complete overview of the problem and solution approach.

These can be read together as a toolkit: Use the cash conversion cycle map to understand your overall flow. Use the simple guide to working capital strain to quantify the impact of terms. Use this one-page payment terms summary to communicate your current position and targets. Use the alignment playbook to plan gentle, practical moves on both supplier and customer sides over time.

Moving From Anxiety to Control

The one-page payment terms summary won’t eliminate working capital challenges overnight. It won’t magically extend every supplier term or accelerate every customer payment. But it will transform how you think about and discuss those challenges.

Instead of vague anxiety about “tight cash,” you’ll have a concrete picture showing exactly where the strain originates and approximately how much it costs. Instead of feeling powerless in payment term discussions, you’ll have a clear, professional framework for proposing small improvements that benefit all parties. Instead of month-end feeling like an unpredictable crisis, you’ll understand the structural rhythm driving cash pressure and can plan accordingly.

Payment terms are design levers, not fixed constraints. The gap between supplier days and customer days can be narrowed through modest, relationship-respectful adjustments on both sides. With that visibility and those adjustments, working capital becomes something you actively manage rather than something that manages you.

Complete your one-page summary. Share it with your team. Use it as a starting point for calmer, more constructive conversations about how payment terms affect cash flow. That simple act—making the invisible visible—is often the first step toward a more predictable, less stressful cash rhythm.

Disclaimer: This article provides educational guidance on understanding and discussing payment terms and working capital. It is not professional financial advice. Readers should consult with their own banker or financial adviser before making decisions about credit facilities, significant term changes, or major working capital strategies.

References:

[1]: The cash conversion cycle measures how long it takes a business to convert inventory and other resources into cash from sales. For kraft paper buyers, this cycle begins when cash goes out to suppliers and ends when payment arrives from customers. Educational resources on cash conversion cycles are available from Investopedia and Trade Finance Global.

[2]: Working capital management remains a critical challenge for small and medium-sized enterprises globally.. Access to adequate working capital often determines whether businesses can scale operations or must decline growth opportunities.

[3]: Research from the Federation of Small Businesses in the UK consistently highlights that poor payment practices—specifically, late payment from larger customers to smaller suppliers—contribute to approximately 50,000 business closures annually in that market alone.

[4]: The concept of business processes working in alignment—similar to mechanical systems with properly matched gears—is well-established in operations management literature. When payment terms, inventory levels, and collection cycles are misaligned, working capital requirements increase substantially.

[5]: Banking institutions increasingly emphasize cash flow analysis and working capital management when evaluating credit applications for small and medium enterprises. Resources on working capital fundamentals are available from institutions like PNC Bank and similar financial education platforms.

Our Editorial Process

Our expert team uses AI tools to help organize and structure our initial drafts. Every piece is then extensively rewritten, fact-checked, and enriched with first-hand insights and experiences by expert humans on our Insights Team to ensure accuracy and clarity.

About the PaperIndex Insights Team

The PaperIndex Insights Team is our dedicated engine for synthesizing complex topics into clear, helpful guides. While our content is thoroughly reviewed for clarity and accuracy, it is for informational purposes and should not replace professional advice.