📌 Key Takeaways

The MOQ Barrier forces small converters to choose between channels that don’t fit their reality—but a neutral decision matrix turns that problem into a documented, defensible sourcing strategy.

- The Real Cost Isn’t Per-Ton Price: Working capital strain, warehouse overcrowding, and locked cash from oversized MOQs often erase the savings from “cheap” mill-direct pricing.

- Seven Criteria Drive Channel Fit: MOQ flexibility, price-to-door, lead time reliability, working capital impact, quality risk, operational load, and grade breadth determine which sourcing channel actually works at your scale.

- No Universal Winner Exists: Marketplaces excel at flexibility and grade access, mill-direct delivers lowest unit costs for stable volume, and local distributors provide speed—the right choice depends entirely on your current cash position and order volatility.

- The Matrix Aligns Stakeholders: When Business Owners and Procurement Managers score the same criteria together using a 1-5 importance scale, internal arguments about “price versus convenience” become logical, data-backed decisions.

- Document to Build Capability: Recording each sourcing decision with its criteria scores and actual outcomes creates a learning asset that refines your channel selection over time and extends beyond kraft paper to other materials.

Most sourcing decisions fail because they optimize for the wrong variable at the wrong time—this framework ensures your choice protects both margin and agility.

SME packaging converters struggling with high supplier MOQs will find a practical evaluation tool here, preparing them for the detailed channel-by-channel comparison and worked examples that follow.

Now that you understand how high MOQs strain your working capital and warehouse space, the next decision is where to buy low-volume kraft paper without making that problem worse.

Most SME converters face the same bind. You need reliable grades and service levels, but traditional mill-direct channels demand order volumes that don’t match your reality. Local distributors seem convenient but carry a price premium that cuts into already tight margins. Online marketplaces promise flexibility but raise questions about kraft paper supplier reliability and quality consistency.

The answer isn’t the same for every converter. It depends on your current cash position, order book stability, and tolerance for operational complexity. This article provides a neutral, criteria-based decision matrix that helps you evaluate three sourcing channels—online marketplaces, mill-direct relationships, and local distributors—across the factors that actually affect your bottom line and operational agility.

How to Use This Low-Volume Sourcing Decision Matrix

This matrix works like a checklist combined with a scoring sheet. You’ll evaluate three sourcing channels against seven criteria that directly impact working capital, lead times, and operational load.

The process is straightforward. First, you’ll identify which criteria matter most for your current situation. A converter with tight cash flow and volatile demand will weigh criteria differently than one with stable contracts and predictable volume. Second, you’ll score how each channel performs on those criteria. Third, you’ll arrive at both a primary recommendation and a backup option.

The output isn’t a universal answer. It’s a documented rationale that you can defend to your finance team, reference in future sourcing decisions, and adjust as your business evolves. Many converters find that their optimal mix involves using different channels for different order types rather than committing exclusively to one.

Why Low-Volume Sourcing Is So Hard for SME Converters

High MOQ requirements are the supply chain constraint where mill-imposed volume minimums exceed the capital and storage capacity of SME converters. It’s like having to buy a whole cow just to get a single steak—it’s inefficient and wasteful for your needs. Imagine the frustration of identifying a perfect paper grade, only to be rejected by the supplier because your 20-ton order ‘isn’t worth their time.’ This problem necessitates finding alternative sourcing channels, such as aggregators or flexible marketplaces.

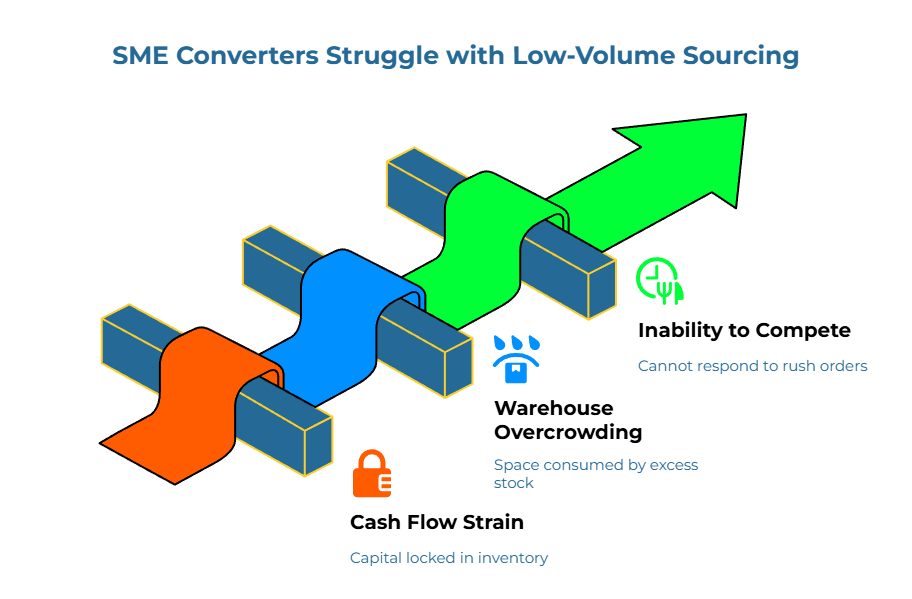

The MOQ Barrier creates three specific operational problems for small converters.

Cash flow strain hits first. Working capital—the capital used in day-to-day operations, typically defined as current assets minus current liabilities—becomes disproportionately locked in inventory when a small converter is forced to buy several months of paper at once. This lengthens the cash conversion cycle, which is the time between paying suppliers and collecting from customers, and increases financial risk. A converter forced to purchase a 40-ton minimum order quantity (MOQ) at $1,000 per ton must allocate $40,000 in working capital, illustrating the magnitude of capital strain caused by large MOQs, effectively parking that cash in the warehouse instead of using it to pursue new accounts or upgrade equipment.

Warehouse overcrowding follows quickly. Physical space costs money, whether you own or lease. Excess inventory from oversized orders consumes valuable floor space that could house finished goods ready for shipment. The risk compounds when you’re carrying inventory for multiple grades to serve different customer segments. Storage costs, handling expenses, and the possibility that specifications change before all rolls are used add hidden costs that erode the apparent savings from “cheap” per-ton pricing.

The inability to compete on lead time becomes the strategic vulnerability. When your cash and space are locked in slow-moving inventory, you can’t respond quickly to rush orders or seasonal demand spikes that would otherwise be profitable. A customer asking for a three-day turnaround might represent a high-margin opportunity, but you’re forced to decline because you can’t justify another large purchase when the warehouse is already full.

SME converters face greater exposure to these problems than large kraft paper buyers. Smaller businesses typically have less access to cheap credit and are more vulnerable when cash becomes trapped in slow-moving stock. For a deeper breakdown of how payment terms interact with this cycle, the Academy’s guide on working capital strain from payment terms explains the mechanics of cash conversion cycles in practical terms.

Overcoming the MOQ barrier isn’t just about finding cheaper paper. It’s about protecting your working capital so you can operate with the agility your business scale demands.

The Criteria That Actually Matter for Low-Volume Sourcing Decisions

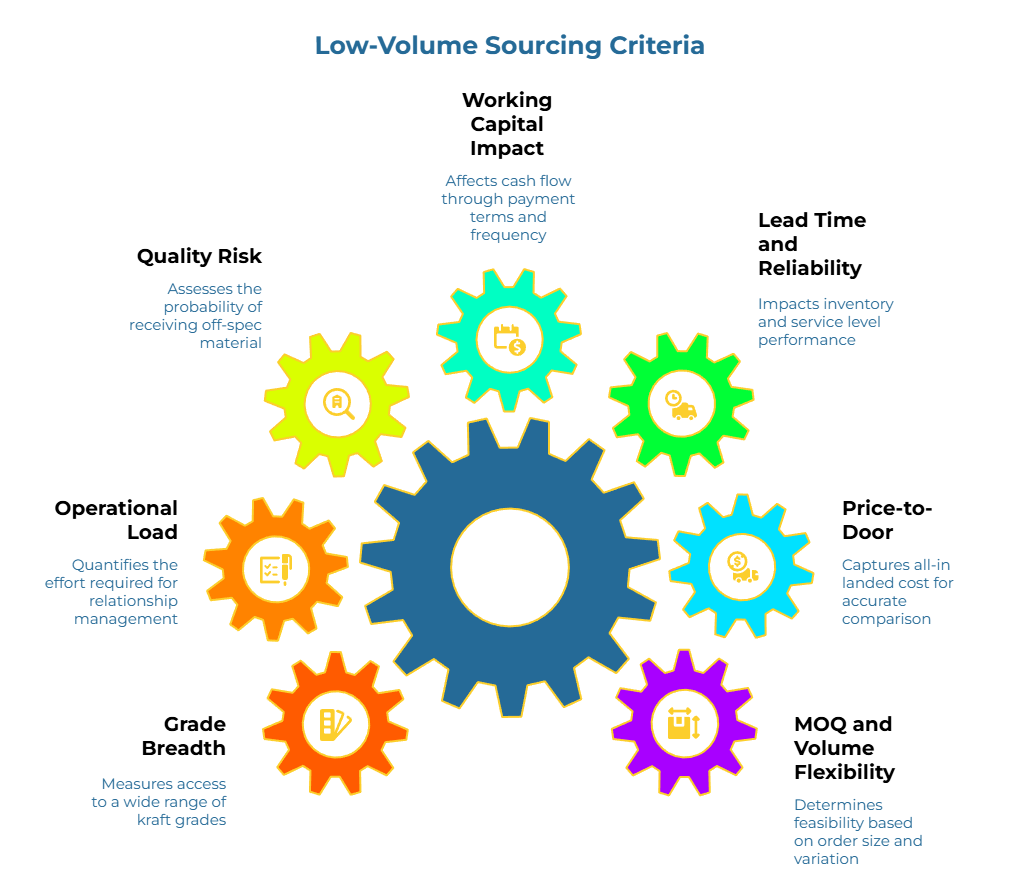

Seven criteria determine whether a sourcing channel fits your operational reality. Each one reveals different trade-offs between cost, flexibility, and risk.

MOQ and Volume Flexibility measures the smallest order a channel will accept and how much variation they’ll tolerate across orders. For SME converters, this criterion often determines feasibility before price even enters the conversation. A channel that demands 40 tons minimum doesn’t work if your monthly consumption averages 15 tons across all grades.

Price-to-Door captures all-in landed cost to your warehouse. This includes the paper itself, freight, insurance, duties if applicable, and any handling or coordination fees. A supplier quoting $500 per ton EXW isn’t directly comparable to one offering $580 DDP to your dock. You need the final number that hits your books, not a starting quote that excludes logistics.

Lead Time and Reliability tracks typical fulfillment windows and schedule consistency. Lead time and its variability are critical drivers of safety stock requirements and service level performance. Longer or less predictable lead times force converters to hold more inventory, which increases working capital needs and ties up warehouse space. If you’re serving accounts with firm delivery commitments, supplier reliability becomes critical. Missing a shipment window by three days might cost you more than you saved by choosing the cheapest channel.

Working Capital Impact measures how much cash stays tied up and for how long. This goes beyond the purchase price to include payment terms, inventory holding periods, and order frequency. A channel offering Net 60 terms with monthly deliveries treats your cash flow very differently than one requiring prepayment for quarterly shipments.

Quality Risk assesses the probability of receiving off-spec material and the complexity of resolving disputes when it happens. Some channels have clear recourse processes with established inspection protocols. Others require more negotiation and proof. The risk isn’t just about getting bad paper—it’s about the time and friction involved in making it right.

Operational and Administrative Load quantifies the effort required to onboard, coordinate, and maintain the relationship. This includes documentation requirements, communication friction due to time zones or language, the number of touchpoints needed to place and track orders, and the learning curve for their systems or processes.

Grade Breadth and Availability measures your access to a wide range of kraft grades, basis weights, and specifications across suppliers. Broader access makes it easier to match niche customer requirements and to substitute grades when a particular kraft paper mill faces capacity constraints or quality issues. For converters in growth phases or those testing new product lines, having options matters as much as securing the best price on a single grade.

Use a simple 1 to 5 scale to rate how important each criterion is for your situation right now. A score of 1 means “not critical at this moment,” while 5 means “absolutely critical to our operation.” For instance, if your cash flow is tight and your order book is volatile, MOQ Flexibility and Working Capital Impact might both rate as 5s. If you’re testing a new grade for a potential customer segment, Grade Breadth and Quality Risk might move to the top of your priority list.

The scoring isn’t static. As your business evolves—perhaps you secure a major contract that stabilizes volume, or expand into a new product line that requires different grades—your criteria weights should shift to reflect that new reality.

Option 1: Marketplace Sourcing for Low-Volume Orders

Online marketplaces designed for the paper industry aggregate multiple suppliers in a single discovery environment. For SME converters, this model addresses the MOQ problem indirectly by increasing your options and creating competitive pressure that can make suppliers more flexible on minimums.

Paper marketplaces typically don’t hold inventory themselves. Instead, they connect you with mills, traders, and converters who list their available grades and terms. You submit inquiries or post requirements, receive quotes from multiple sources, and conduct negotiations directly with suppliers you choose.

The primary advantage for low-volume buyers centers on choice and flexibility. When you can compare offerings from suppliers across different geographies and business models in one place, you’re more likely to find someone whose natural order size aligns with your consumption patterns. A regional trader might be sourcing from a mill at higher volumes but happy to sell you 10 tons if that’s what you need. The marketplace provides the visibility to find that match.

Additional benefits include easier discovery of alternative suppliers when your primary source faces capacity constraints or quality issues, the ability to test new grades from different regions without long-term commitments, and access to suppliers you wouldn’t have found through traditional networking. For converters exploring new product applications or entering unfamiliar markets, the breadth of grade options available through marketplace aggregation often exceeds what local distributors stock or what individual mill relationships would provide.

The trade-offs require attention. Supplier quality varies more than in curated mill-direct relationships. You need to verify credentials, check references, and potentially run trial orders before committing to larger volumes. This due diligence takes time. Some marketplaces offer verification badges or screening processes, but you still own the final vetting decision. Platform learning curves exist as well—you’ll need to understand how to post requirements, evaluate responses, and use any communication or documentation tools the platform provides.

Marketplace sourcing tends to be the best fit when you’re exploring new grades where you lack established mill relationships, when you’re entering new geographic markets and need local sourcing options, when your primary supplier is at capacity and you need overflow coverage quickly, or when your order volumes are genuinely too small to justify mill-direct relationships.

Option 2: Mill-Direct Sourcing When You Are Volume-Constrained

Mill-direct sourcing means buying directly from kraft paper manufacturers without intermediaries. The traditional appeal is straightforward: lowest unit pricing, direct access to technical support and quality specifications, and predictable production schedules if you’re a regular customer.

For SME converters, the reality is more complicated. Mills optimize their operations around large production runs and high-volume customers. Their economic model rewards consistency and scale. When your order represents a small fraction of their capacity, you naturally fall lower in their priority queue for scheduling, customer service response times, and pricing flexibility.

Let’s walk through how mill-direct scores on each criterion for smaller converters.

MOQ and Volume Flexibility rates are low for most mills. Typical minimums range from 40 to 100 tons depending on grade and region. Some mills won’t even quote below 20 tons. This constraint immediately disqualifies mill-direct for converters whose monthly consumption sits below these thresholds. Even when you can meet the minimum occasionally, the inflexibility becomes problematic. Mills rarely accommodate partial shipments or allow you to split an order across delivery windows.

Price-to-Door rates medium to high depending on how you structure logistics. Mills quote EXW or FOB, which means you’re responsible for arranging and paying freight. For small shipments or complex routing, freight costs can erode the per-ton price advantage. However, if you can coordinate full container loads or pool orders with other buyers, mill-direct often delivers the best all-in cost.

Lead Time and Reliability rates medium. Established mills run predictable production schedules, which provides planning certainty if you’re a regular customer. The challenge for SME buyers is that smaller orders may be deprioritized when capacity tightens. A mill might stretch your four-week lead time to six weeks if a larger customer needs urgent capacity, leaving you scrambling to explain delays to your own customers.

Working Capital Impact rates low. Mill-direct typically requires prepayment or short payment terms (Net 30 at best, often prepayment for new accounts). Combined with large order sizes, this creates significant cash flow demands. You’re paying for three to six months of inventory upfront and waiting weeks or months to convert it back to cash through sales.

Quality Risk rates high for established mills. Once you’ve qualified a supplier and run trial orders, consistency tends to be strong. Mills have quality control processes and typically stand behind their product specifications. The risk comes during onboarding—qualifying a new mill source takes time and involves sample reviews, trial orders, and specification alignment.

Operational and Administrative Load rates medium to low once relationships are established. Initial onboarding involves technical discussions, quality requirements documentation, and legal paperwork. However, ongoing order management can be streamlined for repeat purchases. The friction comes from time zone differences, language barriers in some regions, and the formality of communication with large organizations.

Grade Breadth and Availability rates medium. Each mill specializes in a finite range of grades and basis weights based on their equipment and market focus. Expanding your grade options through mill-direct relationships requires building and maintaining multiple mill contacts, which multiplies the coordination complexity and often isn’t practical for small teams.

Mill-direct remains viable for SME converters in specific situations. If you can pool demand from multiple customers to reach minimum volumes, the economics improve substantially. Converters with stable, long-term contracts that create predictable monthly consumption above 30 tons can justify mill-direct relationships. Some mills offer more flexible terms to smaller buyers if you commit to regular purchasing patterns rather than sporadic orders. Finally, if you’re willing to pre-sell production to customers before ordering from the mill, you can shift working capital risk and meet minimums more comfortably.

Option 3: Local Distributors and Converters as a Flexibility Lever

Local distributors and regional converters who resell paper in smaller lots represent the highest-convenience, lowest-volume option. This model thrives because it solves a specific problem: immediate access to moderate quantities without the coordination and commitment required by mills or online sourcing.

The typical local distributor stocks common grades and can supply custom-slit sizes or small lots on short notice. They’ve already managed the logistics, import complexity, and quality verification with their upstream suppliers. You’re buying that convenience packaged with the paper itself.

For SME converters, the advantages cluster around flexibility and speed. Lot sizes can be as small as a few tons or even individual pallets for some distributors. Lead times compress dramatically—you might receive material within days rather than weeks. Language and time zone alignment eliminates communication friction. Many distributors offer value-added services like slitting to custom widths, warehousing with just-in-time delivery, or even credit terms if you’ve established a relationship.

The operational simplicity shouldn’t be underestimated. You call or email a local contact who speaks your language during your business hours. Orders are straightforward. Documentation is minimal. Payment processes are familiar. If a quality issue arises, you can often resolve it with a phone call rather than navigating international claims processes.

The price premium is the obvious trade-off. Distributors mark up the paper to cover their own working capital, warehousing, and operational costs. Depending on grade and region, this premium might range from 10% to 30% above mill-direct pricing. For converters operating on thin margins, that differential directly impacts profitability.

Grade breadth may be limited compared to marketplace or mill-direct options. Distributors stock what moves regularly for them, which may not include specialty grades or the exact specifications you prefer. If your requirements fall outside their standard inventory, they’ll often source it for you, but lead times extend and the convenience advantage diminishes.

Price transparency can be opaque. Some distributors adjust pricing based on market conditions, order frequency, and relationship strength rather than publishing clear rate sheets. This lack of standardization makes comparative shopping more difficult.

Local distributors make the most sense in several scenarios. When you need material urgently to cover a customer commitment or production gap, the speed and certainty justify the premium. For new customer relationships in trial phases where order volumes are unpredictable, distributor flexibility reduces risk. When import complexity or freight coordination feels overwhelming—perhaps you’re entering a new market or lack in-house logistics expertise—the distributor’s handling of those details becomes valuable. Seasonal businesses that need to scale purchases up and down rapidly often find distributors more accommodating than mills with fixed production schedules.

The Low-Volume Sourcing Decision Matrix: Putting the Options Side by Side

The following matrix synthesizes everything covered above into a direct comparison. Each cell contains a qualitative score (Low, Medium, High) and a brief explanation.

| Criterion | Online Marketplace | Mill Direct | Local Distributor |

| MOQ & Volume Flexibility | High – Many suppliers willing to quote on smaller lots; easy to find sources that match your consumption patterns. | Low – Mills typically require 40-100 tons minimum; inflexible on partial shipments. | High – Distributors often sell by the pallet or in single-digit tons; extremely flexible. |

| Price-to-Door | Medium – Generally better than distributors but may include freight variables; requires normalizing quotes to same delivery basis. | High (lowest unit cost) – Best per-ton pricing if you can meet MOQs and manage freight efficiently. | Low – Highest per-ton cost due to distributor markup, but price includes delivery and handling. |

| Lead Time & Reliability | Medium – Varies by supplier; some can ship quickly, others match mill timelines; requires verification. | Medium – Predictable for established relationships, but smaller orders may be deprioritized during tight capacity. | High – Fastest fulfillment, often days rather than weeks; local stock available. |

| Working Capital Impact | Medium – Depends on supplier terms; marketplace diversity means you can find options with reasonable payment terms. | Low – Large upfront orders with prepayment or Net 30 at best; cash locked in inventory for months. | Medium to High – Smaller lot sizes reduce cash tied up; some distributors offer Net 45-60 terms for established accounts. |

| Quality Risk | Medium – Quality depends on individual supplier; requires due diligence and trial orders; recourse can be complicated for international suppliers. | High (lowest risk) – Established mills have consistent QC; clear specifications and recourse processes. | Medium to High – Depends on distributor’s upstream relationships; local proximity makes dispute resolution easier. |

| Operational & Admin Load | Medium – Learning curve for platform use; need to vet multiple suppliers; ongoing coordination with international sources. | Medium to Low – High initial onboarding; streamlined once established; formality and time zones may create friction. | High (lowest effort) – Simple communication, minimal documentation, familiar payment processes, easy ongoing orders. |

| Grade Breadth & Availability | High – Access to a wide range of suppliers, geographies, and specialty grades in one place. | Medium – Each mill has a finite range; broadening options requires multiple relationships. | Medium – Limited by distributor’s own sourcing network and working capital; focused on fast-moving grades. |

Use this matrix by marking which criteria currently rate as “critical” (4 or 5 on your importance scale) for your operation. Then look at which channels score best on those critical criteria. That alignment points to your primary sourcing channel.

The matrix is designed to be reusable. Print it, screenshot it, or recreate it in a spreadsheet. As your business situation changes—perhaps cash flow improves, or you sign a large contract that stabilizes volume—you can re-score and see if your optimal channel has shifted.

One crucial point: most successful converters don’t rely on a single channel exclusively. They develop a primary source for core grades and regular orders, maintain a backup option for overflow or emergencies, and keep a third contact for specialty grades or trial orders. The matrix helps you determine which channels fit which roles.

Worked Examples: How the Matrix Changes Real Decisions

Let’s walk through three scenarios showing how different situations lead to different sourcing choices.

Scenario 1: Cash Flow Tight, Demand Uncertain

A 30-employee converter produces small-batch custom boxes for e-commerce brands. Order sizes vary dramatically—one customer might need 500 boxes, another needs 5,000. Monthly paper consumption averages 12 tons but fluctuates between 8 and 18 tons. Cash flow is tight; the owner can’t tie up more than $15,000 in paper inventory at any time.

For this converter, three criteria rate as critical 5s: MOQ Flexibility, Working Capital Impact, and Operational Load. They can’t meet mill minimums without overextending cash. They need suppliers who can ship in small lots and don’t require massive upfront payments.

Scoring the matrix:

- Marketplace performs well on MOQ (high flexibility) and offers medium working capital impact (can find suppliers with Net 30-45 terms). Operational load is medium due to vetting requirements.

- Mill Direct fails immediately—MOQ is too high, and working capital impact is severe.

- Local Distributor scores high on MOQ flexibility and operational simplicity, medium on working capital (smaller lots mean less cash tied up, though terms may require prepayment initially).

Decision: The converter establishes relationships with two local distributors as their primary sources, covering different grades. They use an online marketplace secondarily to find specialty papers and compare prices quarterly, ensuring distributors remain competitive.

This approach costs more per ton than mill-direct would, but the converter maintains the agility to take on short-notice orders without inventory risk. The premium is justified by avoiding the cash crunch that would result from larger orders.

Scenario 2: Stable Contract, Predictable Volume

A 45-employee converter has a three-year contract with a major food packaging company, producing consistent box designs. Monthly consumption is steady at 55 tons of the same two grades. The contract guarantees volume, so the converter can forecast six months ahead with confidence. They have adequate warehouse space and sufficient working capital to support bulk purchasing.

For this converter, Price-to-Door and Lead Time Reliability are critical 5s. Working Capital Impact is a moderate 3—they can handle it, but prefer efficiency. MOQ Flexibility is less important because their volume naturally meets most minimums.

Scoring the matrix:

- Mill Direct scores high on price-to-door and, given their regular volume, medium-high on lead time reliability. Working capital impact is acceptable because predictable sales replenish cash steadily.

- Marketplace offers medium price and medium lead times—better than distributors but not as optimized as mill-direct once established.

- Local Distributor scores poorly on price and doesn’t offer significant advantages given the converter’s scale and stability.

Decision: The converter establishes a mill-direct relationship for both core grades. They negotiate favorable payment terms (Net 45) based on the contract guarantee, order in 50-60 ton lots every 5-6 weeks, and achieve the lowest landed cost. They maintain a marketplace contact as a backup for capacity emergencies or quality issues with the mill, and keep one local distributor relationship for trial orders when testing new designs outside the main contract.

Scenario 3: New Grade Trial for Market Testing

An established converter wants to test demand for a higher-end kraft grade to pursue premium product accounts. They’ve identified potential customers but need to produce samples and fulfill small trial orders before anyone commits to volume. Initial consumption will be under 5 tons over three months.

For this scenario, MOQ Flexibility is a critical 5. Quality Risk is also a 5 because they can’t afford to submit poor samples to premium prospects. Grade Breadth and Availability rates as a 4—they need access to specialty grades they haven’t sourced before. Price-to-Door is a moderate 3—they’re willing to pay more to de-risk the test. Working Capital Impact matters (rated 4) because they’re not yet generating revenue from this grade.

Scoring the matrix:

- Mill Direct is immediately disqualified—no mill will engage for a 5-ton trial of a new grade with an unproven customer.

- Marketplace scores high on MOQ flexibility and grade breadth. Quality risk is medium after proper vetting. Price is medium, working capital impact is manageable if they find a supplier willing to ship in 2-ton increments.

- Local Distributor scores high on MOQ flexibility and medium-high on quality risk (easier to verify and resolve issues locally). Grade breadth is limited—they may not stock the premium grade. Price is higher but operational simplicity is valuable during a test phase.

Decision: The converter sources the initial 2 tons from a local distributor if the grade is stocked, or uses a marketplace to find a specialty supplier willing to ship small trial quantities. This gives them speed and manageable risk. If customer response is positive and volumes grow beyond 10-15 tons monthly, they’ll evaluate mill-direct relationships or lock in a preferred marketplace supplier with better pricing. The marketplace’s broader grade access makes it the more likely long-term choice for this specialty application.

Each scenario demonstrates that the “right” answer isn’t about finding the universally cheapest or fastest channel. It’s about matching your specific volume profile, cash position, and risk tolerance to the channel that best supports your current business reality.

Aligning the Business Owner and Procurement Manager Around One Decision

The Business Owner and Procurement Manager often prioritize different criteria, which can create internal friction when evaluating sourcing channels.

The Business Owner typically focuses on cash flow, profit margin, and growth risk. Their questions center on: “How much capital do we need to tie up?” “What does this do to our cash conversion cycle?” “Does this channel let us take on new opportunities without inventory risk?” They’re often more willing to pay a premium for flexibility and reduced financial exposure.

The Procurement Manager prioritizes supply continuity, process reliability, and supplier performance. Their concerns include: “Will this supplier deliver on time consistently?” “How complex is it to place and track orders?” “What’s our recourse if quality issues arise?” They tend to favor established relationships with predictable processes, even if that means accepting higher MOQs or more rigid terms.

These different priorities lead to classic disagreements. The owner might push for local distributors because the small lot sizes protect cash flow, while procurement resists because the price premium erodes margin. Or procurement might advocate for mill-direct relationships to secure the best price, while the owner worries about the working capital impact.

The decision matrix creates a shared, transparent framework that respects both perspectives. Instead of arguing about “price versus convenience” in the abstract, both stakeholders score the channels against the same criteria with explicit weights reflecting current business priorities.

A simple meeting format helps align the decision:

- List the criteria (MOQ, price-to-door, lead time, working capital, quality risk, operational load, grade breadth)

- Agree on importance weights (owner and manager jointly assign 1-5 scores to each criterion based on current business situation)

- Score each channel (use the matrix as a guide, adjusting scores based on specific supplier quotes or relationships under consideration)

- Document the decision and rationale (record which channel was chosen, why, and what circumstances would trigger a re-evaluation)

This process doesn’t eliminate disagreement, but it forces the conversation to be specific rather than emotional. When the owner and manager both see that Working Capital Impact is rated a 5 due to current cash constraints, and that mill-direct scores poorly on that criterion, the decision becomes logical rather than contentious. Conversely, if cash flow has improved and that criterion drops to a 3, the owner can support procurement’s preference for mill-direct on rational grounds.

The documented rationale serves another purpose: it provides continuity if staff changes occur or if someone questions the decision months later. You can point to the scored matrix and explain the conditions that led to the choice, then reassess whether those conditions still hold.

Turning the Matrix Into a Repeatable Sourcing Playbook

The decision matrix becomes more valuable over time as you refine your scoring based on actual outcomes. Start building a simple sourcing log that captures each major sourcing decision.

For each decision, record:

- Date and context (what prompted the sourcing need)

- Criteria scores (which criteria you rated as critical, and your importance weights)

- Channel scores (how each option scored on the matrix)

- Decision made (which channel you chose and why)

- Outcome (how well the decision performed in practice—delivery reliability, actual cost, quality consistency, ease of management)

After six to twelve months, patterns emerge. You might discover that your initial scoring consistently overestimated or underestimated certain criteria. Perhaps you thought operational load would be a major issue with marketplace sourcing, but in practice it proved manageable. Or maybe you underweighted quality risk initially and experienced problems that taught you to prioritize it more in future decisions.

These learnings let you calibrate the matrix. You’re not changing the framework—the seven criteria remain constant—but you’re adjusting your importance weights and channel scoring to reflect your actual experience rather than assumptions.

Over time, you can extend the matrix beyond kraft paper. The same framework applies to sourcing decisions for other packaging materials, supplies, or services. The criteria labels might shift slightly (for instance, “grade availability” might become “specification customization” for printed components), but the underlying logic of criteria-based comparison remains robust.

This evolutionary approach to sourcing strategy fits the broader principle that informed procurement isn’t about finding a permanent “correct” answer. It’s about building a documented, repeatable process that adapts to your business as it grows and changes. The matrix provides structure without rigidity, making your sourcing decisions more defensible both internally and externally.

For converters looking to develop more comprehensive sourcing capabilities, more guides on agile paper sourcing cover topics like supplier verification processes, international trade considerations, and working capital management techniques that complement this decision framework.

If this matrix clarifies your thinking, the most valuable next step is straightforward: capture your current sourcing situation in it and use the results to frame your next internal discussion about where to buy. When you’re ready to explore more flexible suppliers at volumes that match your scale, consider listing your buying requirements on PaperIndex, a neutral paper marketplace so multiple mills, traders, and distributors can respond.

References

[1] “Working Capital,” Investopedia. https://www.investopedia.com/terms/w/workingcapital.asp

[2] “Working Capital Management: Concept, Importance and Objects,” SRCC (Shri Ram College of Commerce).

[3] “Inventory Management and Working Capital,” Massachusetts Institute of Technology / ScienceDirect. https://www.sciencedirect.com/topics/economics-econometrics-and-finance/working-capital

[4] “Freeing Up Cash from Working Capital,” Harvard Business Review.

[5] “Lead-Time and Demand Variation in Supply Chain Decisions,” Vanderbilt University.

Disclaimer: This article provides educational guidance on sourcing strategy evaluation. Actual sourcing decisions should account for your specific business circumstances, supplier relationships, and market conditions.

Our Editorial Process

Our expert team uses AI tools to help organize and structure our initial drafts. Every piece is then extensively rewritten, fact-checked, and enriched with first-hand insights and experiences by expert humans on our Insights Team to ensure accuracy and clarity.

About the PaperIndex Insights Team

The PaperIndex Insights Team is our dedicated engine for synthesizing complex topics into clear, helpful guides. While our content is thoroughly reviewed for clarity and accuracy, it is for informational purposes and should not replace professional advice.