📌 Key Takeaways

Buying toilet tissue parent rolls the smart way means matching order size to your real cash timeline, not just chasing a lower price per ton.

- Plan in Weeks, Not Tons: Convert every supplier’s minimum order into how many weeks of stock it represents—that number shows your true cash exposure.

- Map When Money Leaves and Returns: Cash goes out at deposit, freight, and customs; it only comes back after you convert, ship, and get paid—often 60 to 120 days later.

- Stress-Test Before You Commit: Add two weeks of shipping delay and surprise fees to your plan; if that scenario threatens payroll, the order is too big.

- Watch for Hope-Based Buying: If your team knows the minimum order but can’t immediately say how many weeks of stock that equals, you’re guessing, not planning.

- Set a Reorder Trigger, Not a Habit: Order when inventory hits a safe threshold and your cash can handle the gap—not just because the warehouse looks low.

Cash trapped in parent rolls can’t pay for repairs, marketing, or sudden opportunities.

Small and mid-sized toilet tissue converters seeking stronger working capital discipline will find a ready-to-use framework here, preparing them for the detailed planning steps that follow.

~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

A toilet tissue parent roll order can look manageable on paper and still trap cash for longer than expected.

The spreadsheet says the MOQ is acceptable. The warehouse still has some stock. The quote looks reasonable enough to keep the toilet tissue converting lines moving. Then the deposit leaves early, transit drifts, charges arrive in uneven waves, and the cash cushion feels thinner than expected. This order looked safe, but the weight of the commitment now threatens liquidity. This is rarely a failure of procurement discipline; rather, it is a failure to account for the simultaneous collision of lead-time exposure, payment timing, and true conversion run-rates. For a small converter, that is a working capital defense problem before it is a purchasing problem.

The goal is not to buy less. The goal is to buy the right amount at the right timing—so cash keeps moving.

Inventory liquidity planning for toilet tissue converters is the practice of matching parent-roll order size, cash-out timing, and run-rate reality so working capital does not get trapped in slow-moving inventory.

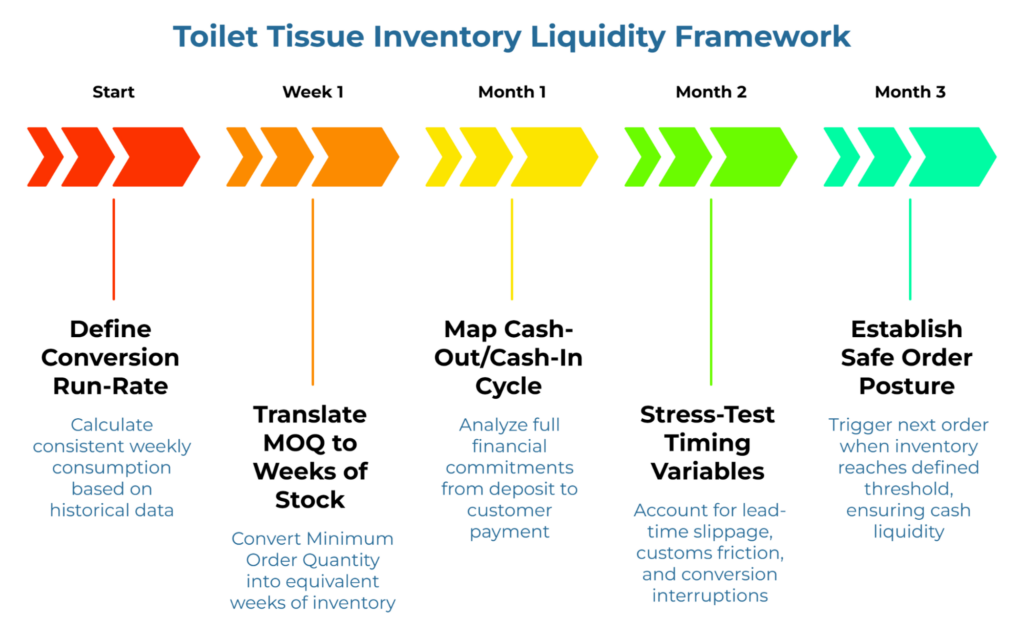

A Simple Toilet Tissue Inventory Liquidity Framework

Start with a simple rule. Effective inventory management often involves planning parent roll procurement based on time, cash flow, and actual converting capacity, rather than relying on tonnage alone.

- A critical first step in this framework is calculating the actual conversion run-rate. Basing these calculations on historical consumption rhythms rather than projected demand helps maintain accuracy. The useful number is not what the business hopes to convert next month. It is what the toilet tissue converting lines can consume consistently, including normal interruptions, waste, and changeovers. Liquidity planning is only as strong as the material assumptions beneath it, which is why specification discipline still matters; toilet tissue parent roll technical specifications are the right baseline when those assumptions are still loose.

- Translating a mill’s Minimum Order Quantity (MOQ) into ‘weeks of stock’ can provide a much clearer operational picture. While a mill MOQ sounds commercial, evaluating it as ‘weeks of stock’ makes it operational. This translation matters because it shows whether the order protects continuity or traps cash tied up in stock. A 20-metric-ton MOQ at 4 metric tons weekly locks five weeks of capital. At a reduced rate of 2.5 tons weekly, that same order sequesters capital for eight weeks—a full bimonthly cycle of idle cash. While a high-volume MOQ may offer a lower unit price, it often forces a small converter into a dangerous inventory-to-cash ratio. The dynamics behind this trade-off are explored more fully in from volume constraints to agility: a guide to overcoming the MOQ barrier.

- Mapping the full cash-out versus cash-in cycle allows operators to analyze the complete sequence of financial commitments. Analyze the full sequence—from initial deposit and freight commitments to duties and final clearance—recognizing that these outflows hit the balance sheet in uneven waves. Cash recovery does not begin when the rolls arrive, either. It begins after toilet paper is converted, shipped, and paid for—a cycle stretching 60, 90, or 120 days depending on customer terms. For small operators seeking to shorten this gap, negotiating payment terms: how to move beyond 100% advance offers a practical script for structuring staged payment arrangements. Payment in March, arrival in April, production through June, customer payment in August. That is five months of working capital locked in one order cycle.

- Resilient plans often stress-test the timing by accounting for variables such as lead-time slippage, customs friction, or a slower-than-average conversion week. What if the shipment arrives two weeks late? What if duties add 8% after payment is already cleared? This is not pessimism. It is a defensive liquidity posture designed to insulate the core operation before the next order is placed. If the stressed scenario threatens payroll, the order is too large.

- Establishing a safe order posture helps protect both production uptime and working capital liquidity. A safe order posture protects uptime and liquidity together. It defines the maximum inventory carrying capacity without weakening operational survival. The practical rule becomes: when inventory reaches a defined threshold of weeks at run-rate, trigger the next order—provided the cash position can absorb the timing gap. The exact buffer will vary by payment terms, transit conditions, and converting speed, but the discipline stays the same.

A useful diagnostic is simple:

| Result | What it means |

| Safe | The order fits the real toilet tissue run-rate and leaves room for normal timing friction. |

| Stressed | The order may work, but only if transit, cash-out timing, and conversion stay close to plan. |

| Dangerous | The order weakens liquidity before converted toilet paper can rebuild cash. |

Why Toilet Tissue Parent Roll Inventory Drains Cash Faster Than Expected

Inventory is not just stock on the floor. It is working capital trapped in physical form. That is why buying more toilet tissue parent rolls is not automatically a stronger move. It can simply be a larger exposure.

Large orders feel efficient. Buying 40 metric tons instead of 20 often unlocks better pricing. The spreadsheet looks favorable. But spreadsheets do not show liquidity cost. Every pallet beyond immediate needs represents capital that cannot be redeployed—not for marketing, equipment repairs, or seizing unexpected opportunities.

Overbuying and underbuying both damage operational resilience. Overbuying locks too much cash into slow-moving bathroom tissue inventory. Underbuying creates stockout risk, unstable production scheduling, and emergency reorder behavior. One weakens liquidity. The other weakens operational continuity. Neither is healthy.

As a general finance principle, the timing of inventory, receivables, and payables shapes cash strain through the broader cash conversion cycle. For converters seeking a deeper understanding of these mechanics, working capital strain from payment terms: a beginner’s cash conversion cycle map for kraft paper buyers offers a practical visual framework that adapts to toilet tissue operations. For small operators, that principle becomes practical very quickly. A parent roll order that looks affordable on quote day can still feel dangerous if the cash-back cycle is vague, the to-door predictability is poor, or the business is already carrying too much material. Basic cash discipline matters here, which is consistent with the U.S. Small Business Administration’s guidance on managing business finances.

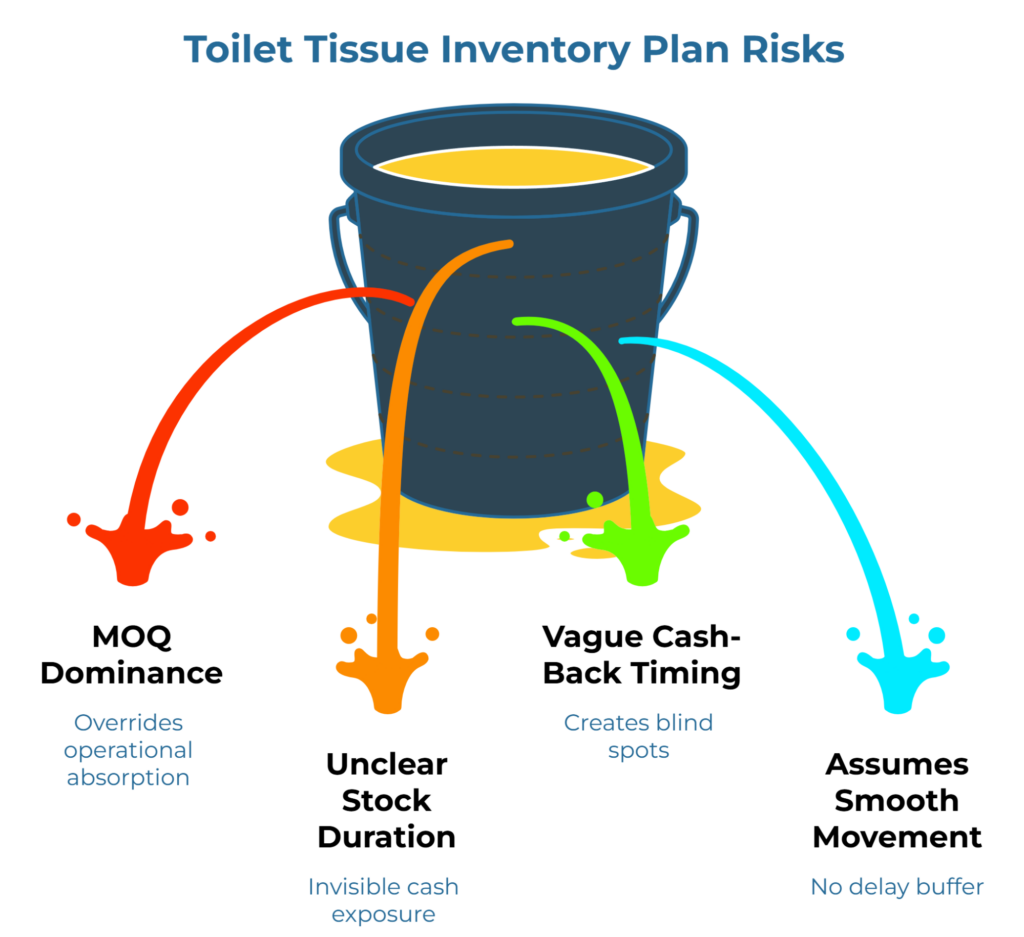

Four Signals That Your Toilet Tissue Inventory Plan Is Becoming Dangerous

Operators often review the following parameters before making their next parent-roll commitment:

- MOQ is driving the decision more than run-rate. The team knows what the mill wants to sell, but not what the operation can safely absorb. If procurement knows the minimum order but cannot state weekly consumption confidently, sizing is based on hope.

- Order tonnage is clear, but stock duration is not. Twenty metric tons sounds concrete. How many weeks does that represent? If nobody can translate the order into weeks of toilet tissue inventory immediately, the cash exposure is invisible.

- Cash-out timing is clear, but cash-back timing is vague. The payment is scheduled, yet the business has not mapped when converted toilet paper will realistically begin refilling liquidity. Payment terms have due dates. Cash-back depends on production pace, sales cycles, and customer behavior. The asymmetry creates blind spots.

- The plan assumes smooth movement. No delay buffer. No hidden timing costs. No stress test for customs, damage, or slower-than-normal conversion. That is not planning—that is hoping.

Where Landed Cost Normalization Fits

Landed-cost normalization belongs inside liquidity planning, not beside it.

A toilet tissue parent roll quoted at competitive EXW can become expensive once freight, duties, and transport are added. Each cost component hits cash at different times. A parent roll order can look acceptable at the quotation stage and still become a cash trap if the to-door picture is incomplete. For the next layer down, a practical framework for normalizing global EXW and CIF toilet tissue raw material specifications is the right companion method.

As a general accounting principle, inventory discipline also sits within formal inventory treatment frameworks such as IAS 2 Inventories. The exact treatment will depend on the business and jurisdiction. The planning lesson here is simpler: clearer timing produces better buying posture.

From Reactive Buying to Financial Defense

The behavior shift is the real upgrade. Elite operators prioritize liquidity over tonnage and timing over unit price, replacing reactive habits with a disciplined procurement posture.

A quick alignment view helps:

| Founder / Owner | Finance Lead | Procurement Lead |

| How much cash is tied up in stock, and for how long? | When does cash leave, and when does it begin coming back? | Is MOQ alignment sound, and is to-door visibility good enough to commit? |

Before the next parent-roll order, review four things. Confirm the real toilet tissue run-rate. Convert the MOQ into weeks of stock. Map cash-out versus cash-back timing. Then test the plan against delay and hidden timing pressure. That sequence is simple, but it is stronger than improvisation.

That is the goal. Not the biggest order. Not the cheapest-looking quote. A safe order posture that keeps the business standing.

This is about safer toilet tissue procurement—not squeezing price.

More toilet tissue procurement guidance is available in the PaperIndex Academy. Once the planning discipline is clear, the next operational step is safer supplier evaluation through established authentication protocols, beyond the broker: three steps to direct toilet tissue raw materials supplier authentication. After that, it becomes reasonable to review bathroom tissue parent roll suppliers with a stronger filter, or browse bathroom tissue mills for broader category awareness.

Frequently Asked Questions

What is inventory liquidity planning in toilet tissue procurement?

It is the discipline of matching toilet tissue parent roll order size, run-rate, and cash timing so working capital does not get trapped in slow-moving inventory.

How do toilet tissue parent roll MOQs affect working capital?

Large MOQs increase the amount of cash committed at one time. A 20-metric-ton MOQ at 4 metric tons weekly locks five weeks of capital; at 2 metric tons weekly, ten weeks. If that quantity represents too many weeks of stock for the real converting rhythm, liquidity pressure rises.

Why is landed-cost visibility important before committing to toilet tissue inventory?

Because the quoted number is not the whole timing picture. Freight, duties, inland movement, and delay risk all affect when cash leaves and how long it stays exposed.

What distinguishes healthy stock from cash-trapping overbuying?

Healthy stock matches run-rate and converts within a planned cycle. Overbuying exceeds absorption pace, locking capital until surplus clears.

Disclaimer:

This content is for informational purposes only and does not constitute financial, accounting, or professional business advice. Working capital requirements, cash-cycle timing, and inventory liquidity vary by operation, payment terms, and market conditions. Consult qualified financial and accounting professionals before making inventory or procurement commitments. Individual outcomes depend on specific circumstances.

Our Editorial Process:

Our expert team uses AI tools to help organize and structure our initial drafts. Every piece is then extensively rewritten, fact-checked, and enriched with first-hand insights and experiences by expert humans on our Insights Team to ensure accuracy and clarity.

About the PaperIndex Insights Team:

The PaperIndex Insights Team is our dedicated engine for synthesizing complex topics into clear, helpful guides. While our content is thoroughly reviewed for clarity and accuracy, it is for informational purposes and should not replace professional advice.