📌 Key Takeaways

A cheap bulk order can become your most expensive inventory if it traps cash and triggers port storage fees.

- Demurrage Starts with Planning, Not Ports: Container fees at the port usually reveal an upstream mistake—an order that was too big for your cash reserves from the start.

- Map Every Cost Before You Commit: Ex-mill prices hide freight, insurance, duties, and handling fees that can double your real cost if you don’t calculate them upfront.

- Match Orders to Your Production Speed: If your converting lines can’t use up the shipment in 60–90 days, the volume is too high—idle rolls mean trapped cash.

- Build Delay Scenarios Into Every Quote: Ask what happens if customs take five extra days; if that cost breaks your budget, the order is too risky.

- Normalize Quotes to the Same Basis: Comparing EXW to CIF prices without adjusting for who pays what creates false savings that vanish at the port.

Small order savings beat big order headaches.

Finance leads and procurement managers at SME toilet tissue converters will sharpen their MOQ decisions here, preparing them for the detailed framework that follows.

~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

The finance lead at a growing toilet paper converting plant stares at a supplier quote. The ex-mill price looks sharp. The minimum order quantity stretches cash reserves, but the per-ton savings seem to justify the commitment. Three weeks later, a container sits at port. Customs clearance has stalled. Storage charges tick upward daily. The “smart” raw material purchase is quietly bleeding the business dry.

You have likely felt this tension before: the pressure to lock in volume while your working capital screams for protection. The anxiety of committing limited cash to a shipment when the true landed cost remains foggy. The fee itself is just a symptom. The root cause almost always traces back to an MOQ decision made weeks earlier, without full respect for run rates, cash reserves, or realistic to-door exposure.

With a clearer understanding of how MOQ miscalculations in bulk substrate procurement erode profit margins, you can make procurement commitments that protect cash flow instead of jeopardizing it.

What the Demurrage Trap Really Means for Toilet Tissue Converters

Demurrage is the fee typically assessed by the ocean carrier for the extended use of a container beyond its allotted free time. This charge often compounds alongside separate port storage fees levied by the terminal itself. For a small bathroom tissue converter, this fee carries weight far beyond its invoice line. It often marks the moment where theoretical savings are offset by actual liquidity outflows.

The trap works like this: when a jumbo roll shipment sits at port, the real problem is rarely the port itself; rather, working capital was already stretched by an oversized order. Flexibility vanished before the container even arrived. There is no buffer left to absorb a delay, expedite paperwork, or cover unexpected charges without squeezing other operations.

A demurrage problem is often a planning problem wearing a logistics label.

This is why experienced procurement teams treat demurrage exposure as a planning discipline, not a logistics accident. The container sitting at port is the consequence. The cause lives in the MOQ decision that ignored what happens between the mill gate and the converting line. Working-capital defense is not a finance-side detail. It is part of the procurement decision itself.

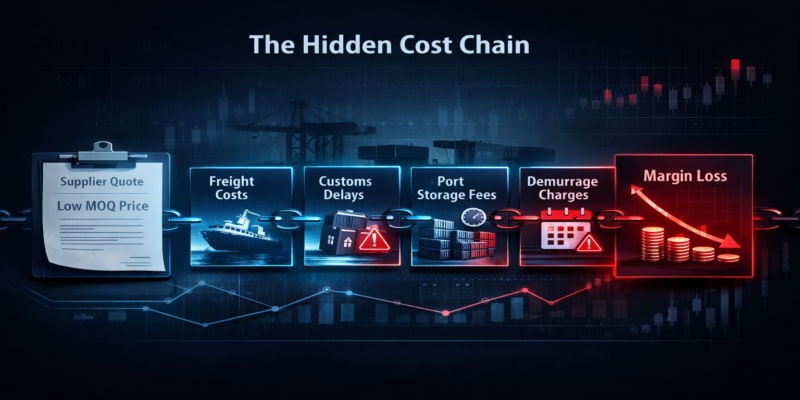

How a Bulk Substrate MOQ Error Turns into a Port-Cost Problem

The path from MOQ miscalculation to margin collapse follows a predictable chain reaction:

- The buyer sets the MOQ too aggressively, committing volume based on per-ton price rather than operational fit.

- More cash gets locked in toilet tissue inventory than planned. Working capital that should cover other obligations is now tied to parent rolls in transit.

- Flexibility disappears when friction appears. Customs documentation takes longer than expected. Freight timing shifts. A clearance fee surfaces. The business has no financial room to respond.

- Delay lengthens exposure. Each additional day at port compounds the problem. Free storage windows expire.

- Port storage and related charges start multiplying. Demurrage, detention, and handling costs stack.

- Margin on the shipment collapses. The unit-cost advantage that justified the stretch evaporates—often into a net loss.

This sequence explains why two toilet paper converters buying from the same supplier, at the same ex-mill price, can have completely different outcomes. The difference is not the supplier. It is MOQ alignment and the working capital buffer behind the order.

Why the Cheapest Toilet Tissue Raw Material Order Can Become the Most Expensive Shipment

Unit price thinking is the most common trap in toilet tissue parent roll procurement.

A low ex-mill quote looks like a win. The ex-mill number is only one input in a much larger landed cost equation—a reality explored in depth in the landed-cost framework for kraft paper: from Incoterms to to-door comparability, which applies the same methodology across paper grades. Consider what that attractive quote typically excludes: freight from mill to port of origin, export documentation, ocean freight, marine insurance, customs duties at destination, terminal handling, port storage if clearance stalls, and inland transport to the converting plant.

Depending on the trade corridor and the agreed Incoterms rules, most of these costs sit outside the quoted price. An EXW quote places every one of them on the buyer. A CIF quote covers more but still leaves destination port charges, duties, and inland freight unaccounted for.

A cheap primary stock quote does not guarantee a safe procurement decision. Accepting a low ex-mill MOQ without mapping the full to-door cost is not making a purchasing decision. That converter is making a guess. When that guess meets unexpected port congestion, documentation delays, or a currency swing, the “cheapest” order can easily become the most expensive toilet tissue inventory on the balance sheet.

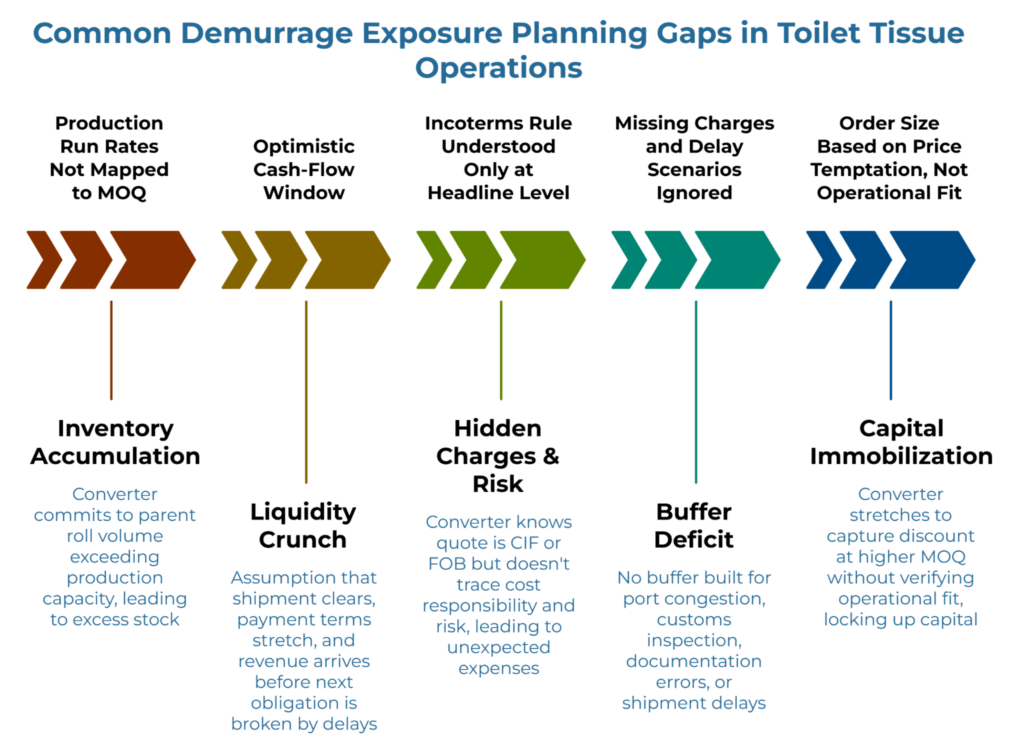

Where SME Converters Usually Miscalculate

Most demurrage exposure traces back to a handful of planning gaps that repeat across SME bathroom tissue operations.

Production run rates are not mapped to the MOQ. The converter commits to a toilet tissue parent roll volume that exceeds what the converting lines can consume in a reasonable timeframe. Inventory sits. Cash stays locked. When the next order is needed, liquidity has already been consumed.

The ‘cash-flow window’ is too optimistic. The assumption is that the shipment will clear quickly, payment terms will stretch far enough, and revenue from converted toilet paper will arrive before the next obligation. One delay breaks the entire assumption.

The Incoterms rule is understood only at headline level. The converter knows the quote is CIF or FOB but does not trace exactly where cost responsibility and risk transfer. The ICC Incoterms 2020 rules define these boundaries precisely, yet hidden charges accumulate in the gap between what the Incoterm covers and what the buyer assumed it covered. While the WTO Trade Facilitation Agreement sets global legal frameworks for expediting the release of goods, databases like the World Bank Logistics Performance Index provide the actual quantitative context on how customs efficiency and shipment timeliness vary across specific trade corridors. Relying on aggregate data without corridor-specific variance modeling creates a ‘Liquidity Gap’ when actual Lead Time (LTa) exceeds planned Lead Time (LTp).

Missing charges and delay scenarios are ignored. No buffer is built for port congestion, customs inspection, documentation errors, or the simple reality that international toilet tissue shipments do not always move on schedule.

The order size is based on price temptation, not operational fit. The supplier offers a better per-ton rate at a higher MOQ. The converter stretches to capture the discount without verifying that the volume, timing, and cash exposure actually fit the business. Toilet tissue parent rolls that cannot be converted and sold on a healthy cycle are not just stock. They are capital that has stopped moving.

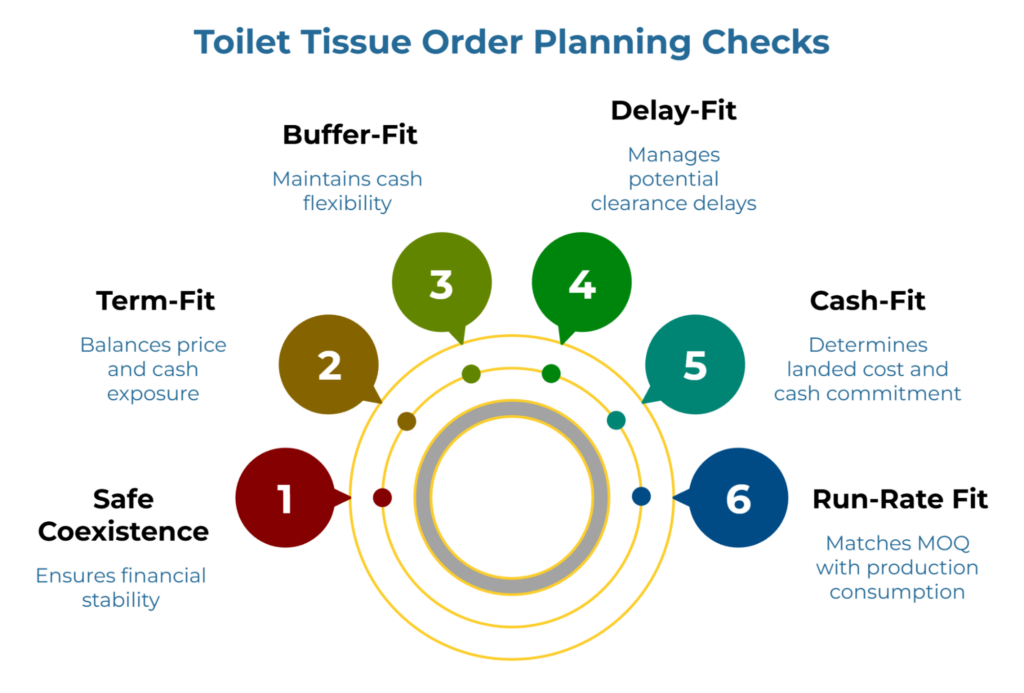

What to Check Before Committing to an Oversized MOQ

Before signing off on a toilet tissue parent roll order, a disciplined converter runs through five planning checks.

- Run-rate fit: Does this MOQ match actual production consumption? If the order volume exceeds what the converting lines will consume within your internally benchmarked working capital cycle (such as your specific Cash Conversion Cycle [CCC] and available warehouse floor time), the MOQ may be too large. Inventory that sits is cash that cannot work elsewhere.

- Cash-fit: What is the realistic to-door cost, and how much working capital gets committed before the material generates finished-goods revenue? Map every cost element from mill to converting plant. If the quote is EXW or FOB, add freight, insurance, duties, terminal handling, and inland transport. If the quote is CIF, add destination port charges, duties, and inland freight. The goal is a single, comparable landed-cost figure—not a headline price.

- Delay-fit: What happens if clearance takes five days longer than expected? Build a delay scenario. If the shipment sits at port past the free storage window, what are the daily demurrage and storage charges? Can the business absorb that cost without disrupting other operations?

- Buffer-fit: Is there a cash buffer between this order and the next obligation? If the toilet tissue jumbo roll shipment ties up all available working capital, flexibility disappears. One unexpected fee or delay can cascade into missed payments, emergency borrowing, or operational disruption.

- Term-fit: Is this volume chosen because it fits, or because the unit price is tempting? A lower per-ton cost is meaningless if total cash exposure exceeds what the business can safely carry. The right MOQ balances price, run rate, cash flow, and risk—not the one that looks best on a unit-cost spreadsheet.

The goal is not to eliminate all uncertainty. The goal is to stop pretending that a thin cash position and an oversized toilet tissue MOQ can safely coexist.

How This Connects to Quote Normalization and To-Door Planning

MOQ discipline is not a standalone fix. It is one part of a broader normalization mindset that protects toilet tissue converters from hidden cost exposure.

When quotes from different suppliers arrive on different Incoterm bases, with different payment terms and delivery timelines, direct comparison is impossible. A normalized approach converts every quote to a common to-door basis so the true landed cost of each option becomes visible before any commitment is made.

The sequence matters: first operating fit, then quote normalization, then landed-cost discipline, then commitment.

This is where better MOQ planning connects to the rest of the procurement process. Understanding how to standardize global quotes builds comparability into the quoting process itself. Learning a practical framework for normalizing EXW and CIF toilet tissue specifications shows how to convert quotes on different Incoterm bases to a like-for-like landed cost. Knowing how to strip hidden variables from RFQ surfaces costs before they become surprises. And for a related warning on false savings, understanding why chasing the cheapest destroys yield reinforces the same business-case discipline.

The safest next move is not “buy less at any cost.” It is to choose a toilet tissue MOQ that matches run rates, cash tolerance, and a realistic to-door cost model. When MOQ planning is grounded in ‘working capital defense’, Incoterm clarity, and to-door landed-cost thinking, the shipment becomes easier to absorb long before it reaches the port. That is how small converters start acting like enterprise-grade buyers—through better methodology, not bigger risk appetite.

Once your MOQ logic is grounded in realistic landed-cost assumptions, the next step is to evaluate bathroom tissue parent roll suppliers on a normalized, to-door basis to build a shortlist of bathroom tissue mills. For deeper methodology, the PaperIndex Academy offers additional guides on quote normalization and landed-cost planning.

Frequently Asked Questions

What is demurrage in toilet tissue imports?

Demurrage is the fee charged when a shipping container remains at a port terminal beyond its allotted free storage period. For toilet tissue parent roll imports, demurrage typically begins after a grace period of a few days and compounds daily until the container is cleared and removed. The charge is imposed by the port or terminal operator and can escalate quickly if customs clearance or documentation issues cause extended delays.

How is detention different from demurrage?

Demurrage usually relates to time a container spends at the terminal beyond the allowed free period. Detention usually relates to time equipment remains outside the terminal beyond the allowed period after pickup. The exact commercial treatment can vary by carrier and contract, so the shipping documents and trade terms need to be checked carefully. Both charges matter because they compound when a toilet tissue shipment is already operationally fragile.

Can a cheap toilet tissue bulk order become more expensive than a smaller order?

Yes. A low ex-mill price does not guarantee a low total cost. If a large toilet tissue parent roll order ties up working capital, exceeds production run rates, or encounters customs delays that trigger demurrage and storage fees, the landed cost can exceed what a smaller, better-aligned order would have cost. The cheapest quote often produces the worst margin outcome when hidden costs are ignored.

What should a small toilet tissue converter think about MOQ?

A small converter should match the MOQ to three realities: the rate at which converting lines consume parent rolls, the ‘cash-flow window’ available to carry the inventory, and the realistic to-door cost including delay scenarios. An MOQ that looks attractive on a unit-cost basis but exceeds operational capacity or cash reserves is not a good deal—it is a liquidity risk.

Why does Incoterm choice affect toilet tissue margin risk?

The Incoterm defines where cost responsibility and risk transfer from seller to buyer. An EXW quote places nearly all logistics costs and risks on the buyer. A CIF quote covers freight and insurance to the destination port but still leaves port charges, duties, and inland transport on the buyer. A converter who misunderstands where Incoterm coverage ends will underestimate true exposure and may face unexpected costs that destroy margin.

Disclaimer:

This article is for educational and informational purposes only. Readers should verify assumptions with qualified customs, logistics, finance, and legal professionals before making procurement commitments.

Our Editorial Process:

Our expert team uses AI tools to help organize and structure our initial drafts. Every piece is then extensively rewritten, fact-checked, and enriched with first-hand insights and experiences by expert humans on our Insights Team to ensure accuracy and clarity.

About the PaperIndex Insights Team:

The PaperIndex Insights Team is our dedicated engine for synthesizing complex topics into clear, helpful guides. While our content is thoroughly reviewed for clarity and accuracy, it is for informational purposes and should not replace professional advice.