📌 Key Takeaways

A 15-day shift in payment terms isn’t a minor adjustment—it can double or eliminate your working capital needs entirely.

- Payment Terms Create Real Cash Gaps: The days between paying your kraft paper supplier and collecting from your customer represent actual cash you must fund through overdrafts, reserves, or delayed payments.

- 15 Days Can Double Your Funding Needs: When your supplier moves from Net 45 to Net 30 while your customer stays at Net 60, your working capital requirement jumps from ₹15 lakh ($18K) to ₹30 lakh ($35K) on a ₹30 lakh ($35K) monthly spend.

- The Formula Makes It Negotiable: Calculate your exposure with “Monthly kraft paper spend × (cash gap days ÷ 30)” to turn emotional supplier conversations into fact-based discussions about who bears the financing burden.

- Alignment Beats Everything: A customer paying on Net 45 while you pay suppliers on Net 45 eliminates the payment terms gap entirely, freeing up capital that was previously locked in the cycle.

- Extreme Mismatches Compound Fast: A 30/90 structure (paying suppliers at 30 days, collecting from customers at 90 days) creates a 60-day gap requiring ₹60 lakh ($70K) in funding—four times the baseline scenario.

Show the numbers, not just the stress.

SME packaging converters buying kraft paper—especially owners, finance heads, and procurement leads—will find concrete scenarios here, preparing them for the actionable frameworks and negotiation tools that follow.

The bank calls to discuss your overdraft limit. Again. Your supplier emails asking for payment 15 days earlier. Your largest customer hints they’ll need 15 extra days to pay their next invoice. Everyone says “it’s just 15 days,” but the knot in your stomach says otherwise.

You’re right to worry. For SME packaging converters buying kraft paper, those 15 days aren’t abstract numbers on a spreadsheet. They represent real cash sitting idle between the day you pay your mill and the day your customer finally settles their account. When you’re already juggling tight margins and month-end anxiety, even small changes in payment terms can turn manageable cash flow into a funding crisis.

This article walks through simple, copyable scenarios that show exactly how a 15-day shift—whether from your supplier tightening terms or your customer stretching them—changes the actual cash gap you need to fund. No complex formulas. Just clear numbers you can use in your next supplier negotiation, customer discussion, or bank review meeting.

Working Capital Strain from Payment Terms in One Clear Picture

Working capital strain from payment terms is a structural cash-flow problem where the timing and length of supplier and customer payment terms create a gap that forces SME packaging converters to lock up more cash in kraft paper inventory than their working capital can comfortably support. In standard finance language, working capital is simply current assets minus current liabilities—a basic measure of how much short-term funding is available to run the business day to day. The cash conversion cycle describes how long cash is tied up between paying suppliers and collecting from customers.

Picture having to pay for all the kraft paper weeks before you see any money from the customers using it. As orders grow, paper purchases grow first while customer payments lag behind, leading to tense supplier calls, hurried bank meetings, and constant juggling of which invoice to pay next. To regain control, converters need to map their cash conversion cycle and identify levers—payment terms, inventory policies, and financing tools—to shrink or safely fund the gap.

This article zooms in on one specific change: what happens when payment terms shift by 15 days. We’ll use consistent numbers across all scenarios so you can see exactly how that shift translates into days of cash exposure and approximate funding needs.

How to Read a Simple Supplier-Customer Terms Timeline

Before diving into scenarios, picture your cash flow as a left-to-right timeline. On the left, you receive kraft paper from your supplier. On the right, your customer pays you for the finished packaging. Between those two points, your cash is locked.

The timeline has three key markers:

Supplier payment date: The day you must pay your kraft paper mill. If terms are “Net 45,” you pay 45 days after receiving the shipment.

Customer payment date: The day your customer pays you for the finished goods. If terms are “Net 60,” they pay 60 days after you invoice them.

The gap (your cash exposure): The number of days between when you pay out and when cash comes back in. You can calculate this with a simple formula:

Payment Terms Gap (days) = Customer credit terms – Supplier credit terms

If you pay your supplier on day 45 but don’t collect from your customer until day 60, your gap is 15 days. Every day in that gap represents cash you need to fund from somewhere—your bank, your reserves, or by delaying other payments.

A note on inventory days: In a standard Cash Conversion Cycle (CCC), you must also fund the time paper sits in your warehouse (Inventory Days). However, to isolate the financial impact of your contract negotiations, this article focuses strictly on the ‘Terms Gap’—the funding void created solely by the difference in payment schedules. While your total working capital need will be higher due to inventory, this Terms Gap represents the specific cash flow variable you can control directly through negotiation.

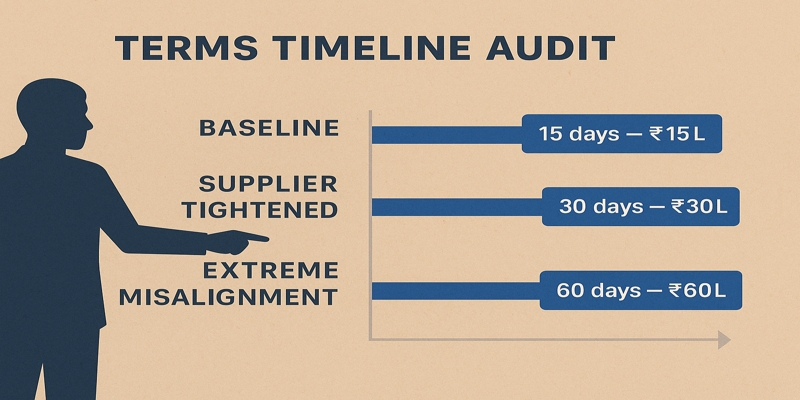

Scenario 1: Baseline Terms and Cash Gap

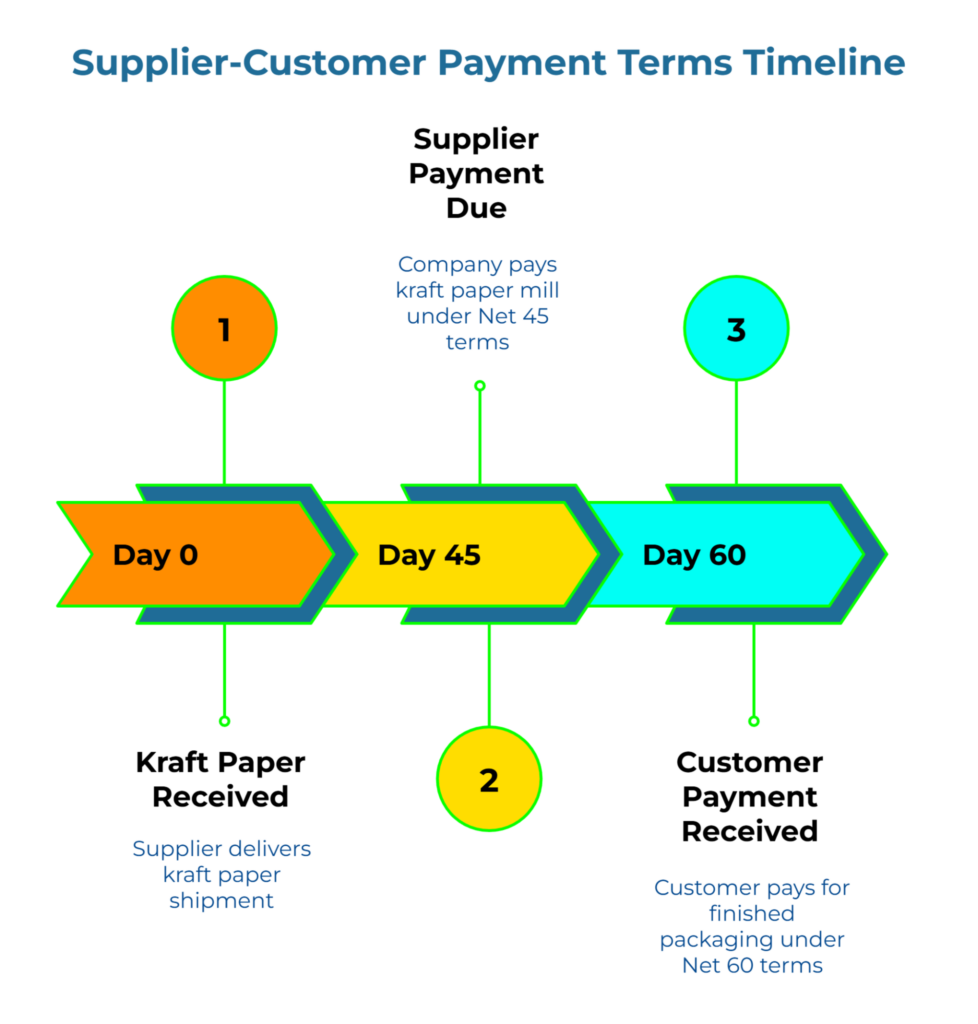

Let’s start with a realistic baseline. Your kraft paper supplier offers Net 45 terms, meaning you pay 45 days after delivery. Your customer pays on Net 60 terms, settling their invoice 60 days after you bill them. Your monthly kraft paper spend is ₹30 lakh ($35K).

Here’s what that timeline looks like:

- Day 0: You receive kraft paper from your supplier

- Day 45: You pay your supplier ₹30 lakh ($35K)

- Day 60: Your customer pays you

Cash gap: 15 days (from day 45 to day 60)

To calculate the approximate cash tied up during this gap, first determine your daily spend:

Daily kraft paper spend = ₹30 lakh ($35K) ÷ 30 days = ₹1 lakh ($1.1K) per day

Then multiply by the gap days:

₹1 lakh ($1.1K) per day × 15 days = ₹15 lakh ($18K)

You need ₹15 lakh ($18K) of available liquidity—whether from cash reserves, an overdraft line, or trade finance—just to bridge the 15-day window between paying your mill and getting paid by your customer.

This is your baseline. It feels tight, but manageable. Now let’s see what happens when terms change.

Scenario 2: Supplier Tightens Terms by 15 Days

Your supplier calls. Market conditions are shifting, and they need payment earlier. Instead of Net 45, they’re moving to Net 30. Your customer’s terms stay the same at Net 60.

New timeline:

- Day 0: Kraft paper delivery

- Day 30: You pay your supplier ₹30 lakh ($35K) (15 days earlier than before)

- Day 60: Your customer pays you

Cash gap: 30 days (from day 30 to day 60)

New cash requirement:

₹1 lakh ($1.1K) per day × 30 days = ₹30 lakh ($35K)

Your working capital needs just doubled. That extra 15 days means you now need ₹30 lakh ($35K) in funding instead of ₹15 lakh ($18K). If your overdraft limit is already near its ceiling, this change alone could push you over the edge.

As a general principle, whenever supplier terms move closer while customer terms stay where they are, the funding gap between suppliers and customers widens, and the business carries more working capital strain from payment terms.

Scenario 3: Customer Improves Terms by 15 Days

Now imagine a different scenario. Your supplier stays at Net 45, but your customer—perhaps trying to strengthen the relationship or secure priority supply—agrees to pay you 15 days faster. They move from Net 60 to Net 45.

Timeline:

- Day 0: Kraft paper delivery

- Day 45: You pay your supplier ₹30 lakh ($35K)

- Day 45: Your customer pays you

Cash gap: 0 days

Cash requirement: ₹0 ($0)

Your payments and collections are perfectly aligned. You’re no longer funding a gap with borrowed money or delayed bills. This is the ideal state most converters dream about but rarely achieve. This single 15-day improvement from a major customer can free up working capital equivalent to ₹15 lakh ($18K) versus the baseline scenario, and ₹30 lakh ($35K) versus the tightened supplier scenario.

Scenario 4: Extreme Misalignment Shows the Real Risk

Here’s a structure contrast that shows how severe the problem can become. Imagine your supplier tightens to Net 30, while your customer—facing their own cash pressures—stretches payment from Net 60 to Net 90.

Timeline:

- Day 0: Kraft paper delivery

- Day 30: You pay your supplier ₹30 lakh ($35K)

- Day 90: Your customer pays you

Cash gap: 60 days (from day 30 to day 90)

Cash requirement:

₹1 lakh ($1.1K) per day × 60 days = ₹60 lakh ($71K)

You’ve gone from a ₹15 lakh ($18K) working capital need in the baseline to ₹60 lakh ($71K). That’s a fourfold increase. The average number of days in these structures can look similar when discussed vaguely, but the working capital squeeze from payment terms in this extreme scenario is four times heavier in cash. This is where the kraft paper cash flow gap stops being an abstract “cash flow issue” and becomes a clear funding gap between suppliers and customers that can cripple growth.

The Mini-Scenarios Comparison Table

Here’s how all four scenarios stack up side by side:

| Scenario | Supplier Terms | Customer Terms | Cash Gap (Days) | Approx. Cash Tied Up |

| Baseline | Net 45 | Net 60 | 15 | ₹15 lakh ($18K) |

| Supplier tightens | Net 30 | Net 60 | 30 | ₹30 lakh ($35K) |

| Customer improves | Net 45 | Net 45 | 0 | ₹0 ($0) |

| Extreme misalignment | Net 30 | Net 90 | 60 | ₹60 lakh ($71K) |

Illustrative values assuming ₹30 lakh ($35K) monthly kraft paper spend and a 30-day month.

The purpose of this mini-scenarios table is clarity, not precision. It helps different stakeholders see, at a glance, how 15-day shifts change both the cash gap in days and the approximate cash locked inside kraft paper.

To adapt the table to your own situation:

- Replace ₹30 lakh ($35K) with your own monthly kraft paper spend for one core supplier-customer combination

- Plug in your actual supplier and customer terms for each scenario you want to test

- Recalculate the approximate cash using the same rule of thumb: Monthly kraft paper spend × (cash gap days ÷ 30)

The table can be printed, screenshotted, or dropped into a one-page slide so that the working capital squeeze from payment terms is visible to everyone, not just hidden in the finance head’s spreadsheet.

How to Use This Table in Real Conversations

These scenarios aren’t just academic exercises. They’re conversation starters.

With your supplier: “I understand you need faster payment, but moving from Net 45 to Net 30 doubles my working capital requirement from ₹15 lakh ($18K) to ₹30 lakh ($35K). Can we phase this in over three months, or can you offer a small early-payment discount to offset my increased financing costs?”

With your customer: “You’re asking for Net 75 instead of Net 60. That adds another 15 days to my cash gap. If we move forward with that change, I’ll need to adjust pricing by 2% to cover the additional financing burden, or we can keep current terms and current pricing.”

With your bank: Instead of walking into your quarterly review with vague statements about “cash flow challenges,” you show this table. You explain: “Here is our main 30/90 structure. It creates a 60-day cash gap and ties up around ₹60 lakh ($71K) in kraft paper funding. This is what the overdraft is actually supporting.” You demonstrate that you understand your cash conversion cycle and have a plan to manage it.

Internal conversations with your owner or managing director: The table helps move from “cash is tight” to “we are carrying ₹30 lakh ($35K) because of this 30-day gap.” That shift makes decisions about pricing, terms, and growth more grounded.

With operations and procurement: The numbers show that working capital is the shock absorber for the plant. A lower price with tougher supplier terms may create more cash conversion cycle pressure than a slightly higher price with better payment terms.

Across all these conversations, the key is the same: show days and cash side by side so discussions about working capital strain from payment terms become more concrete and less emotional.

Common Traps When Thinking About Payment Terms

Many converters fall into predictable traps when they’re under pressure to accept term changes.

Trap 1: Treating all 15-day shifts as equal. A 15-day improvement from your customer (moving you from a 15-day gap to zero) is worth more than a 15-day worsening (moving you from 15 days to 30 days) because it eliminates your financing need entirely. Don’t negotiate them as equivalent trades.

Trap 2: Ignoring the cumulative effect. If you have three major kraft paper suppliers and each tightens terms by 10 days, the stress on your cash flow triples. You aren’t just finding funding for a 10-day gap on one invoice; you are accelerating your entire accounts payable schedule. This means you must fund that 10-day gap across your total procurement volume simultaneously, significantly spiking your overdraft utilization.

Trap 3: Assuming you can always get more credit. Your bank’s willingness to extend your overdraft limit depends on their assessment of your business health. If you keep requesting higher limits because payment terms keep shifting against you, they’ll eventually see you as a higher risk and either charge more or say no.

Next Steps: Build Your Own Scenario Map

Now that you’ve seen how 15-day changes affect working capital, you can build your own scenario map. List your top three kraft paper suppliers and their current terms. List your top three customers and their terms. Calculate the gap for each supplier-customer pair.

Once you have that map, you’ll see where your biggest exposures are. You might discover that one supplier’s aggressive terms are offset by one customer’s fast payment, so that pairing is fine. But another supplier-customer combination might be creating a 50-day gap that’s quietly draining your cash reserves every month.

For a more comprehensive look at mapping your entire cash conversion cycle—including inventory days, supplier variability, and seasonal spikes—explore our guide: Working Capital Strain from Payment Terms: A Simple Guide to Seeing and Fixing Your Kraft Paper Cash Flow Gap.

If you’re just starting to think about these dynamics and want a beginner-friendly introduction to the cash conversion cycle itself, start with: Working Capital Strain from Payment Terms: A Beginner’s Cash Conversion Cycle Map for Kraft Paper Buyers.

For broader background on concepts such as working capital and the cash conversion cycle, these Investopedia references provide high-authority explanations of the foundational finance concepts.

Over time, the scenarios and mini-scenarios table can be expanded to include more suppliers and customers. For now, even a single clear line—showing how a 15-day change affects your kraft paper cash flow gap—can reduce uncertainty, support better negotiations, and make month-end feel more manageable.

From Anxiety to Alignment

Remember the finance head who realized they’d never mapped the days between paying the mill and getting paid by their top customers? They built a simple table like the one above. It took less than an hour. When their largest supplier asked to move from Net 45 to Net 30, they didn’t panic. They showed the supplier the numbers, explained the cash impact, and negotiated a phased transition with a 1% early-payment discount that made the change manageable.

Remember the owner who walked into a bank review with only gut feel? They brought a one-page summary of their supplier-customer term gaps instead. The bank approved a modest overdraft increase because they could see the owner understood their cash conversion cycle and had a plan to manage it.

Working capital strain from payment terms isn’t an abstract finance concept. It’s the difference between a month-end that feels manageable and a month-end that feels dangerous. When you treat payment terms as design levers—not fixed constraints—you give yourself the power to negotiate, plan, and grow without constantly maxing out your credit lines.

The scenarios in this article aren’t predictions. They’re tools. Use them.

Disclaimer

This article shares general, illustrative information about working capital, payment terms, and cash-flow management for SME packaging converters. It does not constitute financial, legal, tax, or investment advice. Always consult qualified professionals and your own financial records before making decisions about credit limits, financing, or contract terms.

Our Editorial Process

Our expert team uses AI tools to help organize and structure our initial drafts. Every piece is then extensively rewritten, fact-checked, and enriched with first-hand insights and experiences by expert humans on our Insights Team to ensure accuracy and clarity.

About the PaperIndex Insights Team

The PaperIndex Insights Team is our dedicated engine for synthesizing complex topics into clear, helpful guides. While our content is thoroughly reviewed for clarity and accuracy, it is for informational purposes and should not replace professional advice.