📌 Key Takeaways

Budget surprises in folding cartons come from vague specifications and mixed quote terms—not from spreadsheet errors.

- Specifications Come First: Define exact tolerances and test methods before asking suppliers for prices, or every quote means something different.

- Same Terms for All: Make every supplier quote on identical commercial terms—same delivery point, same Incoterms—so you can actually compare.

- Normalize to Your Door: Add freight, duties, and handling to each quote until they all reflect the same landed cost at your facility.

- Govern the Process: Assign clear owners for specifications, quotes, and assumptions—then review on a fixed schedule to prevent silent drift.

- Sequence Is Fixed: Tolerances → RFQs → normalization → budget model—skip a step and the next one inherits garbage.

Comparable inputs create predictable budgets.

Procurement managers, operations leads, and finance professionals in folding carton-buying organizations will find a ready-to-use framework here, setting up the stage-by-stage implementation guide that follows.

~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

Folding carton cost overruns trace back to one root cause: vague specifications that produce incomparable quotes. This article presents a four-stage transition—Define Tolerances, Issue Specification-True RFQs, Normalize Landed Costs, Build Budget Governance—that aligns Procurement, Operations, and Finance around a shared sequence.

Why Folding Carton Cost Predictability Fails Before the Spreadsheet

The spreadsheet said one thing. The invoice said another.

A procurement manager reviews a quarterly cost report that missed the forecast by double digits. The suppliers delivered on time. The volumes matched the purchase orders. Yet the numbers diverged anyway, and nobody can explain why with confidence.

The instinct is to blame the spreadsheet model or question the finance team’s assumptions. But the real problem started months earlier—long before anyone opened a forecasting template.

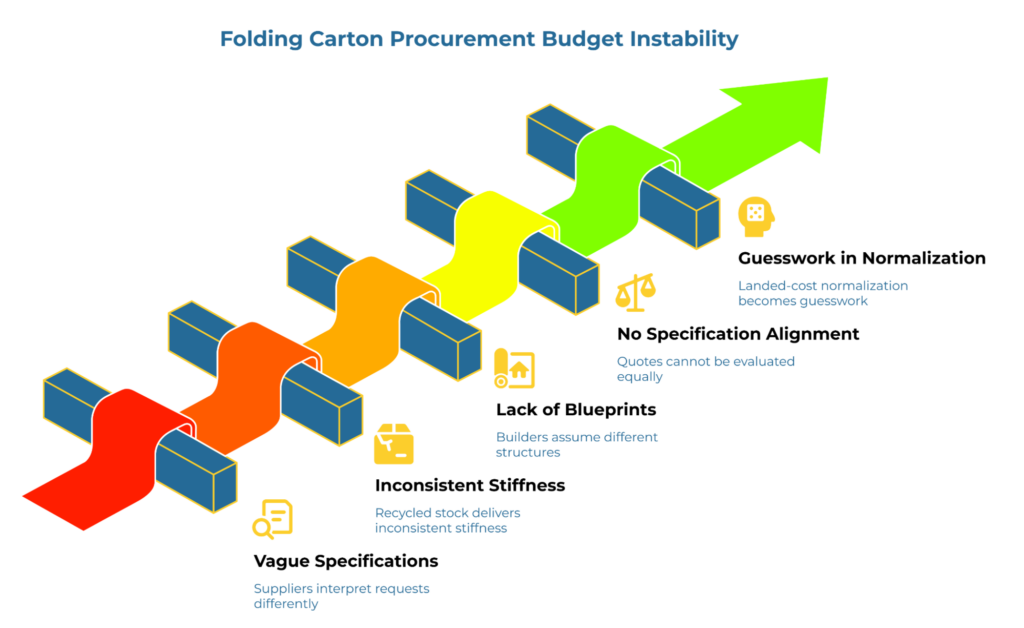

Budget instability in folding carton procurement—whether sourcing from packaging paper suppliers domestically or internationally—rarely originates in the spreadsheet. It originates upstream, in the gap between what buyers think they specified and what suppliers actually quoted. When an RFQ asks for “folding cartons, food-safe” without defining caliper tolerances, test methods, or barrier requirements, every supplier interprets the request differently. One quotes a virgin board with a premium coating. Another quotes recycled stock that technically meets the weight target but delivers inconsistent stiffness. Both quotes look comparable on paper. Neither reflects the same product. That is false comparability—and it is the silent cause of most budget surprises.

This is the architectural-blueprint problem. Imagine asking three builders to quote a house without giving them blueprints. One assumes a two-car garage. Another assumes no garage at all. A third includes a basement you never mentioned. The quotes arrive, and they vary wildly. Comparing them is meaningless because each builder priced a different structure.

The same dynamic plays out in folding carton procurement. Without rigorous specification alignment—the Specification-True Mindset that treats comparability as a prerequisite to price comparison—quotes cannot be evaluated on an equal basis. If quotes cannot be compared, landed-cost normalization becomes guesswork. And if landed-cost normalization is guesswork, the budget model becomes fiction dressed as finance.

The Four-Stage Transition: From Specifications to Spreadsheets

The path from chaotic RFQs to reliable budgets follows a strict sequence. Skipping stages or reordering them breaks the logic chain and reintroduces the unpredictability the process is designed to eliminate.

Each stage builds on the previous one. Define tolerances first, then issue structured RFQs, then normalize quotes to a common cost basis, and only then build the budget model. The sequence matters because each stage removes a different source of noise. Stage 1 eliminates specification ambiguity. Stage 2 eliminates commercial assumption variance. Stage 3 eliminates cost-basis misalignment. Stage 4 locks the inputs into a governed model. A budget built on unnormalized quotes is noise. Unnormalized quotes built on vague specifications are fiction.

Stage 1: Define Tolerances Before Asking for Prices

The first stage establishes what “comparable” means. Without it, nothing downstream works.

Many folding carton buyers generally understand that they need to specify dimensions and material type. However, material basics alone cannot guarantee quote comparability. Two suppliers quoting the same nominal board weight can deliver products with meaningfully different caliper, stiffness, and moisture behavior—all within the range of what “meets spec” could mean when the specification lacks precision.

The solution is parameter discipline. Before requesting any quotes, define the measurable characteristics that matter to production performance and cost predictability. Resources such as the baseline packaging parameter checklist provide a structured approach to identifying these characteristics across several fundamental parameter groups.

For folding cartons, this typically includes basis weight with explicit tolerance bands, caliper ranges tied to filling-line requirements, moisture content windows that prevent warping, and barrier properties specified by test method rather than by marketing language. Board grade tolerances explained: securing folding carton specifications across suppliers deserves particular attention—a grade name alone allows suppliers to interpret specifications differently, creating quote variance that looks like pricing when it is actually scope variance.

If food-contact compliance applies—particularly for food packaging paper applications—regulatory requirements add another layer of specification. Migration testing conditions, coating requirements, and certificate scope all affect what suppliers can legitimately quote. The FDA’s Packaging & Food Contact Substances guidance and EU Regulation 1935/2004 provide reference points for those requirements, though market-specific review remains essential.

The deliverable from Stage 1 is a buyer-owned specification document—not a supplier data sheet, not a verbal description, but a version-controlled document serving as the technical benchmark for all subsequent RFQs.

Stage 2: Implementing Specification-True RFQs to Eliminate Supplier Ambiguity

With tolerances defined, the next stage translates them into RFQ language that forces comparable responses.

A specification-true RFQ does three things. First, it attaches the buyer-owned specification as the governing document, making clear that supplier interpretation is not welcome. Second, it requires suppliers to confirm capability against each specified parameter—not with generic compliance statements, but with evidence tied to the actual fields. Third, it standardizes the commercial basis so that responses can be compared without forensic reconstruction.

In practice, a specification-true RFQ includes one controlled technical specification, one commercial assumptions sheet, one response template, and one clear instruction on how exceptions must be declared. Alternatives can still be useful—they simply need to sit in a separate lane from the base quotation. Otherwise, a team ends up comparing a standard folding carton from one supplier against a modified construction from another without realizing it.

The commercial basis matters as much as the technical specifications. An RFQ that asks for “best price” without specifying delivery terms invites quotes on different Incoterms® 2020 bases. One supplier quotes EXW, another quotes CIF, a third quotes DDP. The numbers look different, but the comparison is meaningless because each quote includes different cost components. Specify a single Incoterm and named place for all responses.

The RFQ should also request evidence of capability at the quoting stage—not after award, when leverage disappears. For critical parameters, ask for recent test reports using the methods named in the specification. For compliance requirements, ask for certificate copies with scope verification. This supplier vetting discipline filters out vendors who cannot actually hold the tolerances before pricing even enters the evaluation.

For Procurement, this stage improves supplier vetting because it reveals who follows the brief cleanly, who flags risks early, and who fills gaps with assumptions. For Finance, it improves the eventual cost structure because the quote has a more stable foundation. For Operations, it reduces late-stage surprises. Comparability before price: the spec-true mindset that reduces kraft paper RFQ chaos provides deeper methodology for teams building this discipline.

The deliverable from Stage 2 is a set of quotes that respond to identical requirements on identical commercial terms. Variance in these quotes now reflects actual pricing differences, not hidden scope differences.

Stage 3: Normalize Quotes to a Common Landed-Cost Basis

Even with specification-true RFQs, quotes rarely arrive in directly comparable form. Stage 3 closes the remaining gaps.

Landed cost means the total cost to receive material at your facility, ready for use. It includes the quoted unit price, freight to your location, insurance, duties if applicable, handling, and any other charges that will appear on invoices downstream. Common pitfalls in landed-cost estimates of kraft paper (and how to avoid invoice disputes) covers the most frequent mistakes: forgetting to add destination charges, applying inconsistent exchange rate assumptions, and treating quoted terms as equivalent when they are not.

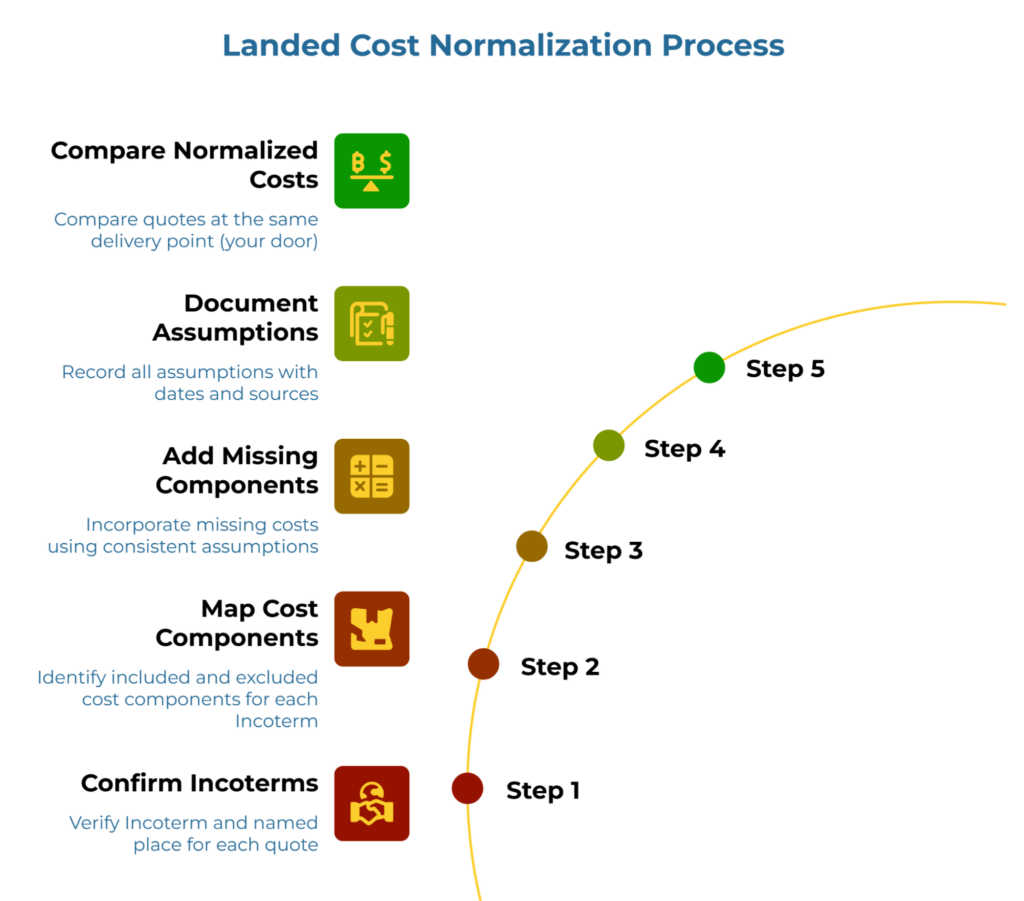

The normalization process is methodical. Start by confirming the Incoterm and named place for each quote. Map the cost components that each Incoterm includes and excludes. Add the missing components using consistent assumptions—same freight rate source, same insurance percentage, same duty classification. Document every assumption with dates and sources.

Trade terms matter here because they define where responsibility and cost shift between seller and buyer. The International Chamber of Commerce describes Incoterms® 2020 rules as a set of eleven three-letter trade terms used in contracts for the sale and purchase of goods, with costs consolidated so users can see expected cost allocation more clearly. That framework provides the reference point for normalization.

Illustratively, if one supplier quotes EXW their factory and another quotes CIF your nearest port, the EXW quote needs freight-to-port, origin handling, ocean freight, and insurance added before comparison. The CIF quote still needs destination handling and inland freight to your facility. Only after both quotes reach the same delivery point—your door—can the numbers be compared.

The deliverable from Stage 3 is a normalized cost comparison where every quote reflects the same scope, the same delivery point, and the same assumption set. This is the input Finance needs for reliable budgeting.

Stage 4: Build the Budget Model and Governance Loop

Normalized costs become predictable budgets only when the organization commits to maintaining the underlying discipline.

A one-time normalization exercise produces a snapshot. Markets shift, volumes change, and suppliers adjust. Without a governance loop, the carefully built cost structure decays back into the chaos it replaced.

Governance means defining who owns the specification, who validates changes, who updates the cost model, and how often reviews occur. As a general principle, a reliable budget model does three things: it records assumptions clearly, it assigns ownership clearly, and it defines review cadence clearly. Without those three controls, even a well-built first model will drift as specifications change, supplier terms shift, or new SKUs enter the mix.

For cross-SKU material standardization, governance also means controlling how new products inherit or deviate from established specifications—preventing the portfolio drift that creates specification chaos over time.

The budget model itself should separate what is known from what is assumed. Locked parameters—specification tolerances, contracted volumes, agreed payment terms—form the stable foundation. Variable parameters—freight rates, exchange rates, commodity-linked price adjustments—get explicit assumption bands with triggers for review. When a variable breaches its band, the model flags a re-forecast rather than silently drifting.

The deliverable from Stage 4 is not just a spreadsheet but a repeatable management process: specification discipline feeding RFQ discipline feeding cost normalization feeding budget governance feeding back into specification updates as requirements evolve.

A Shared Checklist for Procurement, Operations, and Finance

The four-stage sequence only works when stakeholders agree on who owns what.

Procurement owns specification alignment, supplier vetting, RFQ normalization, and version control.

Operations or Quality validates barrier requirements, line fit, structural performance, and test-method relevance.

Finance owns the landed-cost model, budgeting frameworks, review cadence, and cost-control assumptions.

Shared ownership applies to change control: no quiet specification edits, no mixed quote bases, and no budget updates without documented assumptions.

The handoffs between functions need explicit protocols. When Operations updates a tolerance, Procurement re-quotes affected suppliers. When Procurement normalizes costs, Finance validates assumptions. When Finance flags a variance, the team investigates whether the root cause is specification drift, supplier performance, or market movement.

This is not bureaucracy. It is clarity about who decides what, documented before disputes arise.

Common Failure Modes That Break Predictable Folding Carton Costs

Even organizations that understand the four-stage sequence can fail at execution. These patterns appear repeatedly.

Copying supplier-led data sheets instead of defining specifications. Supplier data sheets describe what suppliers want to sell, not what buyers need to buy. They often omit tolerance bands, use proprietary test methods, and conveniently exclude parameters where the supplier is weak. Starting from supplier documents instead of buyer requirements guarantees specification gaps.

Comparing quotes before normalization. The lowest quoted price can sometimes become the highest landed cost once freight, duties, and hidden charges appear . Awarding business on unnormalized quotes rewards suppliers who hide costs in commercial terms rather than suppliers who deliver value.

Treating unit price as total cost. Unit price ignores yield loss, rework rates, downtime from specification drift, and the administrative cost of managing quality disputes. A supplier whose folding cartons jam the filling line twice per shift is not cheaper than a competitor whose folding cartons run clean, regardless of what the price list says.

Running multiple specification files with weak version control. When Procurement has one specification version, Operations has another, and the supplier quotes against a third, everyone is working from a different blueprint. Version control is not optional once specifications become commercial documents.

Budgeting without locking assumptions. A budget model that says “freight included” without documenting which rate, which lane, and which date is not a forecast—it is a guess with formatting.

Your Next 30 Days: The Procurement Transition Roadmap

Understanding the sequence is the first step. Implementing it requires a realistic timeline. The following roadmap provides a practical path from current state to specification-driven procurement.

Days 1–7: Audit current specifications. Gather every specification document, supplier data sheet, and RFQ template currently in use. Identify which parameters are defined with measurable tolerances and test methods, and which rely on vague language or supplier interpretation. This audit reveals the gap between current practice and Stage 1 requirements.

Days 8–14: Draft buyer-owned specifications. For one high-volume SKU family, create a controlled specification document that defines tolerances, test methods, and compliance requirements. Have Operations validate that the parameters reflect actual production needs. Have Finance confirm that the specification scope matches budgeted cost assumptions.

Days 15–21: Issue a pilot specification-true RFQ. Using the new specification, issue an RFQ to existing suppliers and at least one new candidate. Require responses on a single Incoterm basis with evidence of capability for critical parameters. Compare the quality of responses to previous RFQ cycles.

Days 22–30: Normalize and document. Normalize pilot RFQ responses to landed cost using explicit, documented assumptions. Present the normalized comparison to stakeholders. Identify process improvements for the next cycle. Establish the review cadence that will govern ongoing cost updates.

This 30-day cycle produces a working prototype of the four-stage process for one SKU family. Subsequent cycles extend coverage to additional products, refine the specification templates, and build the institutional knowledge that makes predictable costs sustainable.

Moving from Method to Market

Predictable folding carton costs are not a spreadsheet problem. They are a specification problem, an RFQ problem, and a normalization problem that only becomes visible as a spreadsheet problem after the budget fails.

The four-stage transition—define tolerances, issue specification-true RFQs, normalize to landed cost, build governance—creates the upstream discipline that downstream budgets require. Each stage has a clear deliverable, a clear owner, and a clear connection to the next.

Organizations that follow this sequence find that cost surprises decrease, supplier comparisons become meaningful, and Finance stops asking why the forecast missed. The spreadsheet finally reflects reality because the inputs finally reflect comparable data.

The alternative is continuing to build budgets on vague specifications and incomparable quotes—and continuing to be surprised when reality diverges from the model.

A useful next step is to deepen the method before widening the supplier pool. PaperIndex Academy supports teams still refining their specification and RFQ workflow. Once the specification package is controlled and the commercial basis is clear, connecting with verified folding carton manufacturers becomes the natural next move.

Disclaimer:

This article is educational. PaperIndex does not sell market intelligence or publish pricing indices. Any examples above are illustrative or hypothetical.

Our Editorial Process:

Our expert team uses AI tools to help organize and structure our initial drafts. Every piece is then extensively rewritten, fact-checked, and enriched with first-hand insights and experiences by expert humans on our Insights Team to ensure accuracy and clarity.

About the PaperIndex Insights Team:

The PaperIndex Insights Team is our dedicated engine for synthesizing complex topics into clear, helpful guides. While our content is thoroughly reviewed for clarity and accuracy, it is for informational purposes and should not replace professional advice.