📌 Key Takeaways

Operations and Finance disagree on supplier quotes because they measure different things—one tracks supply security, the other tracks cash exposure.

- Same Quote, Different Pictures: Procurement sees inventory continuity while Finance sees cash tied up in hidden costs neither team fully mapped.

- Unit Price Comparisons Mislead: Comparing quotes without matching their delivery terms hides freight, insurance, and duties that change the real cost.

- Normalize to the Same Finish Line: Convert every quote to full door-to-door cost before deciding which supplier actually offers better value.

- Document Every Assumption: Write down freight estimates, duty rates, and exchange rates so both teams review the same numbers.

- One-Page Summaries Speed Approval: A single document showing true costs, cash timing, and risk scenarios gets faster sign-off than scattered emails.

Shared cost visibility turns supplier debates into math-based decisions.

Procurement managers and finance leads at SME toilet paper converting operations will find a ready-to-use alignment framework here, preparing them for the checklist and one-pager templates that follow.

~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

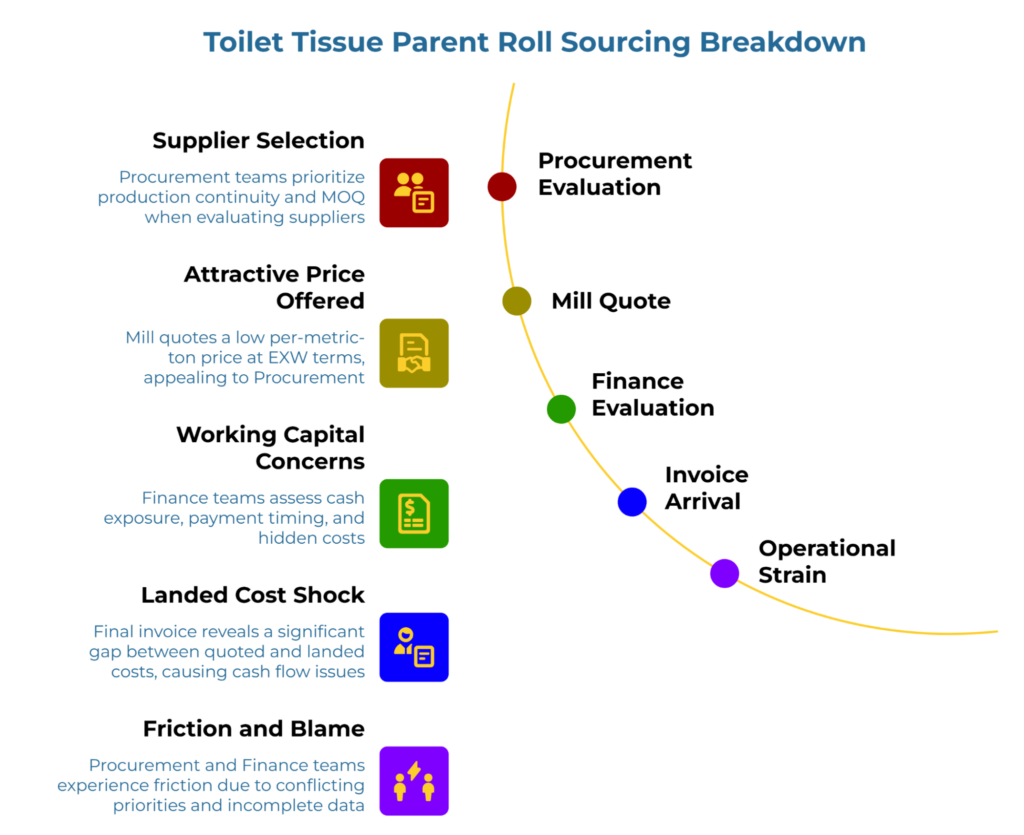

A toilet tissue parent roll quote lands on the procurement desk. The numbers look promising—competitive per-metric-ton pricing, Minimum Order Quantity (MOQ) volumes that would keep the converting line running through the quarter, delivery terms that seem reasonable. Procurement sees an opportunity to secure supply continuity. Down the corridor, Finance sees something different: a six-figure cash commitment stretching across a 60-day payment window, with a list of unstated assumptions that could quietly inflate the true cost by double digits.

Both teams are evaluating the same supplier. Both believe they are protecting the business. Yet the approval conversation stalls, caught between two legitimate but incomplete cost pictures.

This disconnect frequently destabilizes SME converting operations globally. The root cause is rarely the quote itself. The friction stems from Operations and Finance viewing landed cost through fundamentally different lenses—and neither lens captures the full picture. The solution is not another spreadsheet—it is a shared framework for landed cost predictability that both teams can review, challenge, and approve together.

Why Toilet Tissue Parent Roll Sourcing Breaks Down Between Operations and Finance

Procurement teams evaluate toilet tissue raw materials suppliers with production continuity as the priority. A favorable MOQ means fewer reorder cycles, stronger unit economics, and a buffer against supply disruptions. When a mill quotes an attractive per-metric-ton price at EXW terms, Procurement sees a chance to lock in volume and stabilize the converting schedule for weeks ahead.

Finance teams evaluate the same quote through the lens of working capital protection. They see cash exposure, payment timing, and a long list of costs sitting outside the mill’s headline number—ocean freight, cargo insurance, import duties, port handling, and inland transport to the facility. When the final invoice arrives and the gap between quoted price and true landed cost triggers a cash flow shock, the strain ripples across the entire operation.

The friction is structural, not personal. Procurement optimizes for supply security and MOQ alignment. Finance optimizes for liquidity and downside containment. When both teams compare quotes using only the mill’s unit price, they are comparing incomplete numbers.

Consider the difference between a $920/metric-ton EXW quote versus a $1,050/metric-ton CIF quote. These figures cannot be evaluated side by side until the hidden cost layers—including terminal handling charges (THC), port congestion surcharges, and customs brokerage fees—are surfaced and normalized to a common delivery basis. Supplier quote variance becomes invisible when the comparison ignores Incoterm responsibilities.

According to the ICC Incoterms rules, each trade term allocates specific costs, tasks, and risks between buyer and seller. An EXW quote excludes freight, insurance, and customs clearance—all of which become the buyer’s responsibility. A CIF quote typically bundles freight and minimum-cover cargo insurance into the price, but leaves the buyer responsible for import duties, Value-Added Tax (VAT) where applicable, and destination terminal handling, while risk transfers at the load port (ICC Incoterms® 2020 Rules). Without Incoterm normalization, quote comparisons are misleading at best and commercially untenable. The mechanism of failure is straightforward: comparing different Incoterms solely on unit price ignores variable freight, insurance, and import duties, leading to a financial shortfall that can exceed 15–20% of the initial quote—a dynamic explored in depth in our guide on common pitfalls in landed-cost estimates.

The Integrated Landed-Cost Model

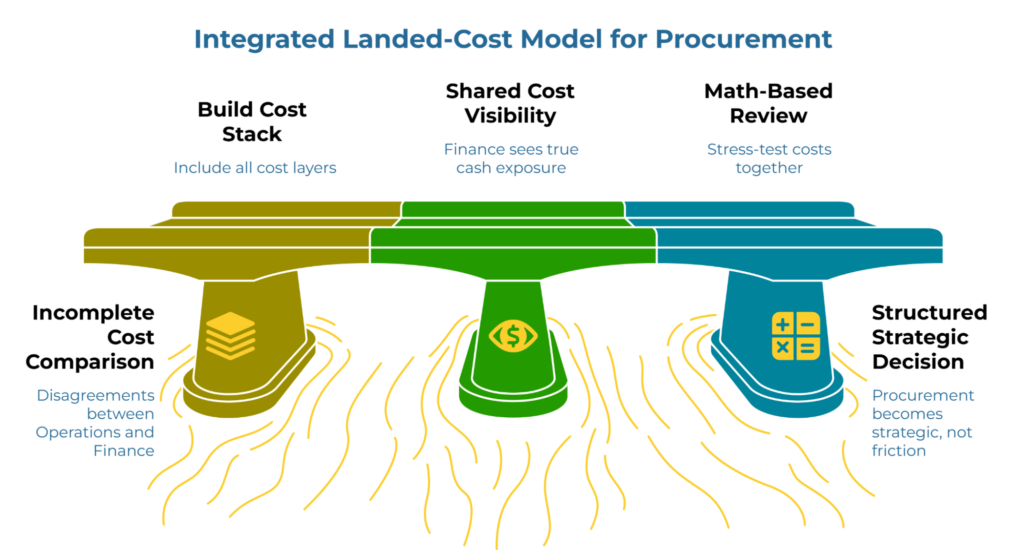

The bridge between Operations and Finance is a shared to-door cost normalization model. Instead of debating which quote appears cheaper on paper, both teams review a single cost stack that translates every supplier’s offer into the same delivery basis: the true landed pricing required to move toilet tissue parent rolls from the mill gate to the converting facility door.

Think of it like comparing airline tickets. One fare shows only the base price. Another bundles taxes and fees. A third includes baggage and seat selection. Comparing them requires normalizing every ticket to the same ready-to-fly total. Toilet tissue parent roll sourcing works identically—without to-door equivalent modeling, the comparison is incomplete.

For smaller converters, this discipline matters even more. Financing constraints are common for small and medium businesses, as the World Bank’s overview of SME finance confirms. Landed cost predictability is not optional analysis for these operations—it is a core component of liquidity preservation.

The minimum cost layers both teams must view together include the quote basis and Incoterm (EXW, FOB, CIF, or another term), estimated or contracted freight costs, cargo insurance, import duties and tariffs, port handling and terminal charges, and inland transport to the facility. Hidden freight calculation becomes explicit. Assumptions move from unstated to documented.

When Procurement builds this cost stack for each supplier, Finance gains visibility into true cash exposure—not just the mill’s headline number. The framework does not replace negotiation. It enables it. When both teams see the same normalized to-door cost, disagreements shift from competing spreadsheets to shared stress-testing. The debate becomes a math-based review, not a departmental standoff. A shared predictive model turns international toilet tissue procurement into a structured strategic decision rather than a recurring source of internal friction.

For a deeper methodology on aligning specifications before cost comparison, specialized industry resources on toilet tissue raw-materials normalization generally offer a complementary framework.

The Alignment Checklist for Toilet Tissue Parent Roll Approval

Before any parent roll sourcing decision reaches final approval, both Procurement and Finance should confirm the following shared benefits of a normalized review:

- Verify the quote basis. Every supplier quote must be converted to the same Incoterm or delivery basis. If one quote is EXW and another is CIF, the missing cost layers have been estimated and added to enable true-to-door comparison.

- Separate hidden freight, insurance, and duties. The mill’s quoted price has been unbundled from logistics costs. Each line item—freight, insurance, import duties, destination charges—is visible and itemized, not buried in a single number.

- Translate the MOQ to its cash-cycle impact. The minimum order quantity has been expressed in working capital terms: how much cash is committed, for how long, and what inventory runway it creates for the converting operation. MOQ alignment means both teams see the same volume-to-cash picture.

- Document all assumptions in one place. Exchange rate assumptions, freight rate estimates, duty classifications, and lead time expectations are written down. Nothing is “understood” without being stated.

- Review downside scenarios. Finance has seen at least one stress-test scenario showing what happens if freight rates increase, if duties are reclassified, or if the shipment is delayed. Approval confidence comes from understanding variance, not ignoring it.

This checklist is not bureaucracy. It is the minimum standard for an approval-ready toilet tissue sourcing case. Teams that skip these steps often revisit the same supplier decision months later, after unexpected costs have already strained cash reserves.

Standardizing the Executive Approval Workflow

The alignment checklist above feeds into a single consensus-building asset: the Executive Summary One-Pager. This document is what Procurement hands to the Founder or Finance Lead before a final sourcing commitment. It transforms scattered quote details into a founder-readable summary that answers one question: what are we actually committing to, and what could change?

The one-pager should contain six sections: the supplier and quote identifier, the Incoterm and delivery basis, the normalized to-door landed cost stack, the MOQ and its working-capital implication, the key assumptions and any unresolved variables, and a clear recommendation or proposed next step.

Procurement owns the drafting. Finance owns the validation. The Founder or Owner reviews a single page that bridges Procurement’s need for inventory continuity with Finance’s need for working capital protection.

When this document becomes standard practice, approval conversations accelerate. Finance no longer needs to reconstruct the cost picture from scattered emails. Procurement no longer needs to defend a quote that was never fully contextualized. Both teams operate from the same source of truth.

For comparing EXW and CIF structures specifically, dedicated standard operating procedures on how to normalize EXW and CIF toilet tissue quotes typically provide a step-by-step methodology.

Strategic Outcomes of Cross-Functional Calibration

When Operations and Finance share one cost model, supplier evaluation changes fundamentally. Instead of cycling through quote-by-quote debates, the team moves faster into relationship-building with pre-qualified toilet tissue parent roll suppliers. Internal alignment does not guarantee the right supplier—but it removes the friction that slows down good decisions.

Aligned teams also audit current parent roll supplier specifications more rigorously, because both Procurement and Finance understand what a complete supplier file should contain. The conversation shifts from “defend this quote” to “evaluate this opportunity together.”

When both teams use the same predictive model, international procurement becomes a unified strategic advantage rather than a recurring source of organizational tension.

For more sourcing frameworks and specification guides, explore the PaperIndex Academy.

Disclaimer:

This content is for informational purposes only and does not constitute financial, legal, or professional procurement advice. Freight rates, duties, tariffs, and landed costs vary by supplier, route, and market conditions. Consult qualified finance and trade compliance professionals before making sourcing commitments.

Our Editorial Process:

Our expert team uses AI tools to help organize and structure our initial drafts. Every piece is then extensively rewritten, fact-checked, and enriched with first-hand insights and experiences by expert humans on our Insights Team to ensure accuracy and clarity.

About the PaperIndex Insights Team:

The PaperIndex Insights Team is our dedicated engine for synthesizing complex topics into clear, helpful guides. While our content is thoroughly reviewed for clarity and accuracy, it is for informational purposes and should not replace professional advice.